Big Banks Face an Uphill Battle in the Digital Wallet Wars

Key Takeaways

Around two-thirds of U.S. adults already use a digital wallet every month, with PayPal being the most widely adopted.

Consumers aren’t loyal to one specific digital wallet; instead, they’re likely to use many brands, and are satisfied doing so.

Banks should view the digital wallet they’re building as a necessary step to stay relevant, but not one that will get customers to abandon their existing wallets or wallet providers.

In the never-ending struggle to protect their customer relationships from disintermediation by fintechs, some of the country’s largest consumer banks have decided to create a digital wallet for use in online checkout. The announcement has been met with skepticism by many industry analysts, and with good reason.

New analysis from Morning Consult reveals that a big bank-backed digital wallet will face several challenges to its success: a crowded competitive landscape with a clear front-runner, a disloyal customer base and barriers to frequent usage, even if the new digital wallet is widely adopted.

The future of wallets is digital, and it’s already here

Digital wallets are not new, nor are they novel. Around two-thirds of U.S. adults have used a digital wallet to make a purchase at least once a month since we began tracking usage in 2021. This metric does ebb and flow slightly with shopping seasons and macroeconomic conditions, but its stability shows mass adoption has already happened.

Not only are a majority of consumers regularly using digital wallets, but they’re doing so more than other traditional financial activities. Notably, the share of U.S. adults who use a digital wallet consistently exceeds the share that say they visited a bank branch or used an ATM. This change in behavior is a perfect example of the tectonic shifts in consumers’ banking and payment habits that leave branches (and the banks that own them) crumbling in importance while digital wallets rise as the new centers of consumers' financial lives.

The strong adoption of digital wallets by U.S. adults can be attributed in part to the fact that there are many to choose from. Apple Pay, Cash App, PayPal, Google Pay and Venmo are some of the biggest names in the digital wallet space, and each has a healthy share of monthly users in the United States. According to Morning Consult Brand Intelligence, PayPal is the digital wallet to beat, with 71% of U.S. adults reporting that they use the service as of February 2023.

PayPal’s dominance makes sense. The service has been around for over 20 years, while its closest competitor, Cash App, has been around roughly half as long. Although their user bases pale in comparison to PayPal’s, digital wallets Apple Pay, Cash App, Google Pay and Venmo have all amassed strong adoption since their debuts. Suffice it to say, banks are entering the digital wallet race late, and they’re up against established behemoths.

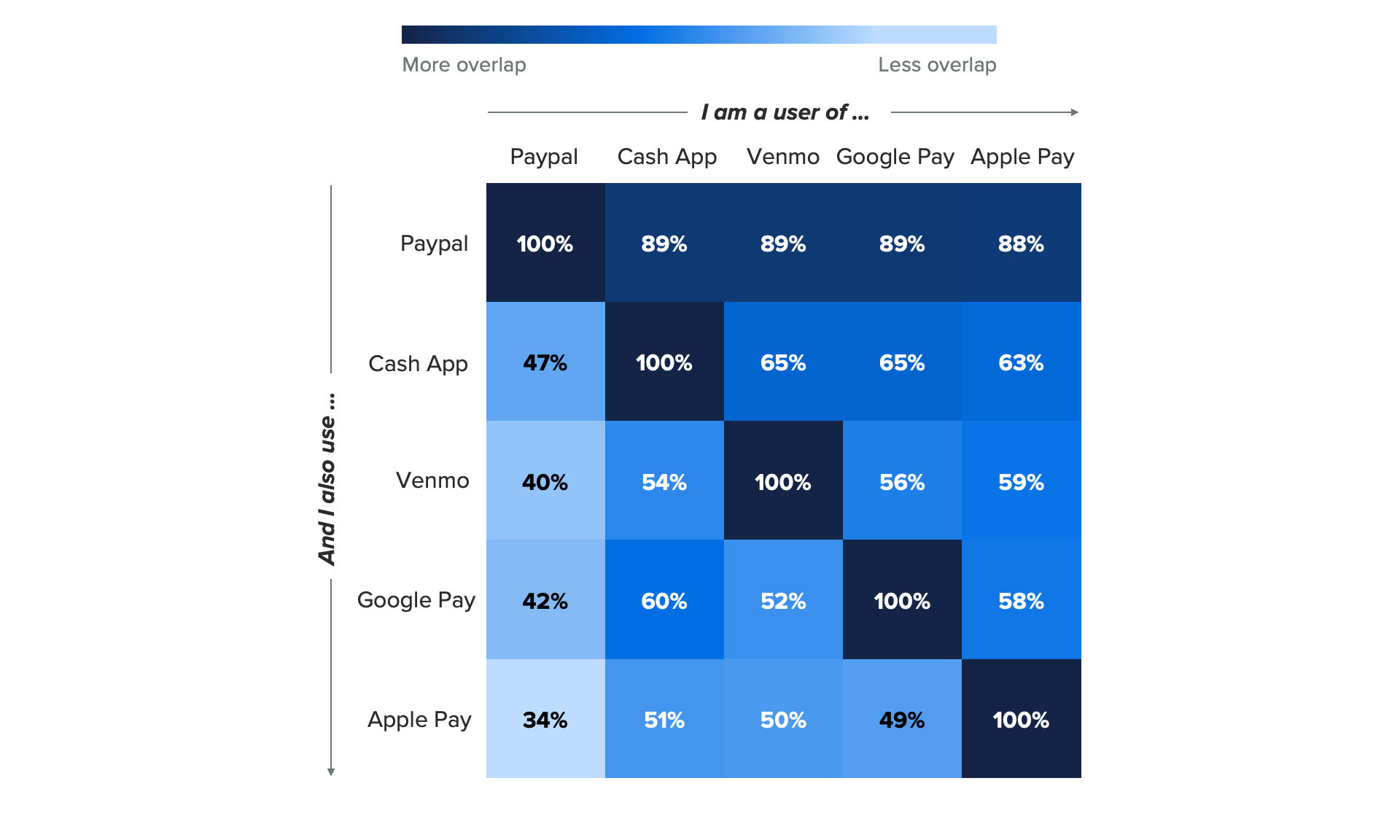

Digital wallets are not a winner-take-all game; disloyalty is the norm

While having only one physical wallet may make sense for most adults, this isn’t the case for digital wallets — at least not yet. MCBI data shows that users of one digital wallet are very likely to use others as well. For example, a staggering 88% of Apple Pay users say they also use PayPal. The latter’s dominance is especially visible in this respect. Nearly every user of any competitor digital wallet also uses PayPal, but the overlap doesn’t stop there: 65% of Google Pay users also use Cash App, and over half of Cash App users also use Venmo.

This use of multiple digital wallet providers may suggest there are gaps a new competitor could fill, but that’s actually not the case. Consumers across the board say they are highly satisfied with their digital wallet providers, even though they use multiple. For example, 82% of Venmo users have a favorable view of the app, despite the fact that 65% of them also report using Cash App. It seems consumers are content managing their money with various digital wallets and don’t expect one digital wallet to serve all their needs.

The high satisfaction but high disloyalty is due to two factors: First, these providers have gone to great lengths to make it easy to sign up for their wallets, and second, not every merchant or retailer accepts every wallet, making it necessary for consumers to have several wallets to meet their payment needs.

While this is great news for banks in the sense that customers don’t seem to have a limit to the number of digital wallets they’ll sign up for, it doesn’t guarantee they’ll actually use a new wallet with any frequency.

The Zelle lesson: Strong distribution does not guarantee strong usage

The history of money transfer service Zelle, another consortium-created response to fintech threats, provides insight as to what the future of a bank-owned digital wallet may hold. Zelle is a relative latecomer to the peer-to-peer money transfer space, but it currently boasts adoption by 39% of U.S. adults — more than Apple Pay and Google Pay, and the same as Venmo. This is a testament to the power of strong distribution: Zelle had rapid adoption due to its automatic integration into the mobile apps of more than 30 U.S. banks.

But strong distribution has not translated to high usage frequency for Zelle. The money transfer service lags behind digital wallets by this metric, with less than half of users saying they make a transfer through Zelle more than once a month. This is a challenge because it’s usage that makes money, not distribution. Digital wallet and money transfer services gather a fee for each transaction, not each user, and unfortunately for them, it only takes one wallet to make a purchase. In that sense, the success of a digital wallet isn’t determined so much by the number of users, but by the number of purchases or payments it is used for. And the number of purchases a digital wallet is used for is determined by the number of places where it’s accepted — i.e., the distribution or merchant adoption.

The same consortium that created Zelle is powering the new digital wallet, and will likely take a similar approach to its rollout strategy as they did with Zelle — i.e., automatic or very simple activation within their mobile banking apps. Adoption of the new digital wallet may be very high if this is the case, but unlike Zelle, the new digital wallet will only be as successful as the extent of its adoption by online merchants. Since Zelle is for peer-to-peer payments, both sides of any transaction were immediately able to use the app when it was introduced. For a digital wallet, consumer adoption is only half the battle to winning pride of place in consumers’ wallet queues. Online merchant adoption will be the ultimate determinant of the wallet’s success.

Despite these challenges, banks likely feel they have no choice but to develop one anyway. While their hope is to protect customer relationships from being poached by PayPal or Apple Pay, the reality is that their new digital wallet will only help them stay relevant. Consumers’ wallets are already fractured across multiple providers. As banks prepare to launch a digital wallet, they should also recognize that a winner-takes-all approach is not possible in the current competitive environment, and that success will not be determined by consumer adoption, but rather by merchant adoption, which is the true gateway to higher usage frequency.

Charlotte Principato previously worked at Morning Consult as a lead financial services analyst covering trends in the industry.