Consumer Confidence Unfazed by Omicron, Rising Cases

Key Takeaways

The emergence of the omicron variant and a recent rise in new COVID-19 cases have had little impact on consumer confidence.

U.S. consumer sentiment has become increasingly resilient to rising cases over the course of the pandemic as Americans adjust their lifestyles and learn to cope with the public health risks.

Despite a modest rise in lost employment income in some sectors, broad employment conditions are improving rapidly, which should support consumer confidence and overall resilience in the economy moving into 2022.

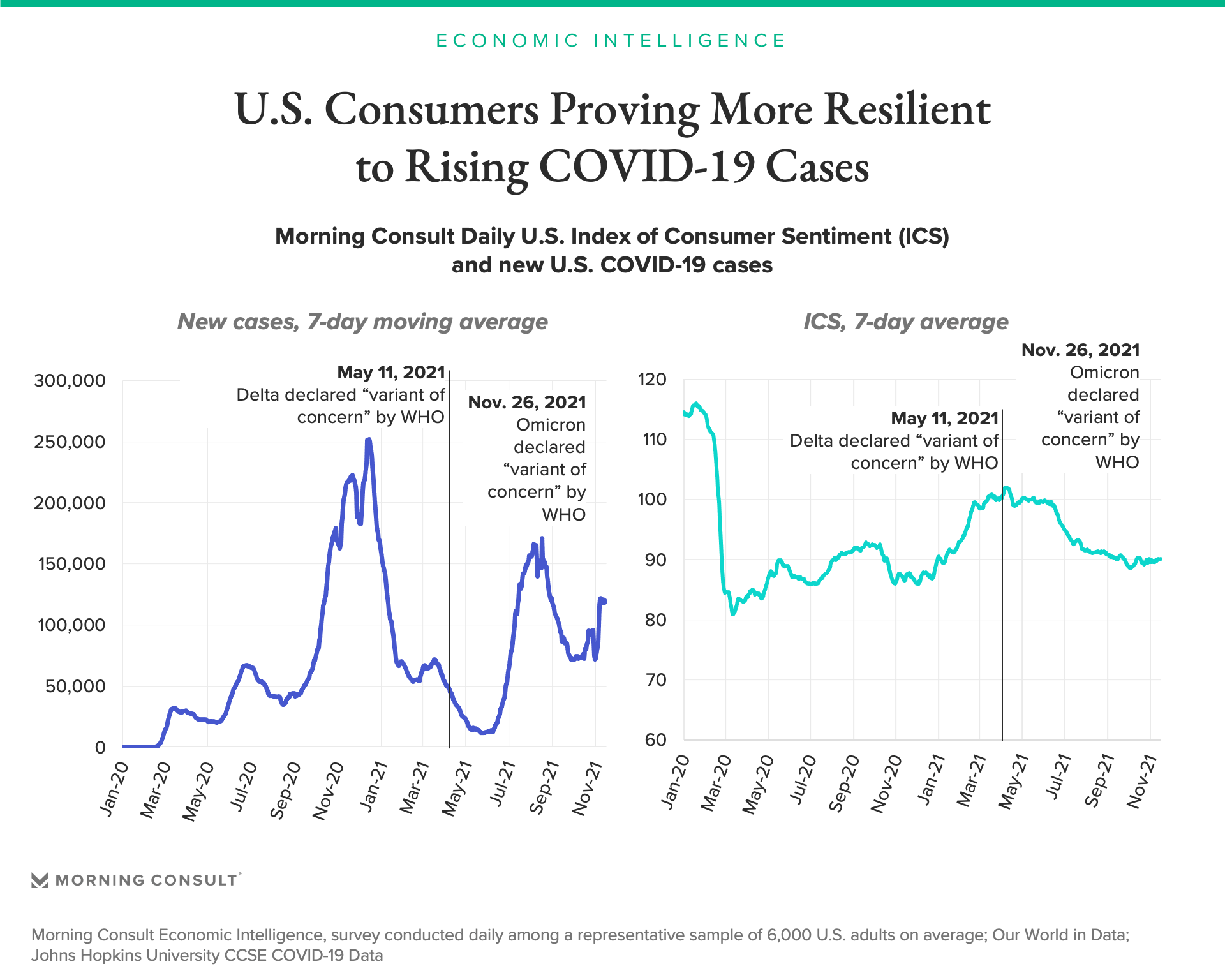

U.S. consumers have not materially changed their economic outlook over the past month, despite a recent surge in new COVID-19 cases and the emergence of the omicron variant. Since omicron was deemed a “variant of concern” on Nov. 26, Morning Consult’s Index of Consumer Sentiment (ICS) has remained largely unchanged, with the seven-day moving average currently at 90.1. Likewise, the surge of COVID-19 cases in recent weeks has had little impact on consumer confidence; the ICS has hovered around 90 since mid-November.

Over the course of the pandemic, U.S. consumers have become increasingly resilient to subsequent surges in COVID-19 cases. As previously reported in Morning Consult’s October U.S. Economic Outlook report, the scope and pace of case-driven declines in sentiment have diminished over time. Vaccines, adjustments in lifestyle and increasing risk tolerance are all likely playing a role in limiting the impact of rising case counts on confidence.

According to Morning Consult’s Return to Normal tracker, 38 percent of U.S. adults are “very” concerned about COVID-19 as of Dec. 4, down from 47 percent in mid-September and a peak of 65 percent in April 2020. Consumers' comfort with activities like dining out, traveling or attending sporting events has also been largely unchanged by recent increases in cases or the emergence of the omicron variant.

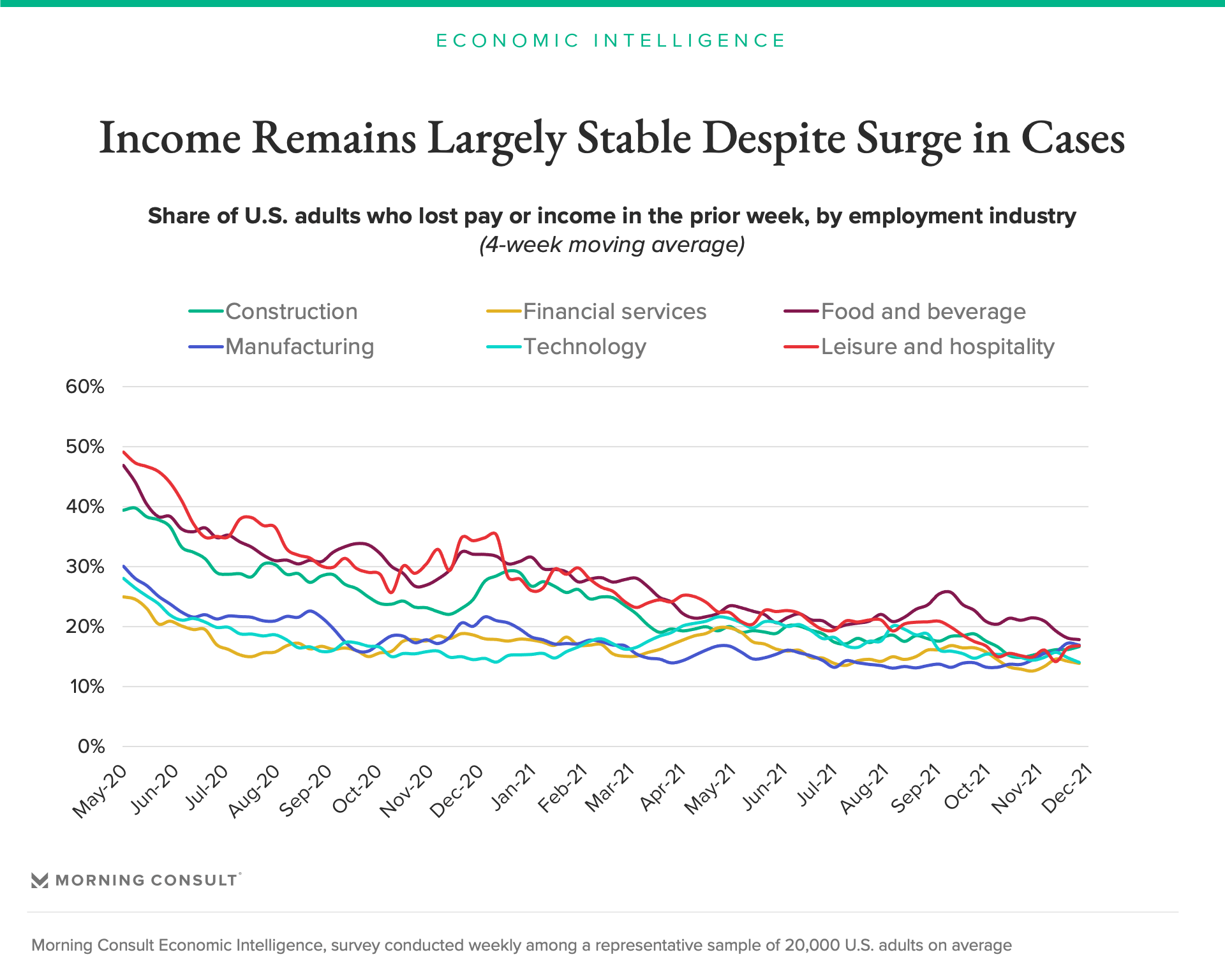

Additionally, unlike during the onset of the delta variant in the U.S., the recent surge in cases has yet to drive a significant uptick in lost employment income or derail broad labor market gains. Workers in sectors that have been more susceptible to losses during past COVID-19 surges — like leisure and hospitality and food and beverage — are still reporting broadly stable employment income. In the past two weeks, the share of food and beverage industry workers experiencing lost pay or income has actually fallen, with the four-week moving average declining from 19.2 percent to 17.8 percent. For leisure and hospitality workers, the four-week moving average has risen moderately from 14.1 percent to 16.7 percent — but still well below the 19 percent to 21 percent recorded during the initial delta surge from July to September.

Looking forward, consumer confidence could still be shaken by further deterioration in the public health situation moving into winter, as COVID-19 still presents the biggest risk to the economic recovery. While rising prices and supply chain issues will remain a top concern for consumers, recent data shows reason for optimism, despite last Friday’s decades-high CPI number: Inflation expectations have begun to stabilize, and the latest Morning Consult data indicates that the share of consumers reporting difficulty obtaining certain goods fell across most categories from October to November. Increased confidence is leading more Americans back into the labor force and will also enable a shift back toward more spending on services, all of which should help to ease price pressures in 2022.

Jesse Wheeler previously worked at Morning Consult as a senior economist.