Inflation and Pay Losses Drive Financial Vulnerability

Key Takeaways

Financial vulnerability surged in January due to the combination of elevated inflation, income losses and reduced policy support.

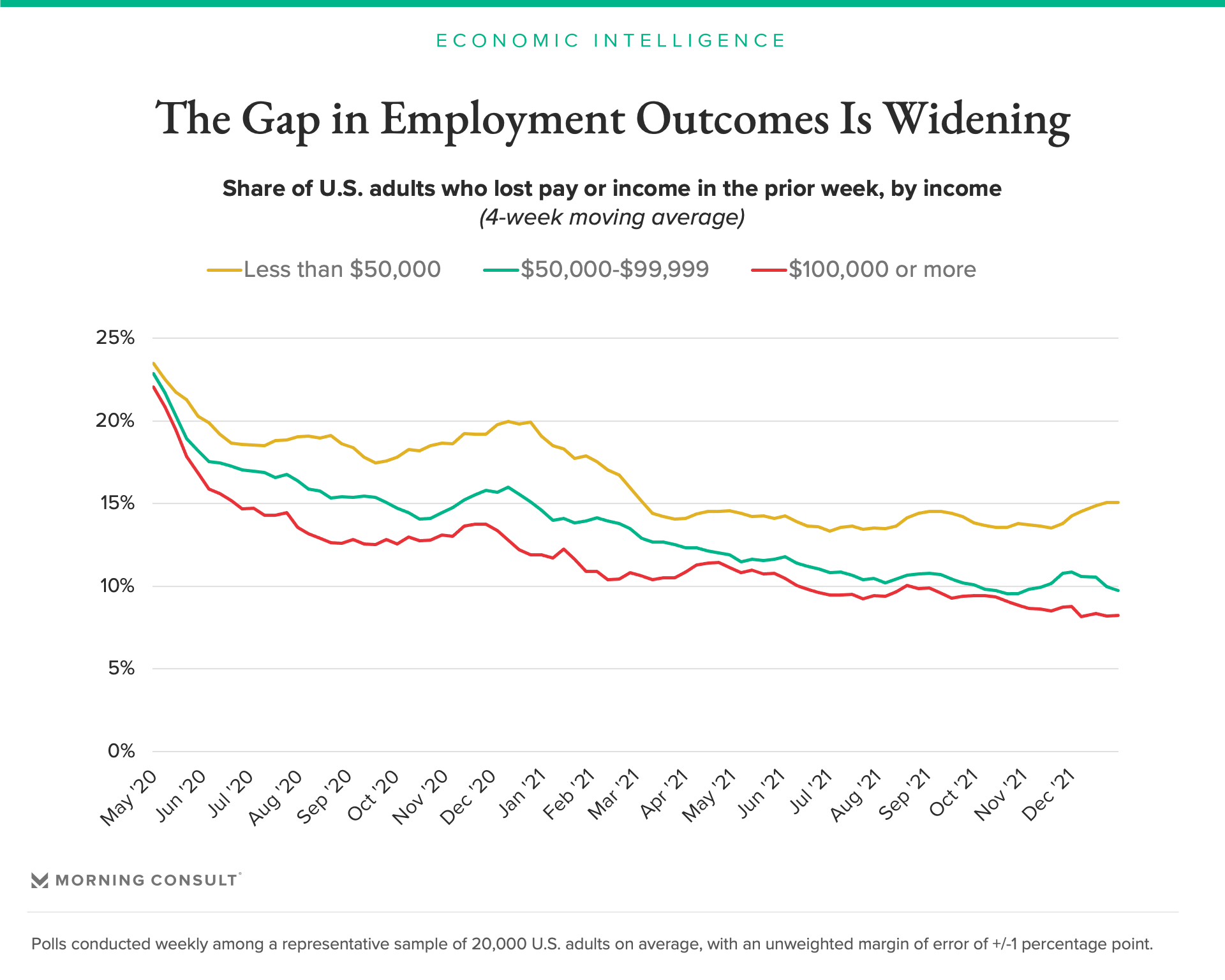

Lower-income adults spend a relatively higher share of their incomes on nondiscretionary goods and services, making it more difficult to tighten their belts in the face of higher prices and income losses.

If Americans’ personal finances continue to deteriorate, inflation-adjusted consumer spending will suffer, with consumer delinquencies and defaults likely to rise throughout 2022.

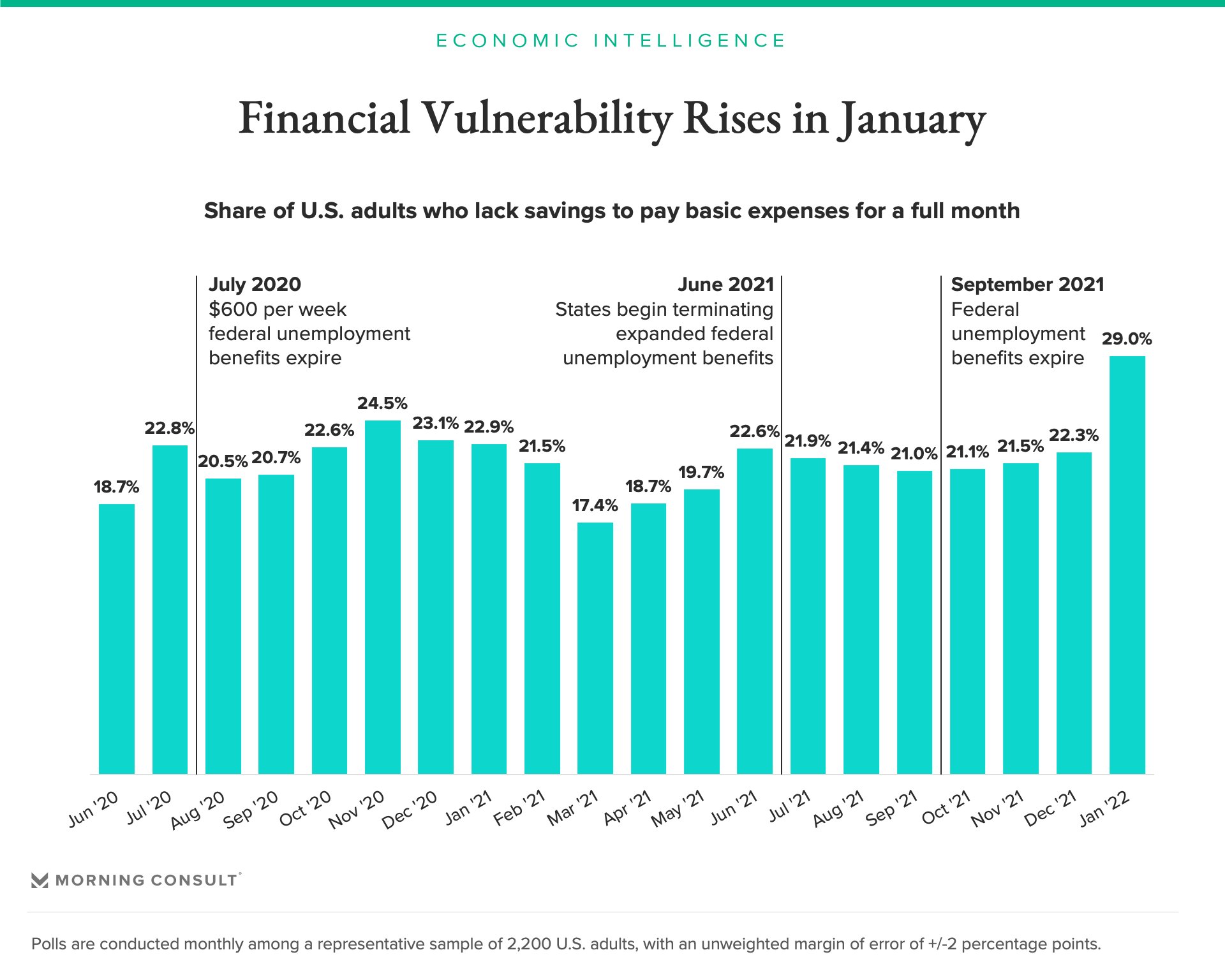

Over the past six weeks, rising prices combined with elevated income losses forced Americans to draw down their savings faster than they were able to reduce their basic monthly expenses. The share of adults who reported insufficient savings to cover a month’s worth of basic expenses rose to 29.0 percent in January, the highest value on record since the survey question began in May 2020.

As reported in Morning Consult’s January U.S. Consumer Spending Report, consumers decreased discretionary spending in December, but modest increases in nondiscretionary goods and services ultimately forced adults to eat into their savings through mid-January.

Income losses related to the omicron-driven case surge were also largely borne by low-income households, disproportionately impacting those least able to cope. During the week ending Jan. 22, 15.0 percent of adults from households earning less than $50,000 reported lost pay or income, up from 13.1 percent at the end of November and nearly double the 8.7 percent of those from households with incomes of $100,000 or more who said the same. Given the already thin — and often nonexistent — savings cushion among lower-income adults, this widening gap in employment outcomes helped increase financial vulnerability among low-income households to 39.8 percent in January.

January’s jump in financial vulnerability reflects the current economic policy environment: Unlike prior periods of elevated pay losses during the pandemic, unemployment benefits are less generous and eligibility criteria are stricter, meaning that fewer laid-off adults are receiving benefit checks and the checks themselves are smaller.

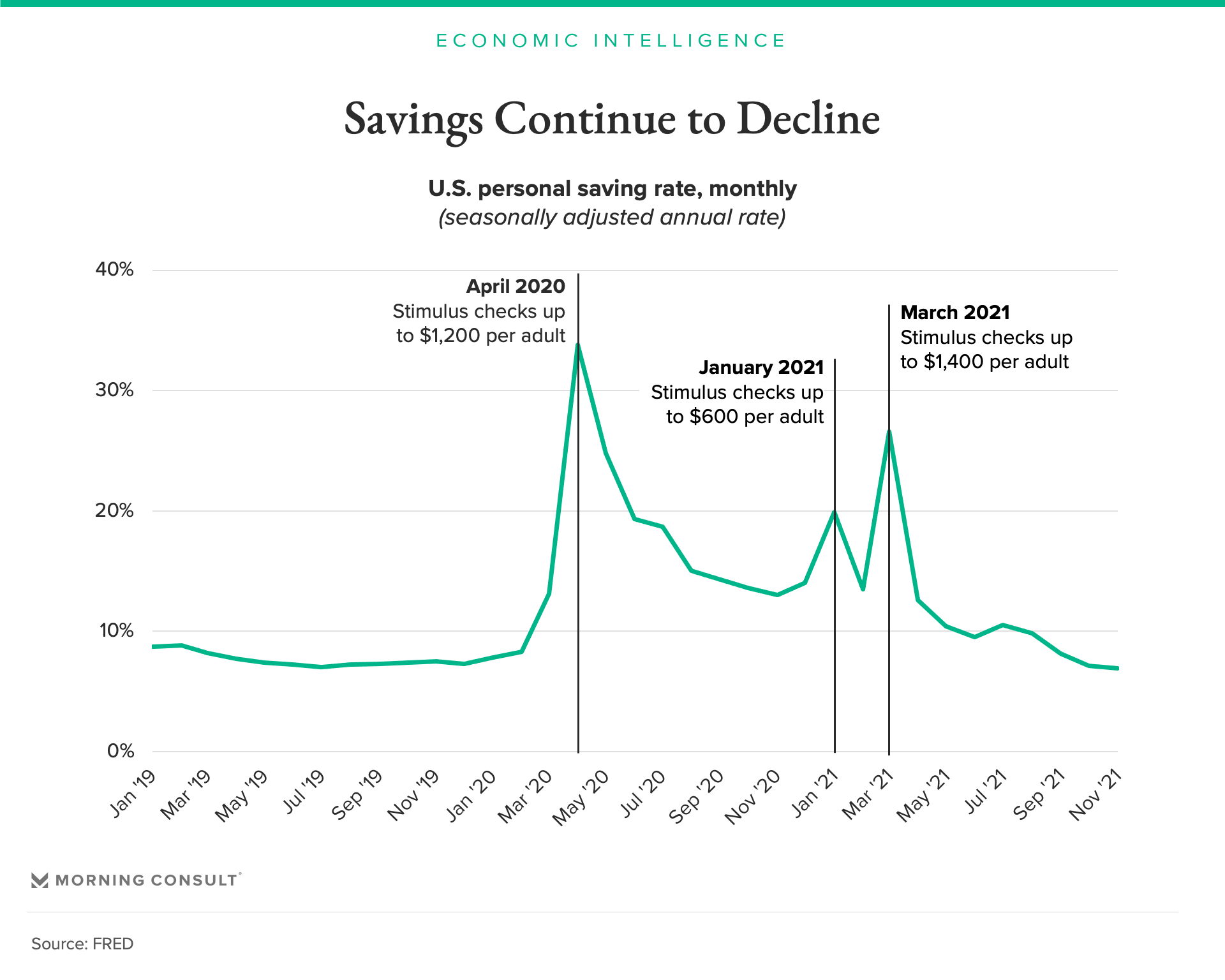

Broadly speaking, Morning Consult’s measure of financial vulnerability is inversely related to the personal savings rate. Both measures show a gradual decrease in savings over the summer of 2020 following the extraordinary measures taken by Congress in the form of stimulus checks and federal unemployment benefits. Additional stimulus in January and March 2021 temporarily drove savings higher and mitigated the 2020-2021 winter surge’s impact on financial vulnerability.

What is unique about Morning Consult’s data is that it captures savings relative to expenses, making it less likely to be skewed by changes in the distribution or concentration of savings. The savings rate does not reflect the distribution of savings in America, whereas Morning Consult’s measure of financial vulnerability identifies adults who are unable to pay their basic expenses for a full month — regardless of the amount in savings that higher-income adults are able to accumulate. Morning Consult’s data also measures stock rather than flow, which makes it more appropriate for assessing the adequacy of savings during a period of elevated layoffs.

Even as the number of daily COVID-19 cases begins to fall in much of the United States, it is going to take longer for workers and consumers to regain their momentum when compared to the delta variant. While consumers remain more resilient to rising cases than they were a year ago, record-setting daily cases combined with policy changes and rising prices will expose Americans’ finances going forward.

John Leer leads Morning Consult’s global economic research, overseeing the company’s economic data collection, validation and analysis. He is an authority on the effects of consumer preferences, expectations and experiences on purchasing patterns, prices and employment.

John continues to advance scholarship in the field of economics, recently partnering with researchers at the Federal Reserve Bank of Cleveland to design a new approach to measuring consumers’ inflation expectations.

This novel approach, now known as the Indirect Consumer Inflation Expectations measure, leverages Morning Consult’s high-frequency survey data to capture unique insights into consumers’ expectations for future inflation.

Prior to Morning Consult, John worked for Promontory Financial Group, offering strategic solutions to financial services firms on matters including credit risk modeling and management, corporate governance, and compliance risk management.

He earned a bachelor’s degree in economics and philosophy with honors from Georgetown University and a master’s degree in economics and management studies (MEMS) from Humboldt University in Berlin.

His analysis has been cited in The New York Times, The Wall Street Journal, Reuters, The Washington Post, The Economist and more.

Follow him on Twitter @JohnCLeer. For speaking opportunities and booking requests, please email [email protected]

Jesse Wheeler previously worked at Morning Consult as a senior economist.