Analysis: More People Got Back to Work in August, but Outlook Dims for Those Still Looking for Jobs

Key Takeaways

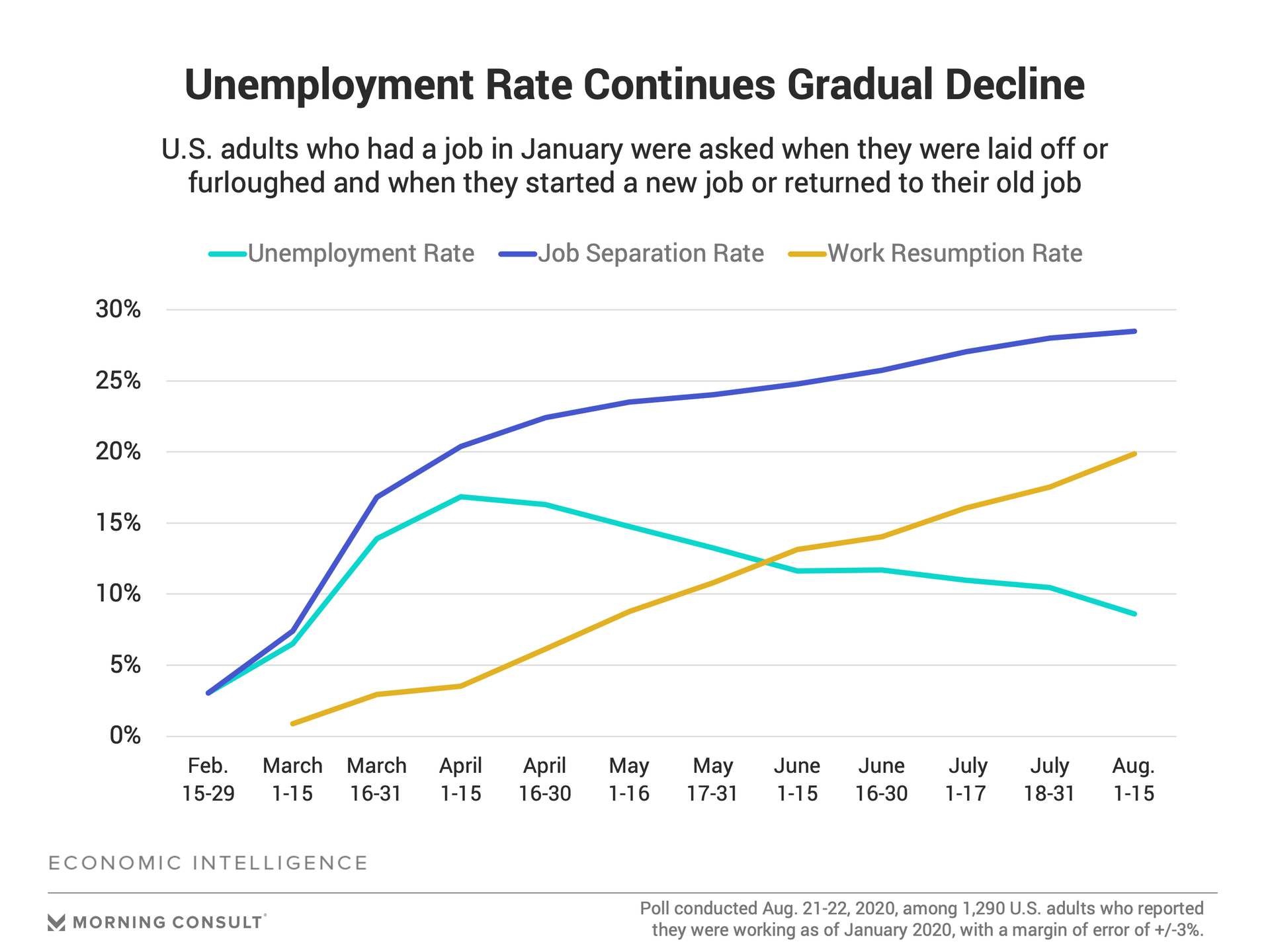

Americans continued to gradually return to work in August, with 8.6% of workers who were employed in January reporting they were out of work in August, down from 11% in the first half of July.

Recent improvements in the demand for labor are creating two distinct employment paths as the economy recovers. On the one hand, a growing share of workers who are now back to work feels secure in their jobs and does not expect to suffer a loss of employment income over the next four weeks. On the other hand, unemployed workers are losing hope of returning to their prior jobs, and 50% of unemployment insurance recipients are unable to cover their basic expenses with the money they receive from UI benefits.

Barring dramatic developments in the spread of the virus, all indicators suggest that U.S. workers are likely to continue experiencing modest employment improvements on average, with unemployed workers likely to experience prolonged unemployment and suffer financial hardship.

Workers in August continued to find work at a faster rate than they were laid off or furloughed, providing yet another signal that the U.S. economy continues to gradually rebound from the depths of the economic fallout induced by the coronavirus pandemic. Morning Consult data suggests most employed workers are well-positioned to keep their current jobs, but it also paints an increasingly grim picture for unemployed workers.

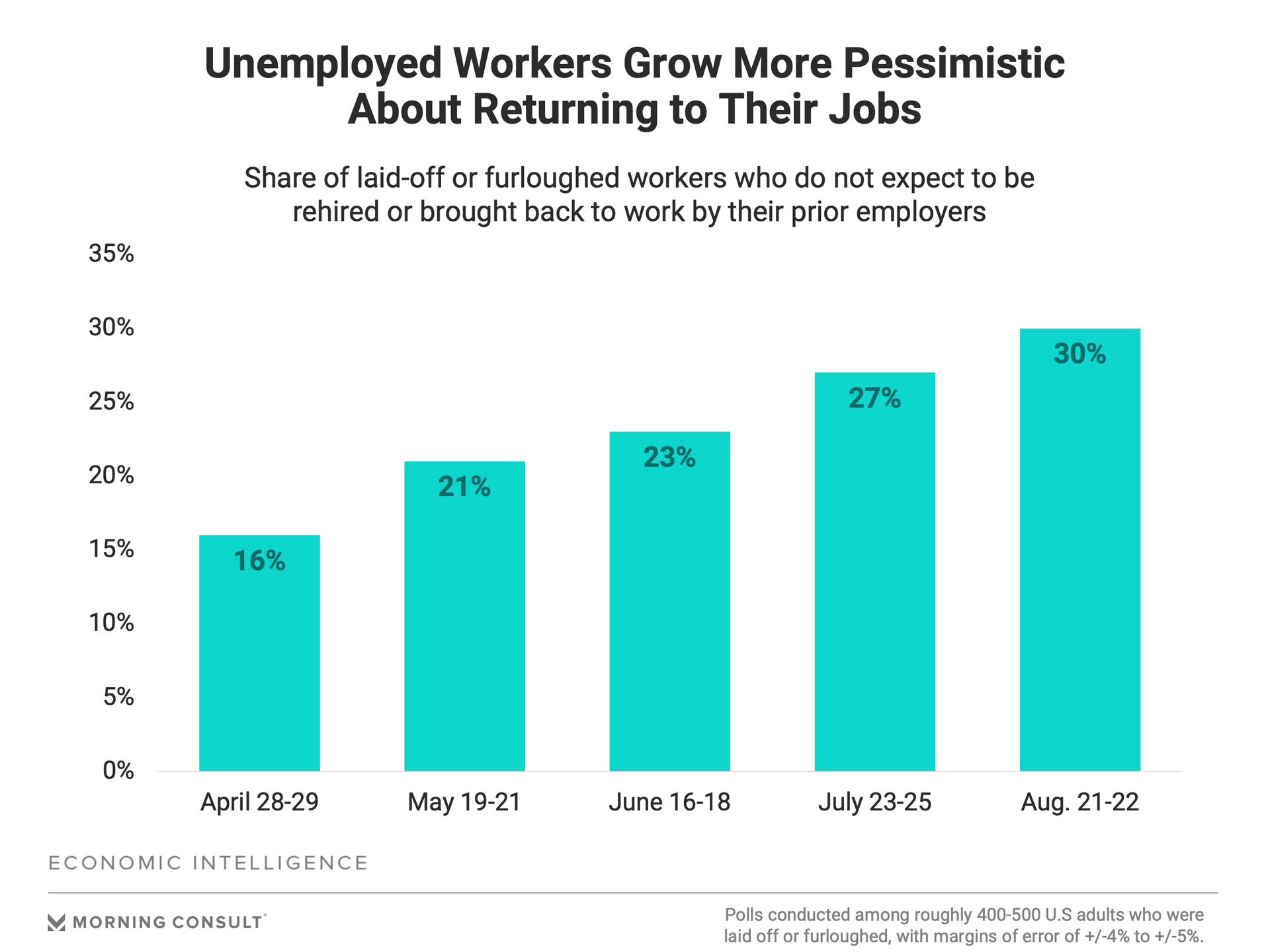

The likelihood of laid-off and furloughed workers returning to their prior employers continues to fall, and given limitations in skills and training, it will become increasingly difficult for them to find work in new industries as they did in July and August. Adding insult to injury, the share of unemployed workers unable to cover their basic expenses with their unemployment benefits rose to 50 percent in August, or an estimated 8.3 million Americans.

While a gradual improvement in employment signals a gradual improvement in consumer spending and the economy over the next six to eight months, the political implications of this data from August could reverberate as early as November. If President Donald Trump and the incumbent Republicans can convince voters that they are aptly managing the economy, it will become easier to argue in favor of their re-election. The likelihood of a rapid jobs recovery seems like a remote possibility at this point, but gradual improvements in August may be enough to make that case to the American public.

The findings in this analysis are based on five separate Morning Consult surveys using similar questions to produce monthly trends. The first survey was conducted April 28-29, the second May 19-21, the third June 16-18, the fourth July 23-25, and the fifth Aug. 21-22. All five surveys relied on a representative sample of 2,200 U.S. adults, weighted to match age, gender, educational attainment and region. Each of the surveys’ margins of error is 2 percentage points.

Demand for labor strengthens, but indicators of future improvements weaken

Based on Morning Consult’s survey research, the unemployment rate in August likely dropped below 10 percent for the first time since late March, indicating a gradual improvement in the demand for labor since the prior month.

Americans continued to gradually return to work in August, with 8.6 percent of workers who were employed in January reporting they were out of work in August, down from 11 percent in the first half of July.

The chart above tracks the employment status of 1,290 U.S. adults who reported that they were working as of January. The Aug. 21-22 survey asks these adults to indicate major changes to their employment status from Feb. 15 to Aug. 15 using roughly two-week intervals.

In the chart above, the purple line tracks workers who either lost their jobs or were placed on temporary leave, showing that the increases in late July and early August are modest, and the yellow line tracks workers who returned to work or found a new job after being fired or furloughed sometime since Feb 15. Unlike the job separation rate, which exhibits an asymptotic shape, the work resumption rate remains linear.

The difference between these two lines is the unemployment rate. As the yellow line approaches the purple line, the unemployment rate continues to decrease.

The trend in the unemployment rate from March--July is consistent with the U-3 rate (or unemployed people actively seeking a job) reported by the Bureau of Labor Statistics, especially after taking into account the magnitude of the misclassification errors in April and May. From a theoretical perspective, the unemployment values in the chart below likely understate the level of the unemployment rate since they do not consider adults who were unemployed in January 2020 and are looking for a job, as well as recent college graduates who entered the labor force in June or July.

In terms of predicting future developments in unemployment, there are two fairly simple questions. First, will the purple line continue to flatten or might it increase? Second, will the yellow line continue its positive linear path or might the rate of work resumption slow in the coming months?

Looking at the purple line: Will job separations accelerate?

The strength of the jobs recovery critically depends on the number of employed Americans who will be laid off or furloughed in the coming months. While April was a terrible month for workers, the steady drumbeat of new claims for unemployment insurance indicates that workers continue to lose their jobs.

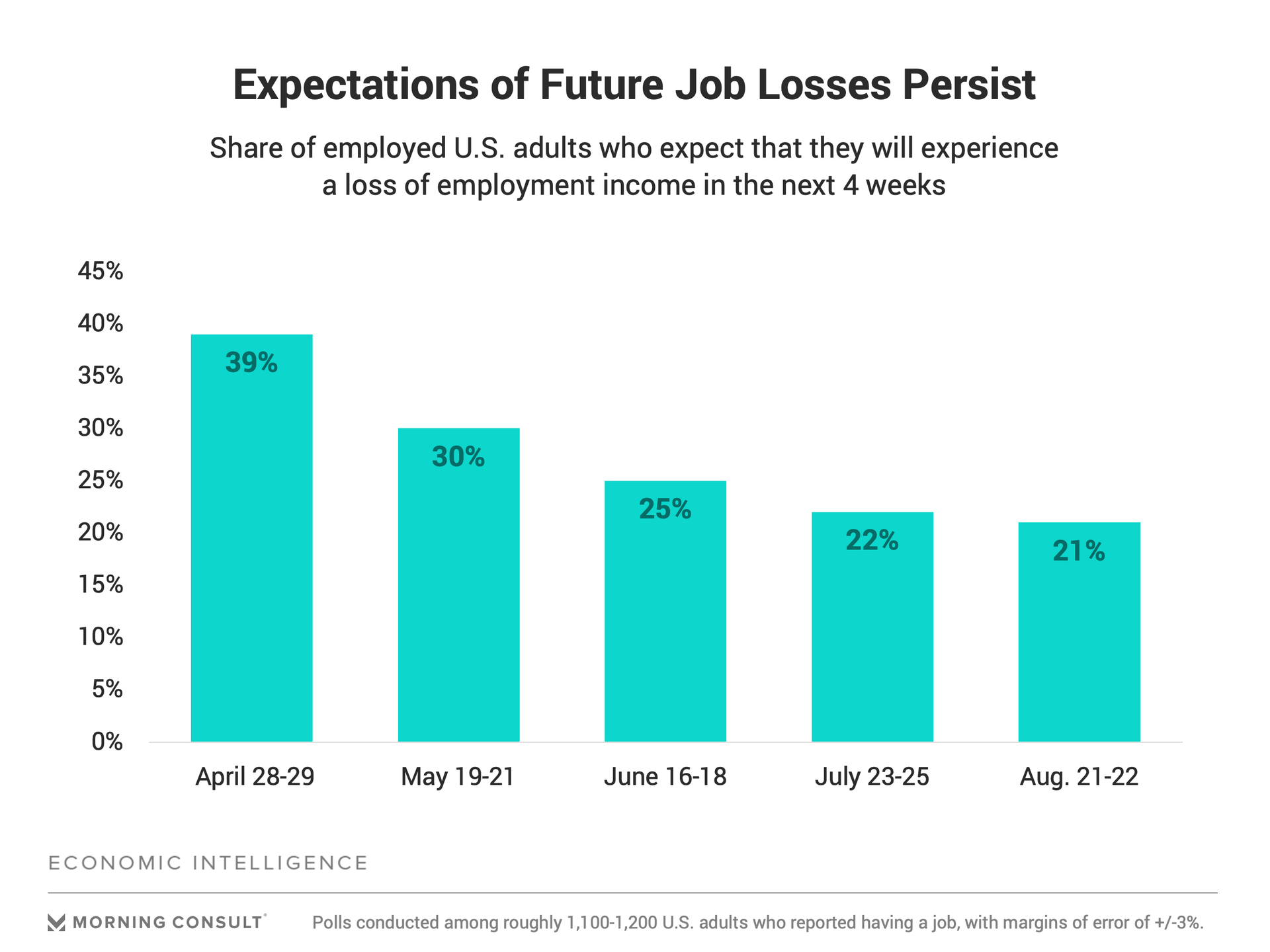

One simple way to estimate future job separations is by asking workers whether or not they expect to experience a loss of employment income in the next four weeks. Employment income is a broader measure of job security than employment alone since some workers may have their hours cut or pay reduced without being fired.

Perceptions of job security moderately improved in August, but the rate of increases has stalled. The share of employed adult Americans who expect to experience a loss of employment income in the next four weeks dropped 1 percentage point in August from the month prior to 21 percent. The numbers in July and August remain well below the 39 percent recorded in April, but the trend over the past five months indicates a slowdown in the decrease in job insecurity.

Added employment stability is a positive sign for consumer spending and the economy. It allows workers to make future spending plans, which tends to drive durable goods purchases.

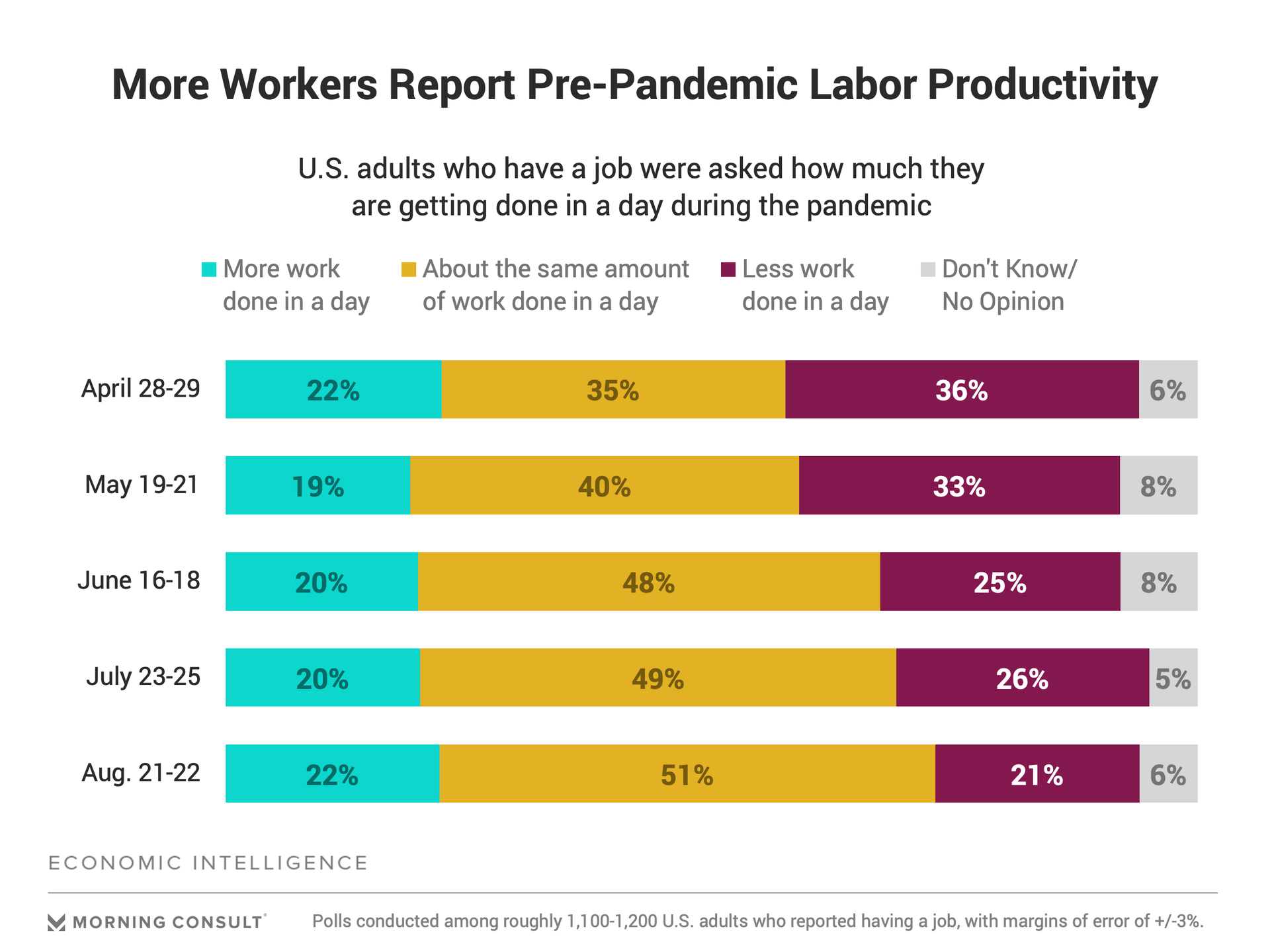

Developments in labor productivity corroborate workers’ perceptions of their job security. Employers use labor productivity to inform their hiring and firing decisions. If workers cannot get as much work done in a given day as they could before the virus, then it becomes relatively more expensive for employers to keep paying them.

Quarterly labor productivity numbers reported by the Bureau of Labor Statistics do not control for changes in the composition of the workforce. During a typical recession, employers lay off or furlough their least productive workers, meaning almost by definition that labor productivity numbers from the BLS during the onset of a recession do not reflect the full impact of the recession.

The chart below shows that 51 percent of workers get about the same amount of work done in a given day as they did prior to the onset of the pandemic, up from 35 percent in April.

The red bar in the chart above shows those workers who report getting less done in a given day since the onset of the pandemic. As workers grew more comfortable working from home and dealing with additional social distancing protocols at work, the share of workers reporting that they were less productive consistently decreased from April to August.

The challenge for the 21 percent of workers who continue to report being less productive now than they were prior to the onset of the pandemic is that employers are most likely to identify them as candidates for additional layoffs. Thus, one of the reasons why some workers may remain concerned about their future employment prospects is that they know deep down inside that they are not as productive during the pandemic as they were prior to its onset.

Looking at the yellow line: Will work resumption continue its linear path?

Since April, millions of laid-off and furloughed workers have returned to work. However, there are a few reasons for being less optimistic about the future path of work resumption. First, laid-off and furloughed workers grew less optimistic about their chances of being rehired by their prior employers in August. As of August, 30 percent of laid off or furloughed workers did not believe they would be rehired by their prior employers. This data is consistent with recent news releases from major employers indicating that temporary furloughs are likely to become permanent layoffs.

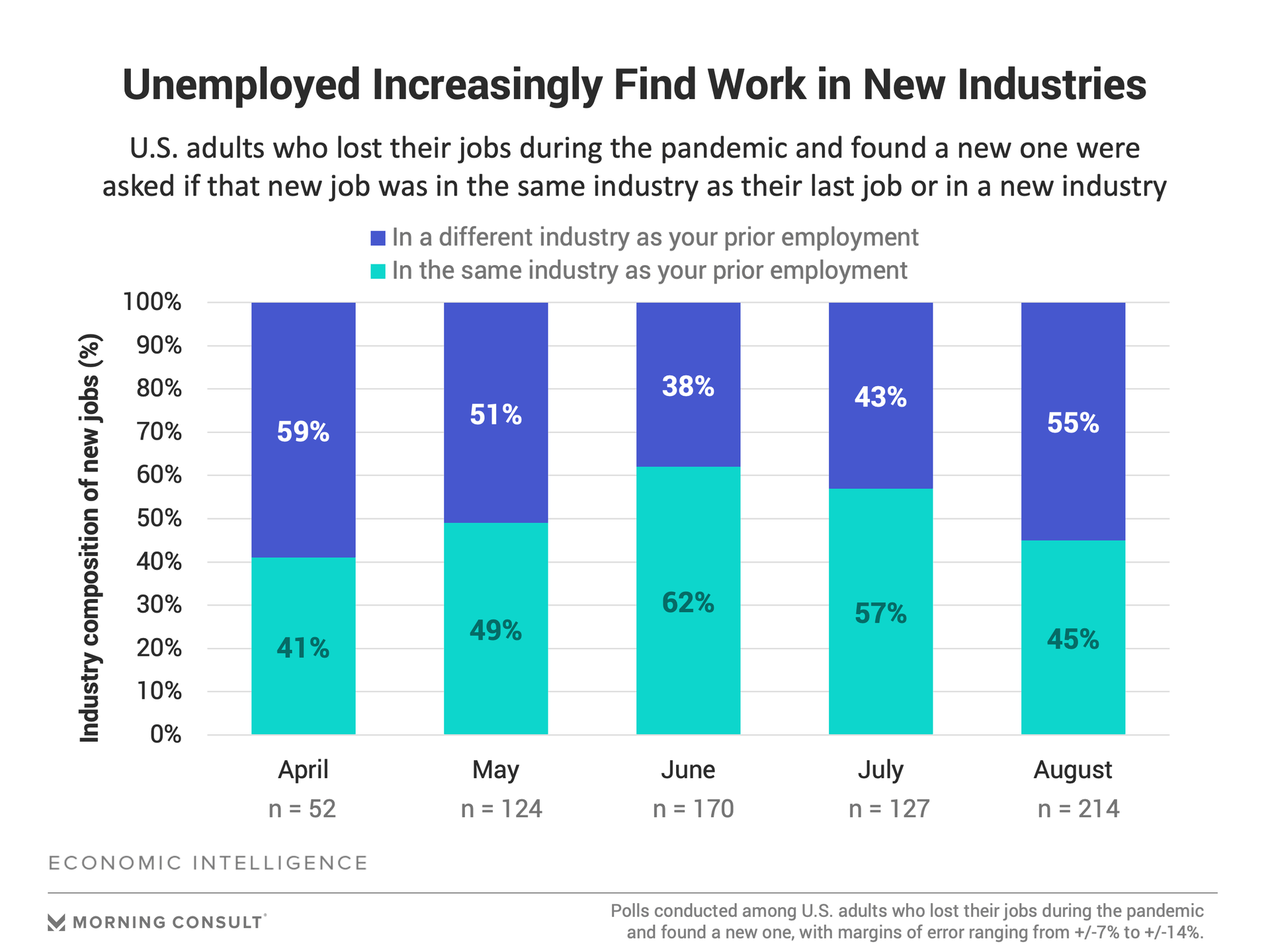

As laid-off and furloughed workers grew less optimistic about returning to their prior employers, workers who found a new job in August were more likely to do so in a new industry. As of August, 55 percent of laid-off and furloughed workers who found a new job since the onset of the pandemic did so in a new industry.

The data from August continues the trend that began in July. Unemployed workers are increasingly looking for new industries to find work as they grew less optimistic in their ability to return to their prior employers.

While industry switching is a positive development, it remains unclear how many workers will be able to transition to a new industry given their existing skills and education. Widespread industry switching typically requires substantial training and skills development programs, suggesting that the trend in August is unlikely to provide a scalable solution of the millions of Americans who remain unemployed in the short run.

As growing share of unemployed struggle to pay bills, most Americans’ finances improve in August

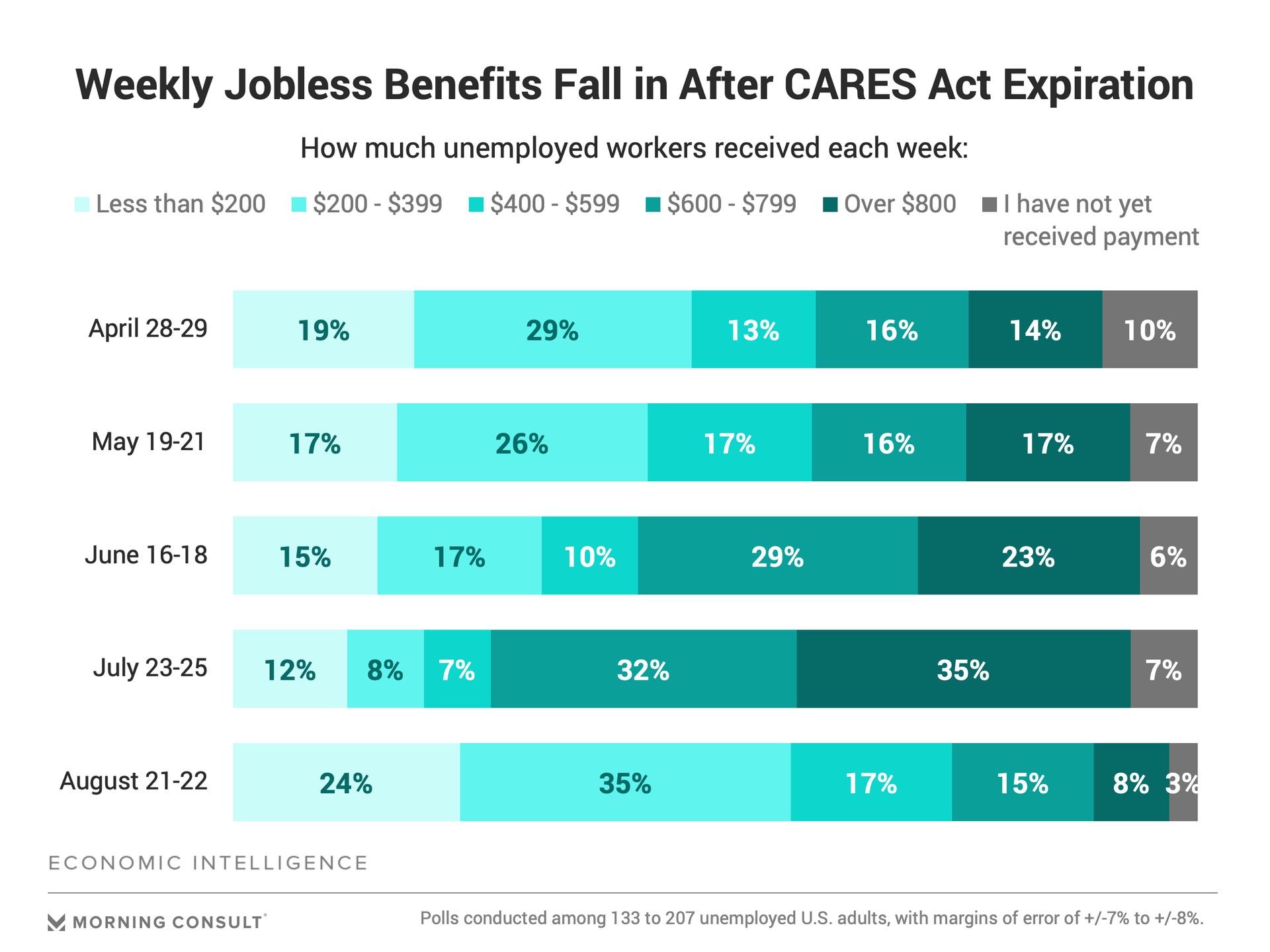

Not only are Americans who remain unemployed increasingly less likely to find new work, the recent expiration of the weekly $600 supplemental unemployment insurance (UI) benefits included in the CARES Act jeopardizes their finances. While Trump signed an executive order granting unemployed workers an additional $300 per week, Morning Consult’s data indicates a dramatic drop in weekly unemployment benefits, with the modal range shifting from over $800 per week in July to between $200 and $399 in August.

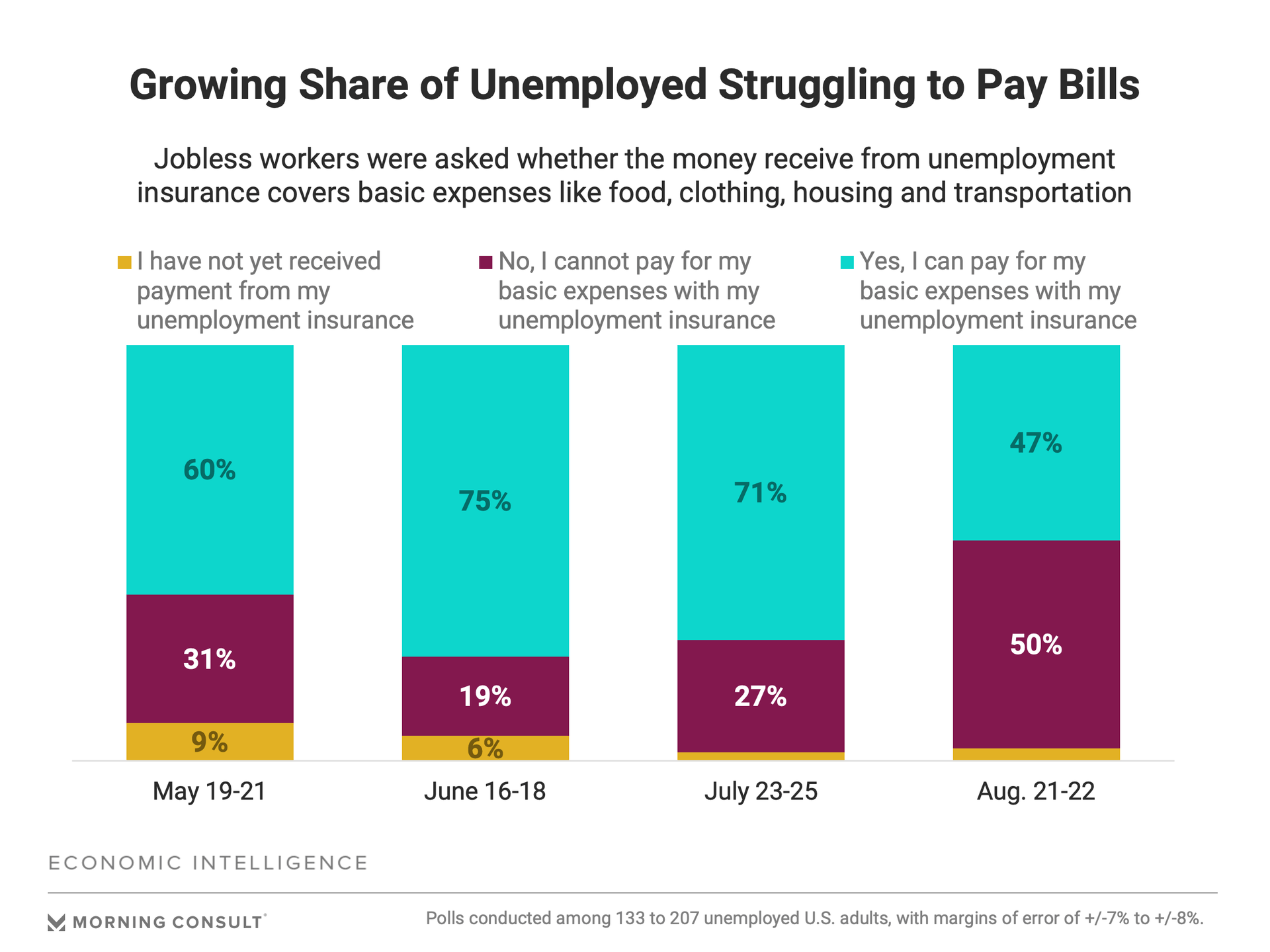

Not surprisingly, more workers receiving UI benefits said that they were unable to pay for basic monthly expenses using the money from unemployment insurance. In August, 50 percent of UI recipients were unable to pay for their basic expenses using their UI benefits, up from 27 percent in July.

As of Aug. 31, 16.6 million Americans received weekly unemployment insurance benefits (continuing claims plus initial claims), meaning that roughly 8.3 million Americans were unable to cover their basic household expenses with their UI benefits.

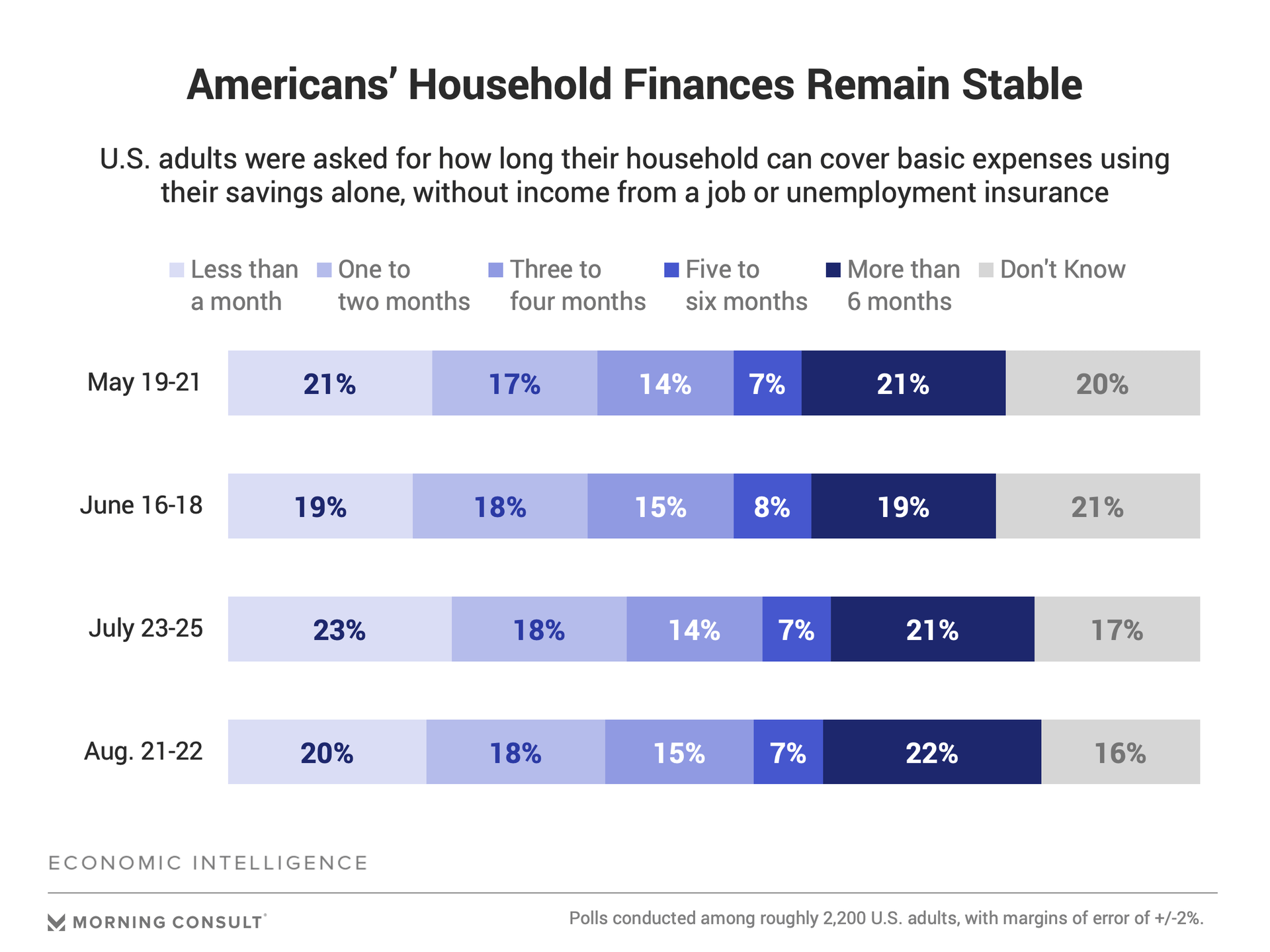

Weaknesses in household balance sheets remain limited to those who have experienced a persistent loss of employment since the onset of the pandemic. Looking at household finances more generally, the aggregate picture moderately improved in August, with a smaller share of households able to cover their living expenses with their savings for less than a single month. Thus far, there is no evidence of a pervasive deterioration in Americans’ finances.

While the trends over time since May remain relatively stable, the distribution of households’ finances sheds light on potential financial vulnerabilities in the United States. As of August, 20 percent of American adults were unable to cover basic living expenses with their savings for a single month. As the economy gradually recovers from the pandemic, these Americans remain at high risk of experiencing financial hardship, and additional deterioration in their finances has the potential to jeopardize the ongoing gradual economic recovery for the country as whole.

John Leer leads Morning Consult’s global economic research, overseeing the company’s economic data collection, validation and analysis. He is an authority on the effects of consumer preferences, expectations and experiences on purchasing patterns, prices and employment.

John continues to advance scholarship in the field of economics, recently partnering with researchers at the Federal Reserve Bank of Cleveland to design a new approach to measuring consumers’ inflation expectations.

This novel approach, now known as the Indirect Consumer Inflation Expectations measure, leverages Morning Consult’s high-frequency survey data to capture unique insights into consumers’ expectations for future inflation.

Prior to Morning Consult, John worked for Promontory Financial Group, offering strategic solutions to financial services firms on matters including credit risk modeling and management, corporate governance, and compliance risk management.

He earned a bachelor’s degree in economics and philosophy with honors from Georgetown University and a master’s degree in economics and management studies (MEMS) from Humboldt University in Berlin.

His analysis has been cited in The New York Times, The Wall Street Journal, Reuters, The Washington Post, The Economist and more.

Follow him on Twitter @JohnCLeer. For speaking opportunities and booking requests, please email [email protected]