July’s U.S. Economic Outlook: Waiting for Liftoff

Key Takeaways

Employment growth is the key to driving the U.S. economy during the second half of the year, and labor force growth in June signals that workers are starting to re-enter the labor force after dropping out during the pandemic.

While waiting for increases in employment to fuel growth in consumption, the most relevant trends in consumer spending will be in terms of how consumers allocate their wallet rather than adjustments to the total size of their wallets.

The termination of unemployment benefits may help drive increases in employment, but it also jeopardizes the strength of households’ balance sheets and the rebound in consumer spending.

The following analysis is based on Morning Consult’s high frequency economic indicator data. Read more from our July 2021 U.S. Economic Outlook report.

After a sluggish May, the U.S. economy laid the foundation in June for liftoff later this year. Americans are slowly going back to work and returning to look for work, but the rapid jobs recovery many economists expected remains elusive. Built-up savings will provide some consumers a backstop against prolonged unemployment, but a growing share of adults has already depleted the financial cushion provided by stimulus checks.

Employment

The near-term trajectory of the U.S. economy most critically depends on increasing employment, but noise in some of the traditional data sources obscures the underlying signal.

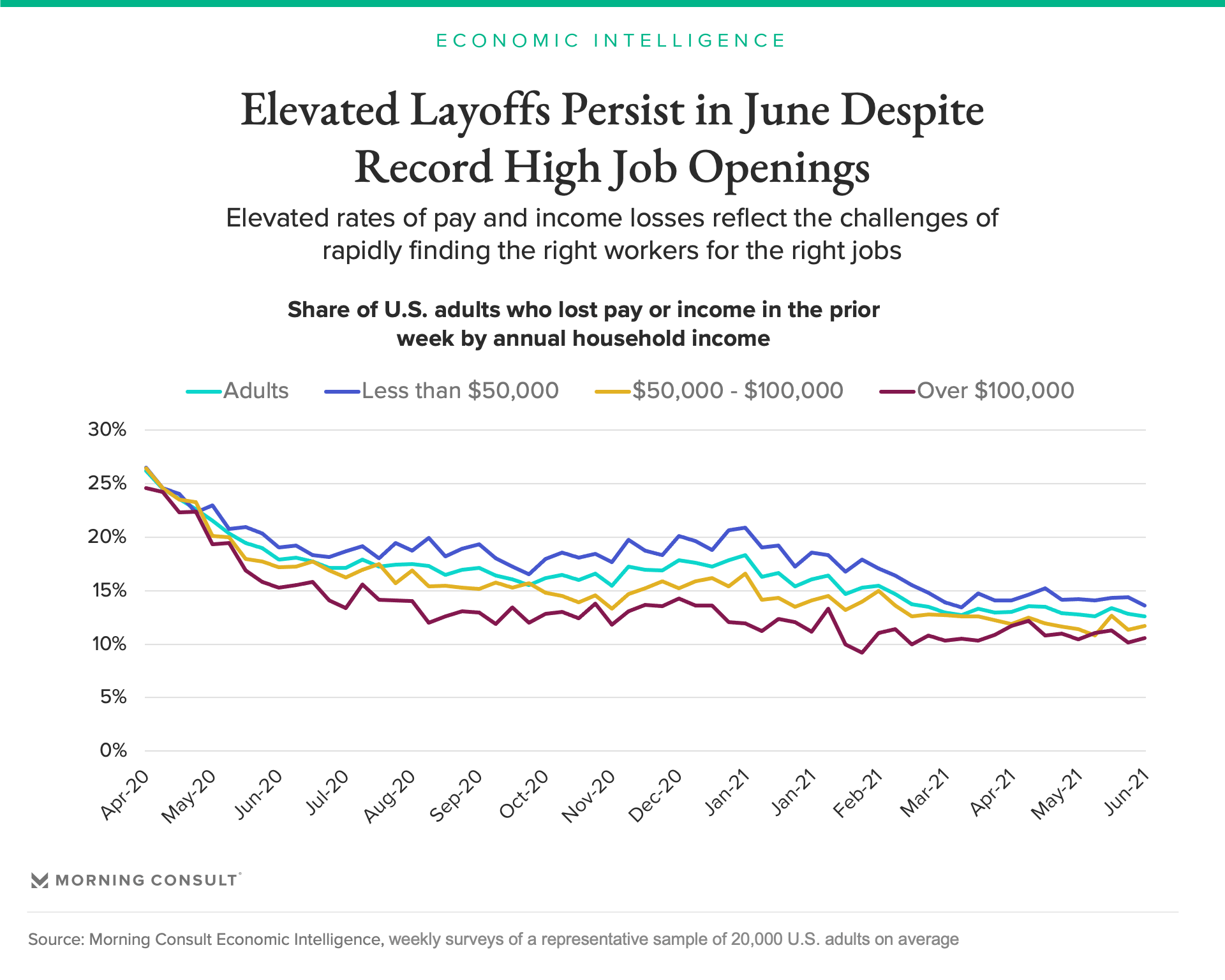

Employers and workers are likely to experience an elevated level of employment churn. The share of Americans experiencing a loss of pay or income remained essentially unchanged during the first three weeks of June, a trend likely to continue given the high number of workers forced to find new jobs. Don’t be fooled by falling weekly unemployment claims: A decrease in benefits and benefit eligibility is not the same as improving demand for workers.

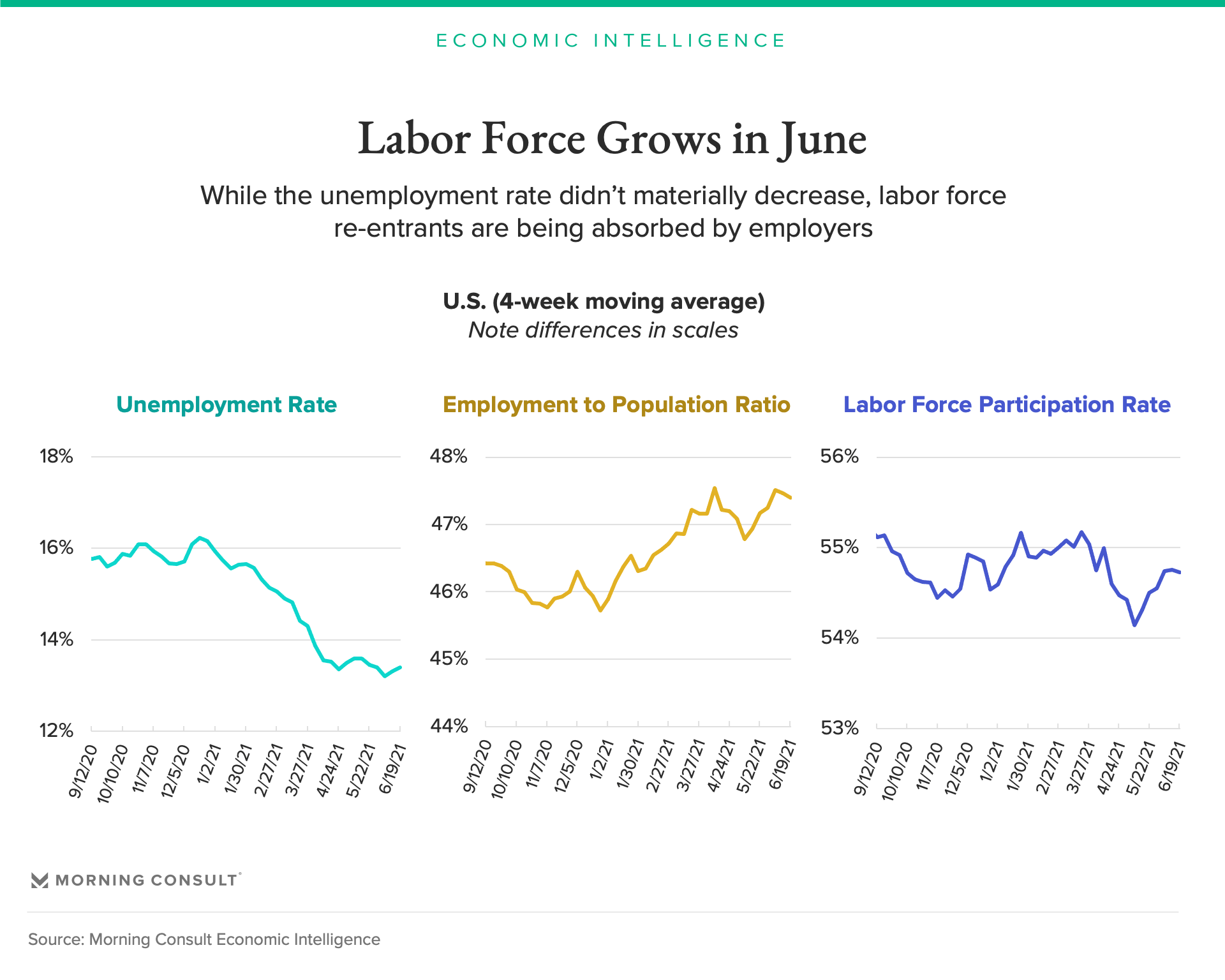

While improvements in Morning Consult’s unemployment rate remained modest in June, the more significant development was the increase in labor force participation. More Americans are either working or looking for work, with most of the improvements coming from students and retirees.

Those conventional employment measures omit how confident employed workers feel about their current positions. Fears of future pay losses fell again in June, with 13.0% of employed workers expecting a loss of employment income sometime in the next four weeks, down from 19.1% in April. This added level of job security led a greater share of employed workers to actively search for other positions in June, particularly among low-income workers.

Consumer confidence

Morning Consult’s daily U.S. Index of Consumer Sentiment remained essentially unchanged over the course of the month, indicating that consumer spending and retail sales did not materially change in June. Looking ahead, consumers are unlikely to significantly revise their views of the economy or increase total spending until a greater share of Americans get back to work. High-income Americans are likely to divert a greater share of income to consumption rather than stockpile it as savings. For low-income consumers, the expiration of unemployment benefits may push some back to work, but it also risks decreasing the money flowing into the economy.

Share of wallet

The most relevant trends in consumer spending will be in terms of how consumers allocate their wallet rather than adjustments to the total size of their wallets. Americans continue to grow more comfortable engaging in basic economic activities, particularly airline travel. Consumers are spending on trips and vacations rather than on automobiles and other durable goods. However, those cars and suburban houses that Americans purchased during the pandemic will leave a lasting impact on consumption patterns. Expect increased car-related spending and time spent outside urban areas to remain features of the economy even after the pandemic.

Personal finances

Americans’ personal finances remained strong in June, but the benefits from unprecedented fiscal stimulus have begun to erode. The share of Americans unable to pay their bills increased in May, leaving a greater share of consumers in June without adequate savings. As federal unemployment insurance benefits expire over the next three months, low- and middle-income workers are likely to continue to draw down their savings as they look for jobs. But high-income adults relied on credit card debt in May to finance their spending, yet another sign that they anticipate a steady income.

Read more from our July report on the U.S. economic outlook.

John Leer leads Morning Consult’s global economic research, overseeing the company’s economic data collection, validation and analysis. He is an authority on the effects of consumer preferences, expectations and experiences on purchasing patterns, prices and employment.

John continues to advance scholarship in the field of economics, recently partnering with researchers at the Federal Reserve Bank of Cleveland to design a new approach to measuring consumers’ inflation expectations.

This novel approach, now known as the Indirect Consumer Inflation Expectations measure, leverages Morning Consult’s high-frequency survey data to capture unique insights into consumers’ expectations for future inflation.

Prior to Morning Consult, John worked for Promontory Financial Group, offering strategic solutions to financial services firms on matters including credit risk modeling and management, corporate governance, and compliance risk management.

He earned a bachelor’s degree in economics and philosophy with honors from Georgetown University and a master’s degree in economics and management studies (MEMS) from Humboldt University in Berlin.

His analysis has been cited in The New York Times, The Wall Street Journal, Reuters, The Washington Post, The Economist and more.

Follow him on Twitter @JohnCLeer. For speaking opportunities and booking requests, please email [email protected]