Navigating U.S.-China Relations: What American and Chinese Multinationals Need to Know

This is a preview of Morning Consult’s inaugural report “The State of U.S.-China Relations.” Download the full report here.

Four years into a trade war and amid persistent security tensions in the Asia-Pacific region, the current state of U.S.-China relations poses both risks and opportunities for U.S. and Chinese multinationals. While the outlook for improved bilateral relations is grim, there are still openings to do business in each other’s markets.

Our inaugural quarterly report “The State of U.S.-China Relations” provides trans-Pacific business leaders with actionable, data-driven insights into these dynamics through an in-depth analysis of U.S. and Chinese sentiment toward trade and tariffs, cross-border investment flows, “Made in America” and “Made in China” goods, reshoring by U.S. and Chinese multinationals, corporate exposure to reputational risks, and more.

Here's what business leaders need to know:

1. U.S. and Chinese adults want improved bilateral relations

Adults on both sides of the Pacific forecast that bilateral tensions will escalate for the foreseeable future. But strong public interest in improving U.S.-China relations will help guard against the worst excesses of bilateral competition: a cold war characterized by a return to economic autarky, or a hot one marked by direct military conflict.

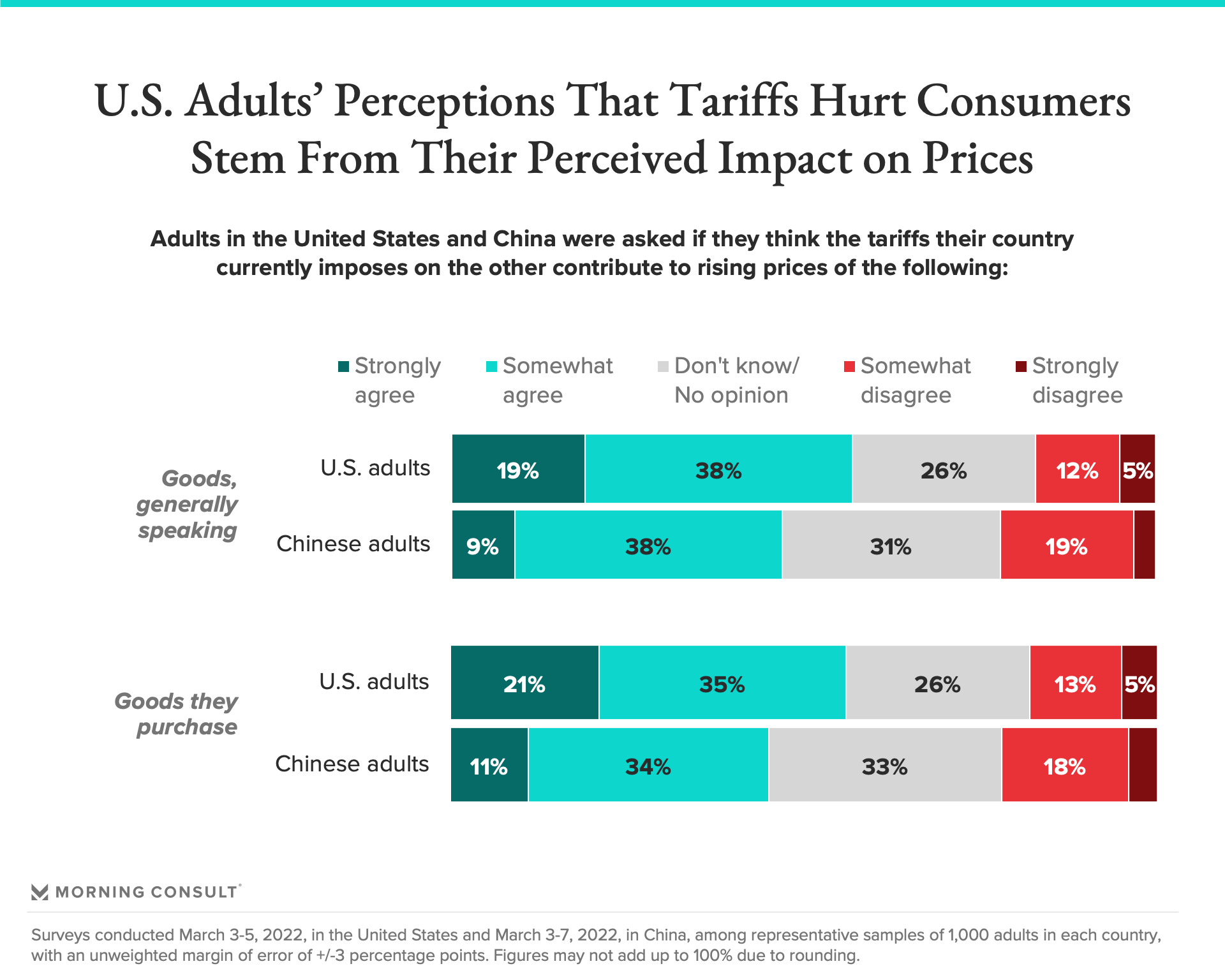

2. Political developments in late 2022 will provide a near-term opening for tariff relief

A majority of U.S. adults and a plurality of Chinese adults believe bilateral tariffs have contributed to rising prices in their country. As a result, sizable shares of both groups continue to buy fewer goods. Amid historically elevated U.S. inflation and a wavering Chinese economy, Presidents Biden and Xi will face heightened political incentives to respond to these dynamics by scaling back tariffs ahead of the U.S. midterm elections and the Chinese Communist Party’s 20th National Congress, both in late 2022. A more promising opening for U.S. and Chinese multinationals to seek tariff relief is unlikely to materialize — so they should seize the moment while they can.

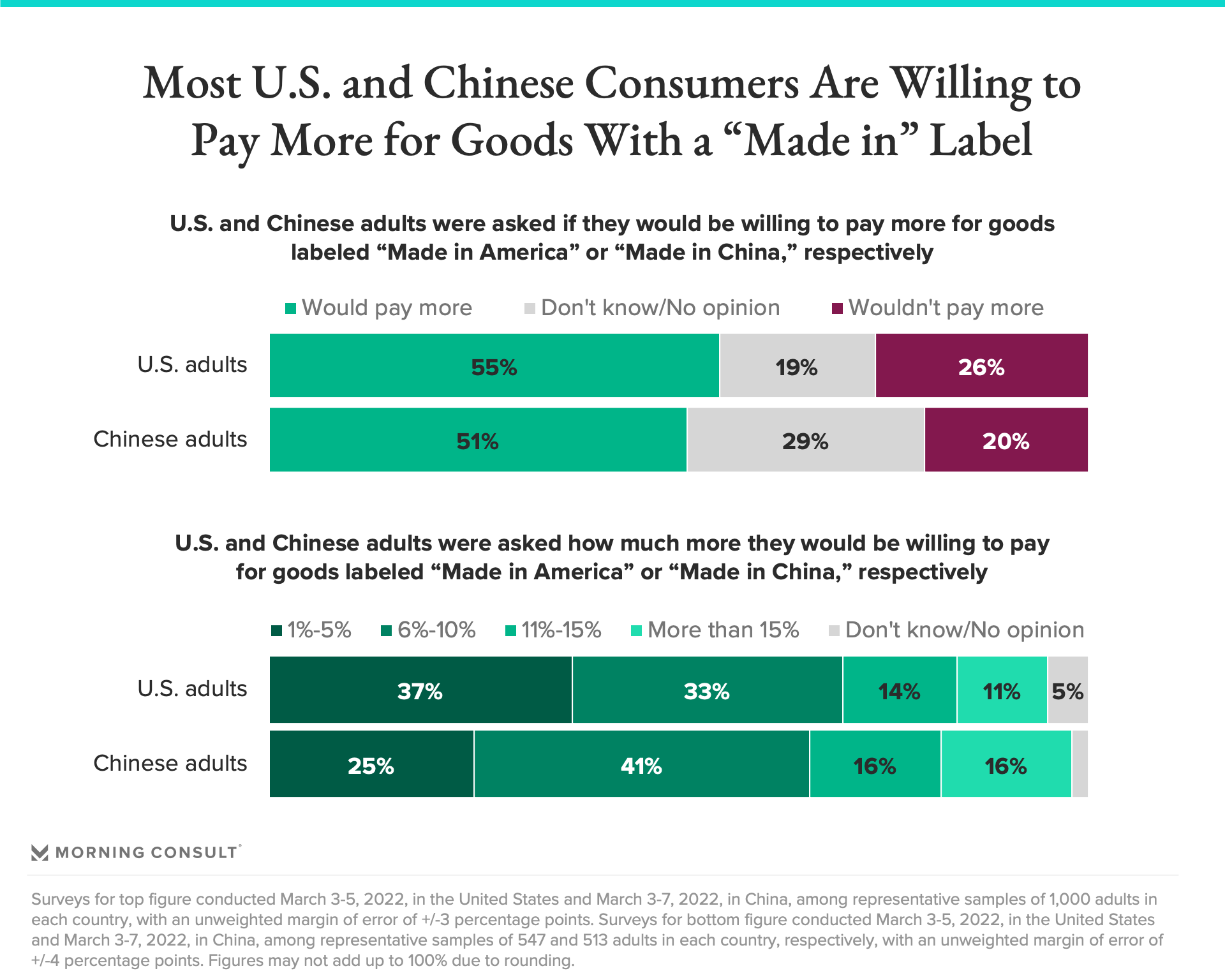

3. Consumer appetite for “made in” goods is strong, but price hesitancy will limit revenue-generating opportunities for both American and Chinese companies

Majorities of U.S. and Chinese consumers say they intentionally purchase “made in” goods sold in their respective countries at least some of the time and are willing to pay a premium for them. But among those willing to pay extra, only around one-quarter say they would pay more than 10% above the usual sticker price. These dynamics will limit market opportunities for multinationals whose transition to a “made in” supply chain would entail substantial costs.

4. U.S. multinationals stand to gain more from reshoring stateside than their Chinese counterparts, while reshoring to China makes less sense for both

Higher shares of U.S. adults are willing to pay more for reshored goods produced by American multinationals than Chinese ones, and most U.S. consumers are unwilling to pay more for reshored goods produced by Chinese companies. American companies that can ramp up their supply chains for “Made in America” products while keeping costs low should do so.

In China, the share of consumers willing to pay more for reshored goods is smaller on average, and Chinese consumers exhibit similar price hesitancy to U.S. consumers. As a result, reshoring to China makes less sense for companies of all stripes.

5. American multinationals’ responses to political pressures involving China go largely unnoticed by U.S. consumers

U.S. multinationals facing reputational risks stemming from their business operations in China can rest easy for the moment: U.S. consumers aren’t paying much attention and don’t especially care how companies respond. Moreover, their purchasing considerations aren’t meaningfully affected by U.S. multinationals’ responses to bilateral political headwinds, suggesting that the risk of material fallout is also limited at present.

Download the full report for deeper insight into these and other issues, and for guidance on how best to navigate the U.S. and Chinese markets amid persistent tensions between the world’s two superpowers.

Jason I. McMann leads geopolitical risk analysis at Morning Consult. He leverages the company’s high-frequency survey data to advise clients on how to integrate geopolitical risk into their decision-making. Jason previously served as head of analytics at GeoQuant (now part of Fitch Solutions). He holds a Ph.D. from Princeton University’s Politics Department. Follow him on Twitter @jimcmann. Interested in connecting with Jason to discuss his analysis or for a media engagement or speaking opportunity? Email [email protected].