Key Takeaways

While some mistakenly attribute increased spending in food- and grocery-related categories to panic buying, new Morning Consult research reveals a more nuanced story, with three primary reasons driving increased purchasing.

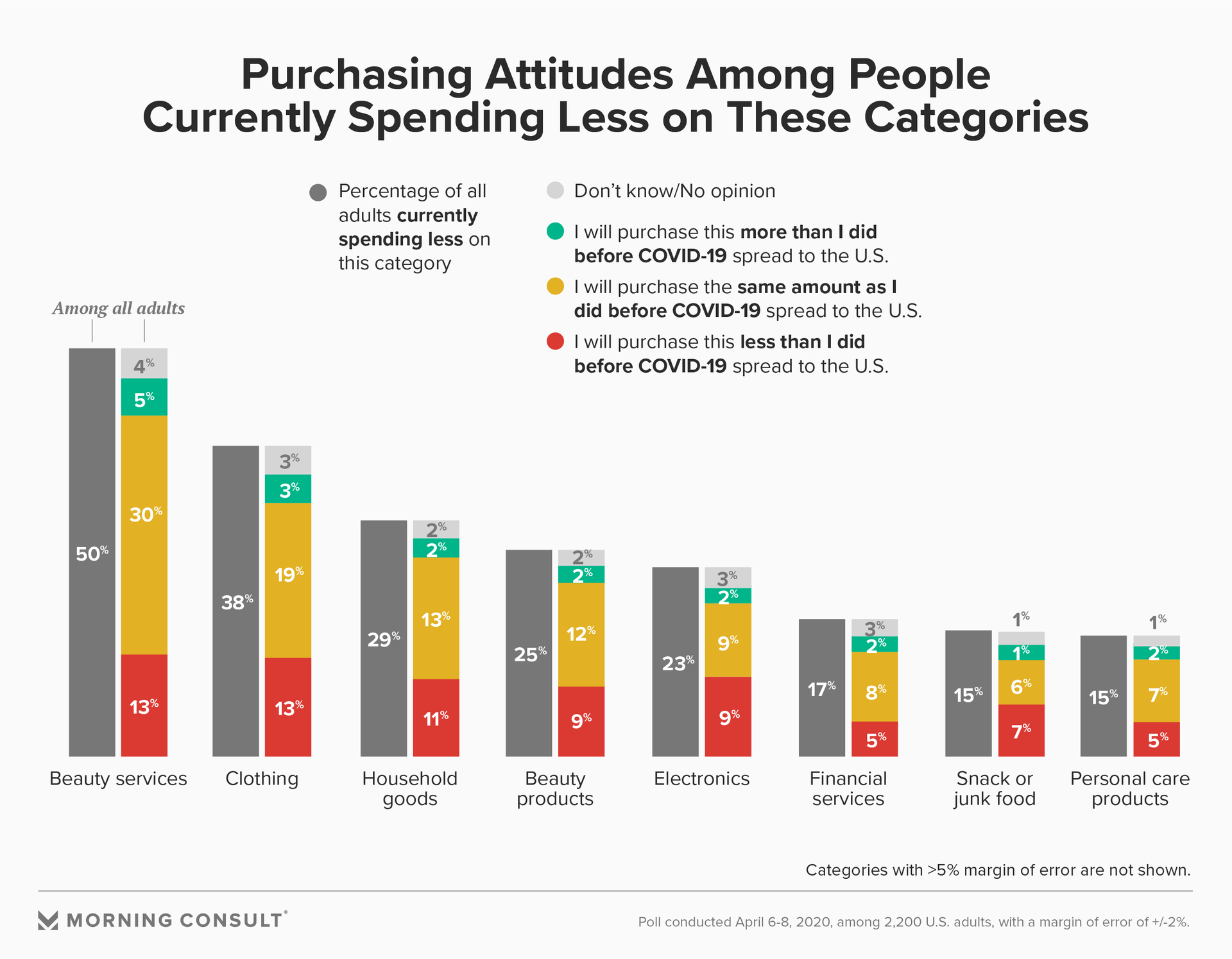

Unsurprisingly, spending on beauty services, clothing, beauty products, household goods and electronics is down since the coronavirus outbreak.

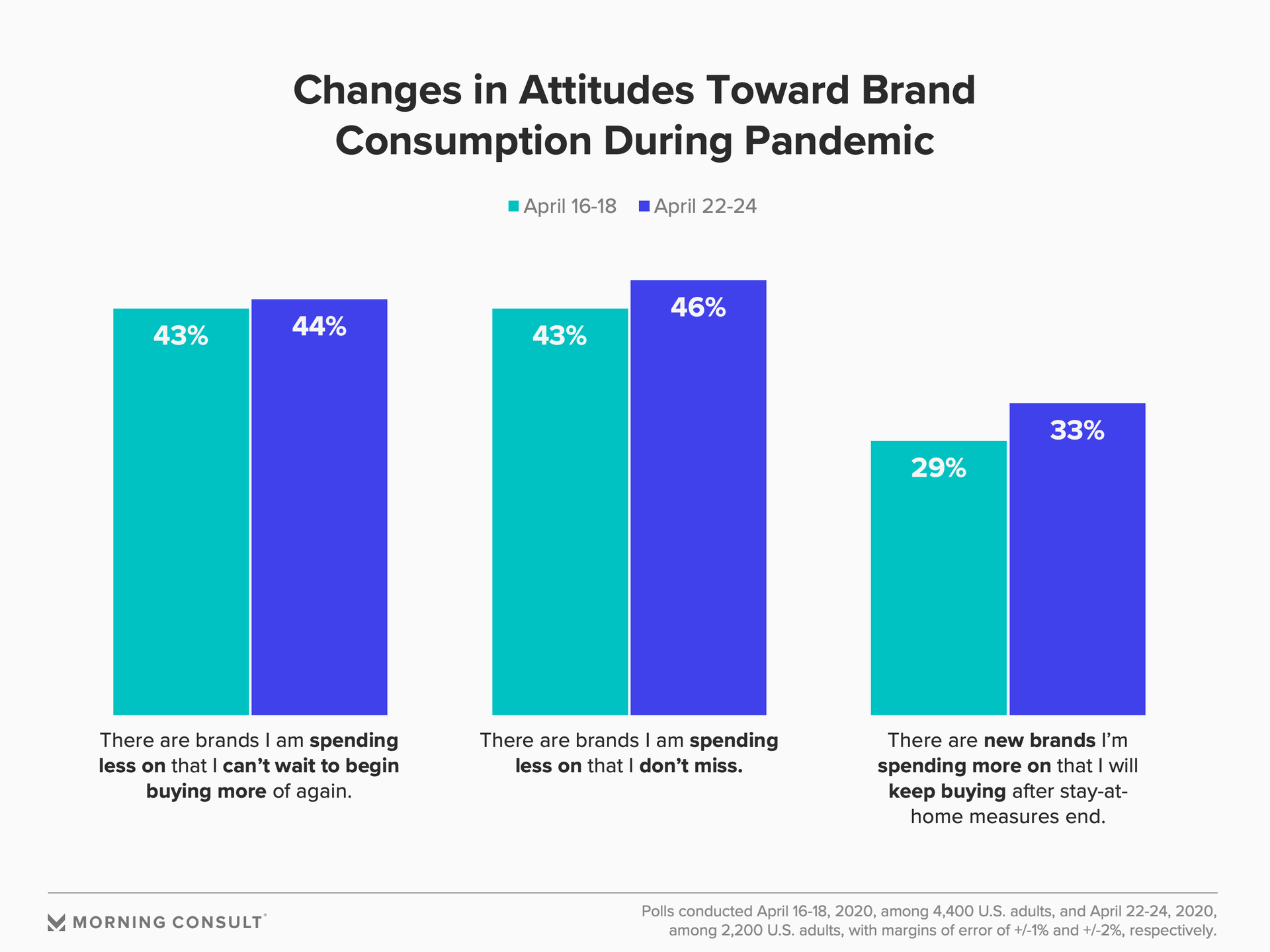

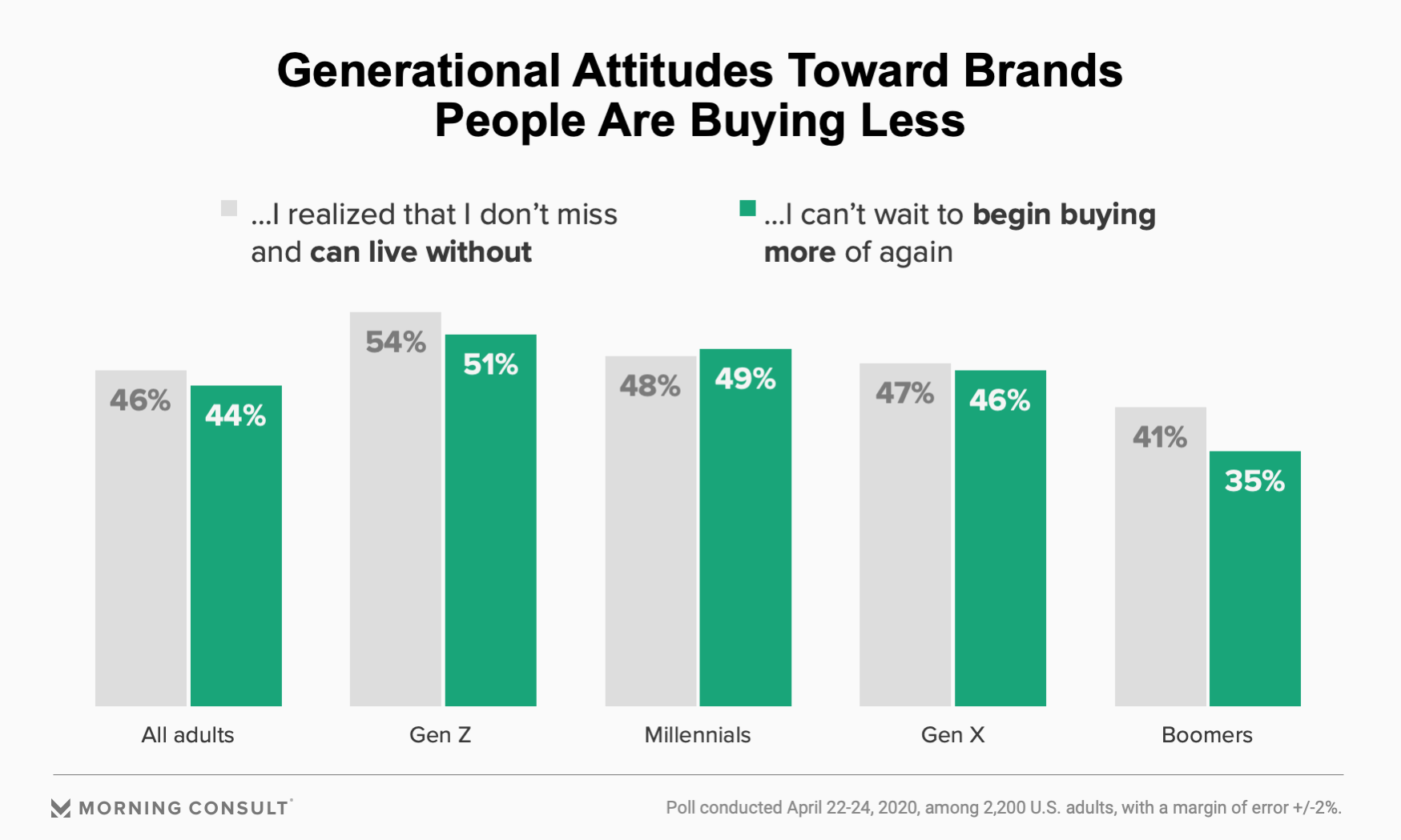

44% of American adults can’t wait to begin buying brands they’re currently spending less on again, but 46% have realized that they don't miss these items and would be fine living without them post-pandemic -- a sentiment that’s only strengthened in the last few weeks.

Morning Consult’s “Favorited or Forgotten” series explores if – and how – consumer behavior will change in a post-COVID-19 world and what brand and business leaders can do to prepare for those changes.

In a time when consumption of preferred products and services has been handicapped by stay-at-home mandates, store closures and out-of-stock issues, American consumption patterns have changed significantly on a category level. But with this unique situation, consumers also have more time to reflect on their purchases -- namely items they typically purchase but are now buying less of, and the new brands they’re buying. Morning Consult took a closer look at not just what people are buying more, but why they are buying more -- and how those three primary reasons for buying more translate to post-pandemic purchasing behavior.

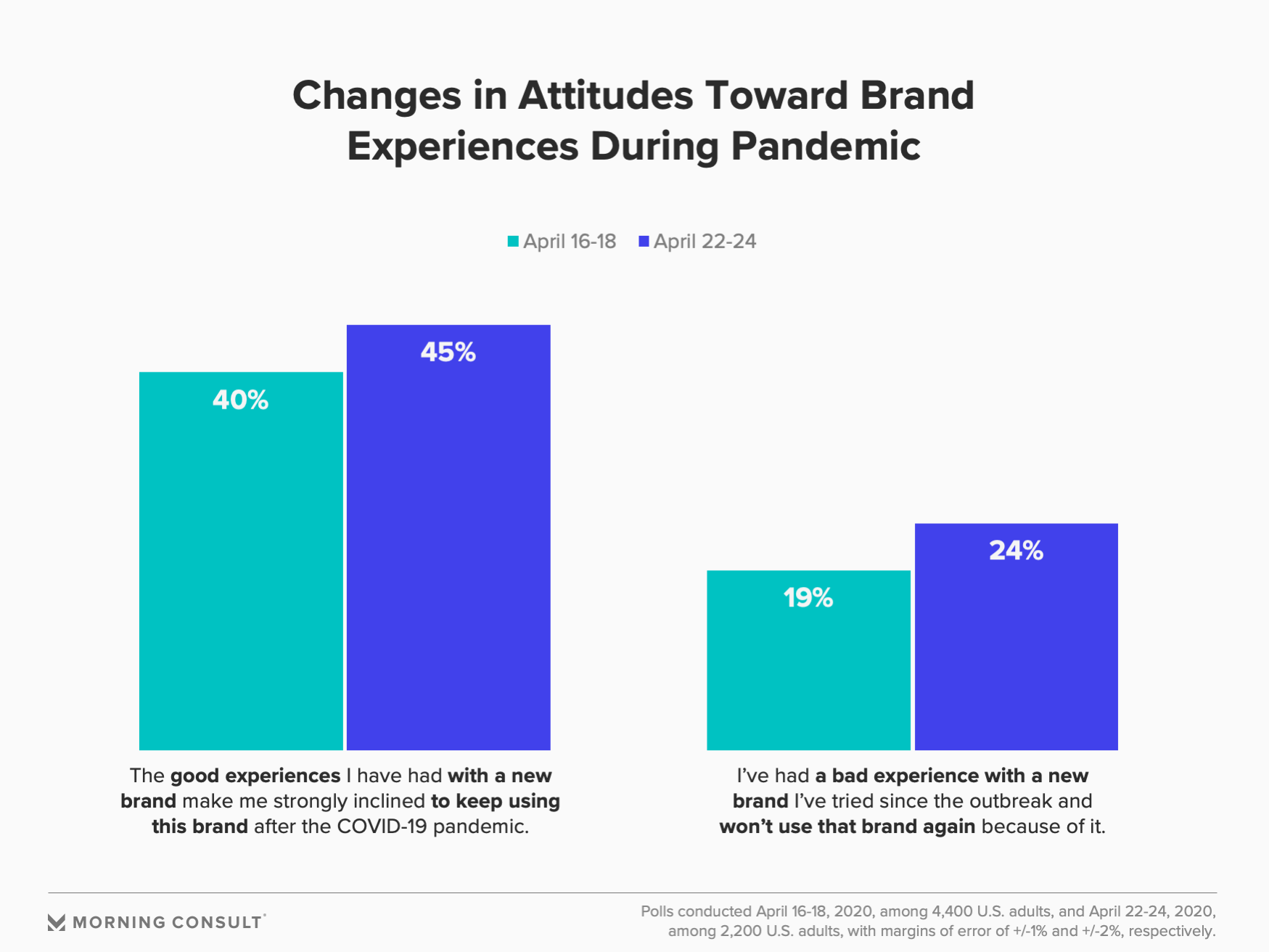

Consumers are paying close attention to the experiences companies are delivering to determine whether or not new brands and companies are worth sticking with post-pandemic. In just a week’s time, Morning Consult research finds that consumers are more strongly considering continued purchasing from brands that they’ve newly tried since the outbreak (33 percent, up 4 percentage points) -- and, importantly, from new brands delivering a good experience (45 percent, up 5 percentage points).

And, further evidence that customer experience matters: increasingly more consumers indicate that bad experiences with new brands or companies will cause them never to buy from them again.

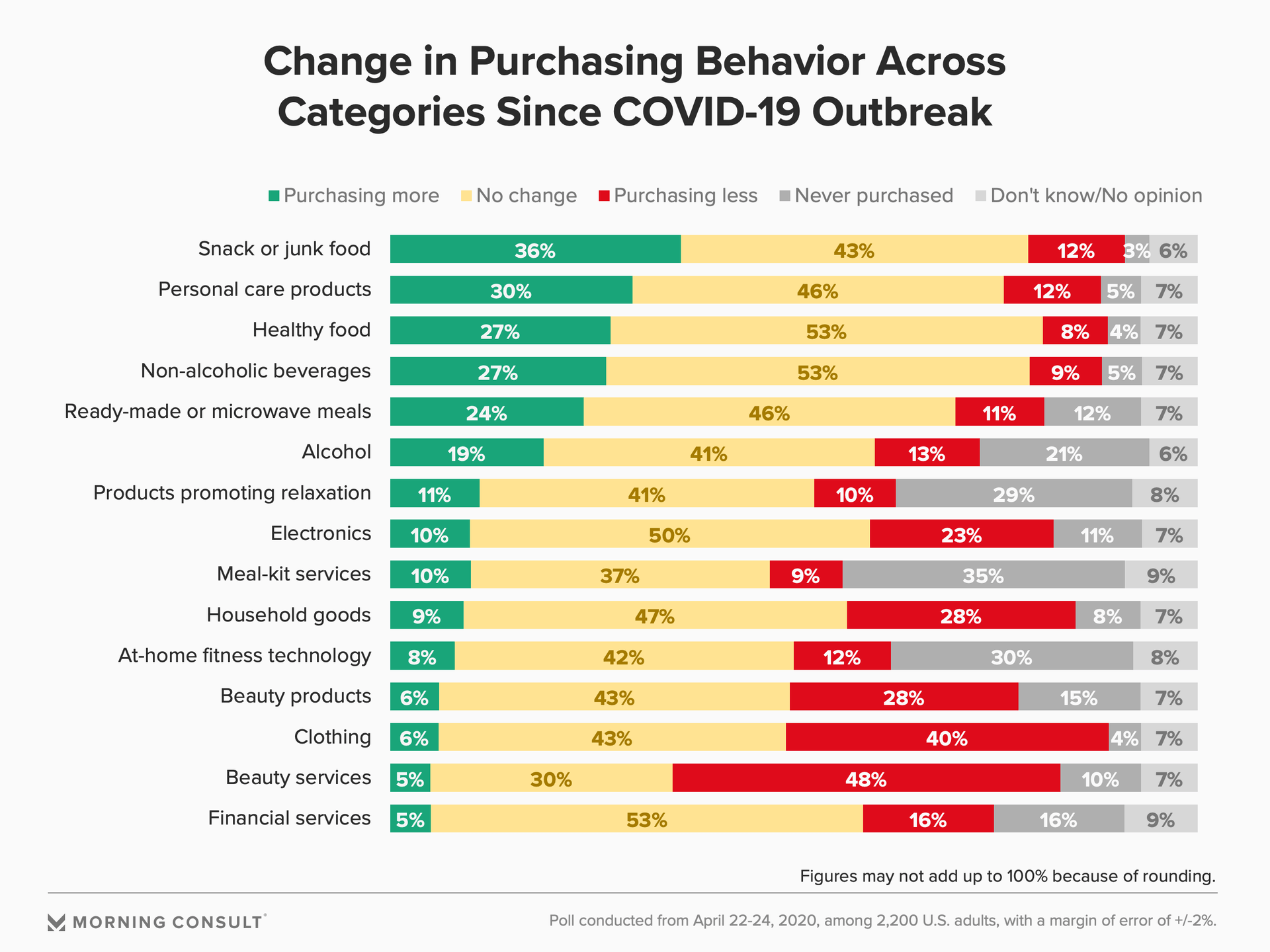

As consumers are jolted out of their usual purchasing patterns, brands active in categories seeing upticks in sales have a unique opportunity to both strengthen relationships with existing customers, and establish formative connections with new ones. Categories in which nearly a fifth or more of American consumers are purchasing more since the COVID-19 outbreak are snack and junk food, personal care products, healthy food, non-alcoholic beverages, ready-made meals and alcohol.

Personal care products and alcohol in particular are increasingly popular the longer stay-at-home policies are in place, seeing a rise of 9 percent and 7 percent among U.S. adults, respectively, since Morning Consult began tracking changing consumption levels in early April. Purchasing of snack and junk food and at-home fitness technology has also continued to rise though to a lesser extent; only time will tell whether or not this trend continues across these opposing categories.

Meanwhile, U.S. consumers continue to shift away from buying beauty services, clothing, beauty products, household goods and electronics, with at least 23 percent of the population and as much as 48 percent purchasing less of these categories since the outbreak began in the United States.

Still, amid these increases and decreases, it’s worth noting that purchase volume has remained consistent for at least 50 percent of the population in a few categories: healthy food, non-alcoholic beverages, financial services and electronics in particular.

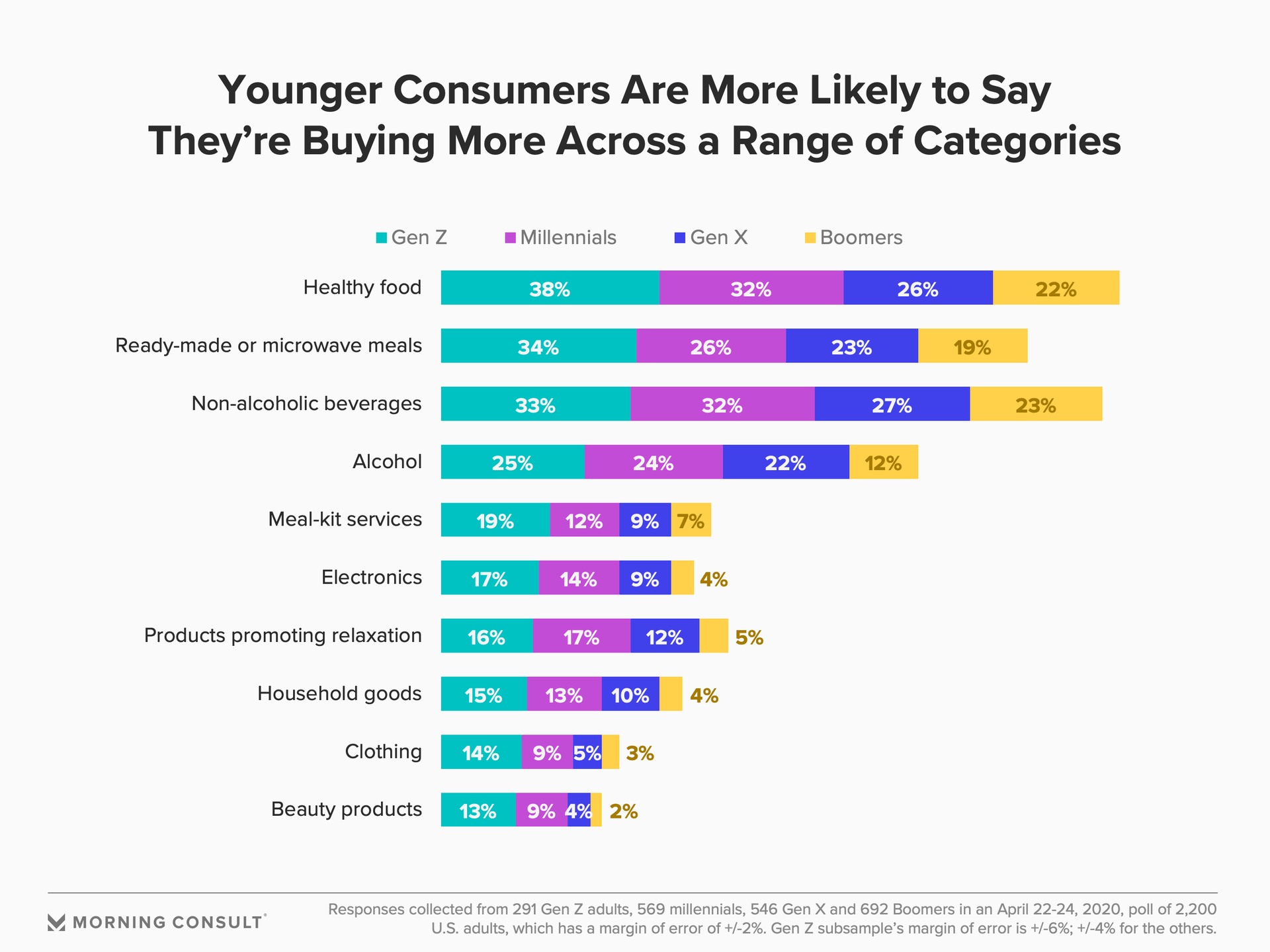

Across generations, the top categories experiencing greater consumer consumption during the pandemic are consistent, but the degree to which consumption has increased is not. Among certain categories -- including many of those with the highest increases in consumption since the outbreak -- Gen Z is handily out-consuming their elders: Their increases in consumption are anywhere from 70 to 80 percent greater than that of Boomers in a number of categories during this time.

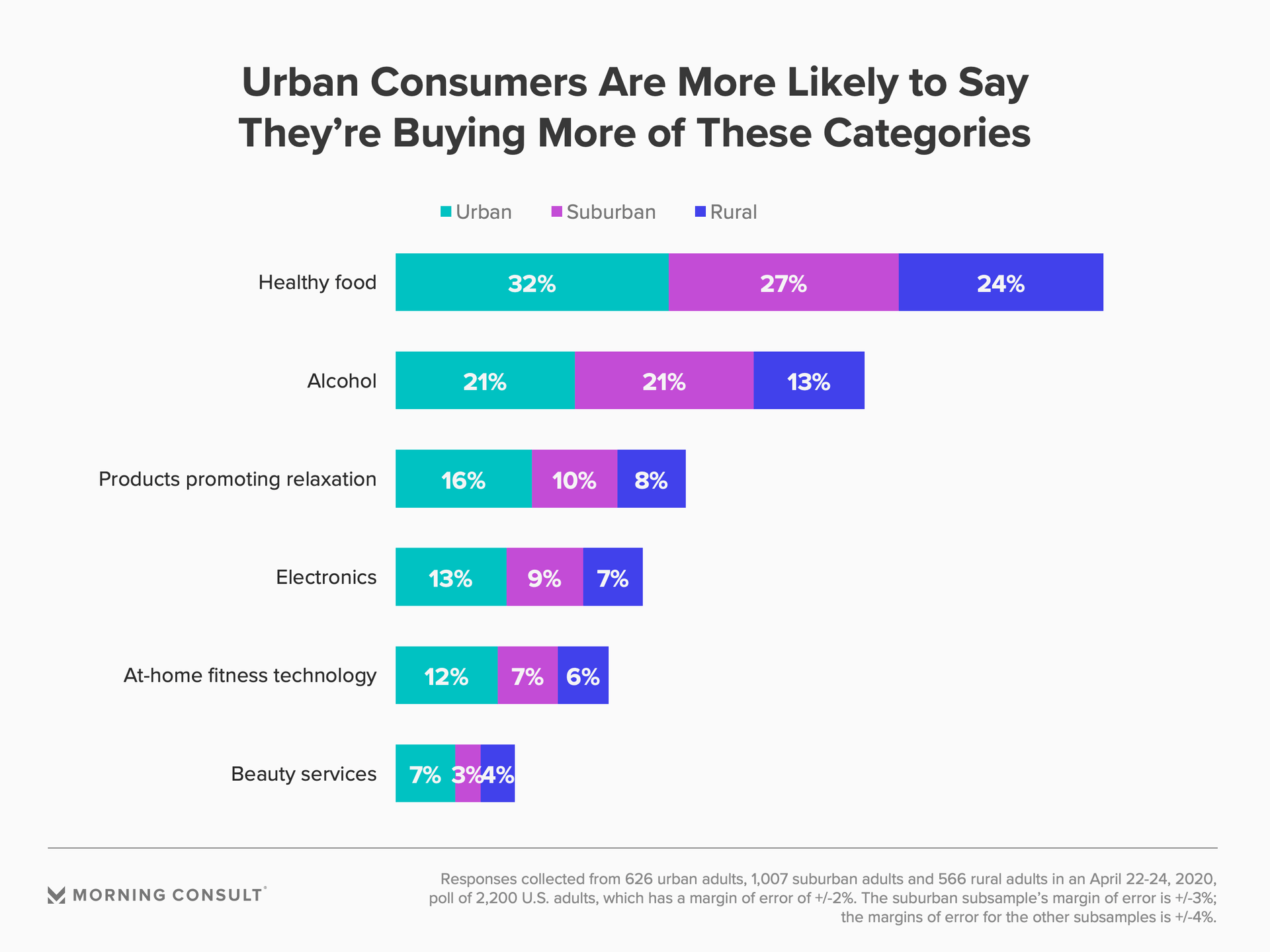

Urban populations are consuming notably more of most categories, including twice the increase in at-home fitness equipment, relaxation-related products and electronics relative to their suburban and rural peers. In combination with the alcohol urbanites are also purchasing notably more of during this time, it’s clear that the usual entertainment options and pastimes of city life have left this audience turning to certain categories to pass the time and provide comfort. Brands would be wise to find ways to fill these lifestyle gaps for urban consumers who are likely seeking the escape that more suburban life naturally affords.

With regard to incomes and education, higher levels are purchasing notably more alcohol and more healthy food, but the desire for snack and junk food appears to transcend class lines: Nearly a third of each income and education level is currently purchasing more of this category. Those with lower incomes and less education are likely on the front lines or facing layoffs, and as such are bearing the financial burden and emotional strain of this crisis to a greater degree than their peers; alcohol and health brands should be sure to underscore the relaxation and wellness benefits these product categories respectively offer to comfort and protect this vulnerable population during this trying time. In doing so, they can potentially forge even stronger relationships with this audience by delivering value in creative ways.

Finally, looking at genders, women are purchasing significantly more snack and junk food while men are buying more meal-kit services or electronics. Women are also cutting back notably on beauty services, clothing and beauty products much more significantly than men are, likely because they were the higher spenders on these categories in the first place, and because these are top categories impacted by stay-at-home measures and non-essential store closures. Still, companies in these three categories should act on this opportunity to maintain a close relationship with otherwise engaged customers as they turn their spending to less healthy comfort-food products. This will not only increase likelihood of repurchase post-pandemic, but also demonstrate the depth of a brand’s value by providing new, healthier, relationship-building ways to help women navigate this stressful situation.

People are increasing spending as much out of want as need

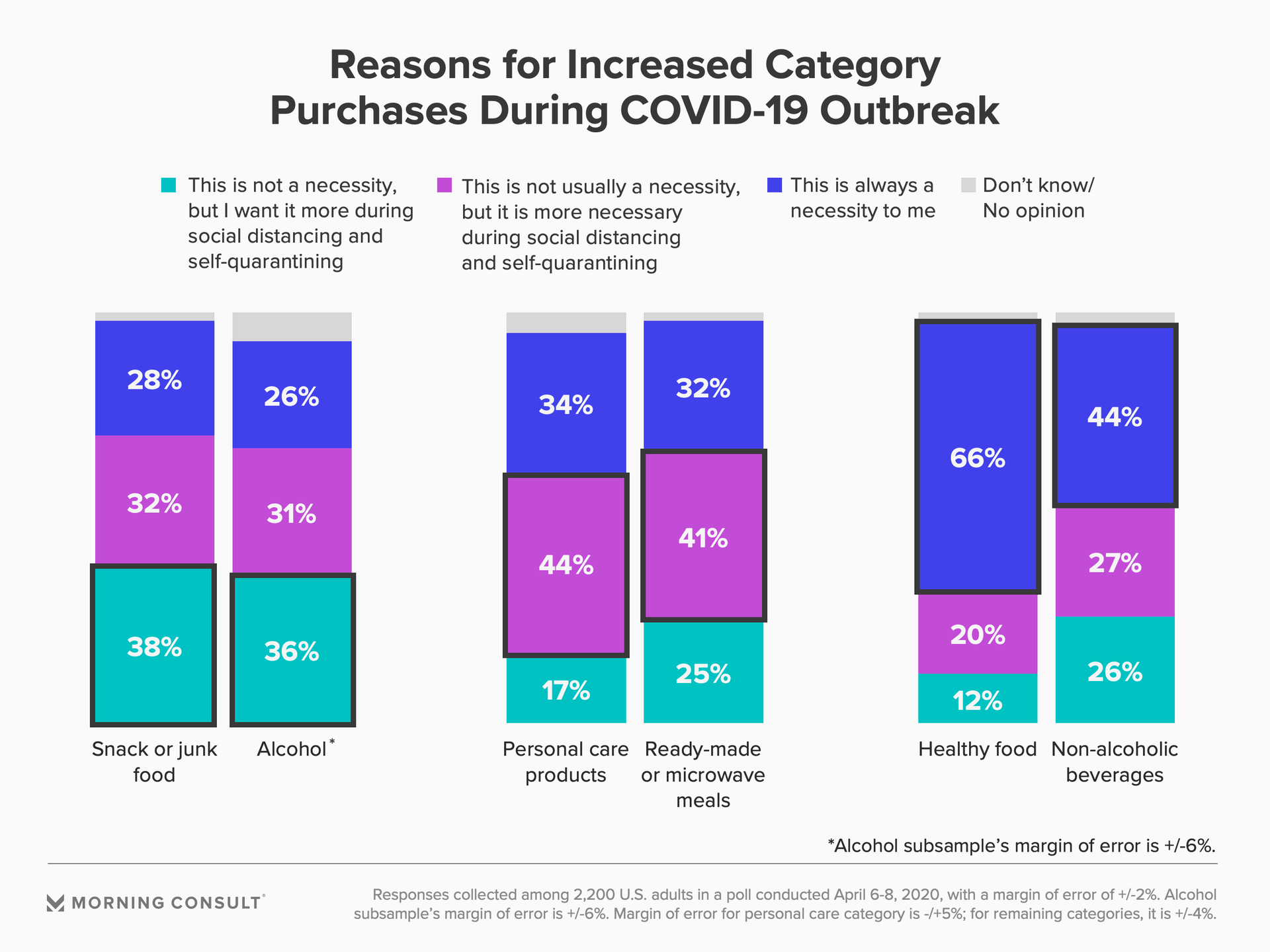

It’s been assumed that adults are buying only essential items they truly need at this time, not items they want -- but this isn’t the case when looking at each of the six categories where nearly a fifth or more of Americans have increased purchasing.

While non-alcoholic beverages and healthy food are being purchased more out of necessity, snack and junk food and alcohol aren’t a necessity to those buying more -- consumers are buying more of these since they simply desire these items more during social distancing and self-quarantining. Ready-made meals and personal care products aren’t considered necessities either, but they are being purchased more because, unsurprisingly, these items have become more necessary given the situation.

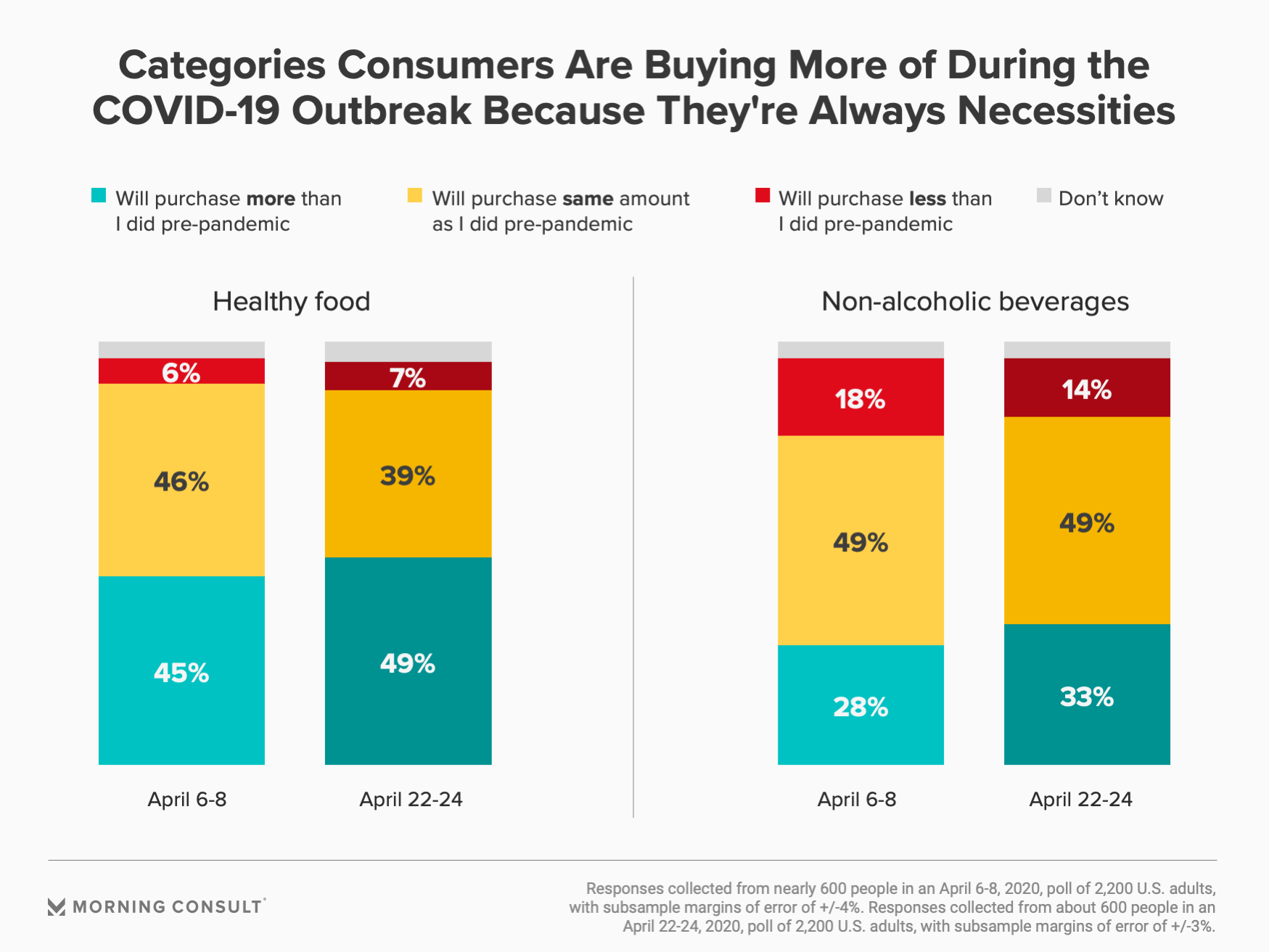

Across all categories being purchased more during the pandemic, at least some consumers expect to return to pre-pandemic purchasing levels. Healthy food, considered a necessity, is the category consumers are most likely to purchase more after the pandemic: 12 percent say they will purchase more, though it’s worth noting that the same amount, 12 percent, says they will return to pre-pandemic purchasing levels.

But beyond inertia returning people to their pre-pandemic consumption levels, top reasons driving increased purchase today predict how consumers will act tomorrow.

For healthy food and non-alcoholic beverages currently being purchased more because people always consider these items a necessity even in normal times, these consumers are quite unlikely to begin purchasing less; they largely expect to revert to pre-pandemic purchase levels. Still, nearly half of Americans (49 percent) currently buying more healthy food anticipate buying more of these items post-COVID, a trend health food brands will want to monitor closely as the crisis continues.

While these two categories are largely sure bets in that consumers expect to maintain if not increase connectivity post-pandemic, companies should nonetheless play defense: creating sticky habits, delivering on promises, assuring quality and value, and nurturing brand affinity will be critical for the post-crisis world in which consumers freedom of choice will return and every other category will have been strategically planning to draw consumers away from their old habits.

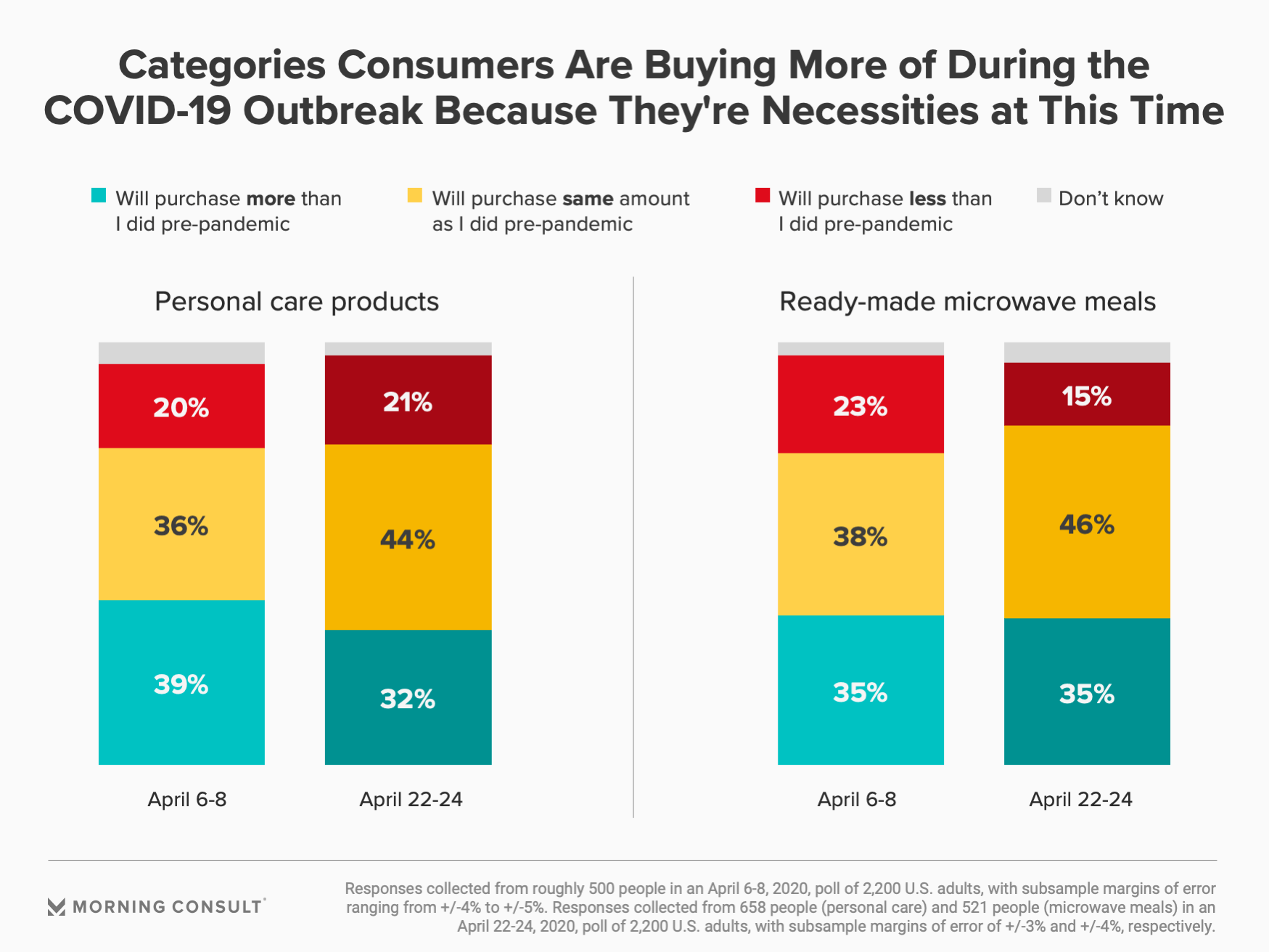

For personal care products and ready-made meals, which people are most likely to be buying more of now because these products have become more necessary at this time, those currently purchasing more are slightly more likely to purchase the same amount as they did pre-pandemic than to purchase more than they used to - but it’s worth noting that about a fifth of those currently buying more anticipates buying less of these items post-COVID, and nearly a third expects to buy more.

With no clear consensus on post-pandemic purchasing levels, brands in these two categories have a real opportunity to win over these “fence sitter” customers who are temporarily captive audiences. Emphasizing value, experience and quality to new and increased users in particular will help brands to strengthen relationships. Equally important for brands, however, is planning for a post-pandemic world in which consumers may associate their products with this troublesome and challenging period instead of the benefits the brand was able to deliver in a time of need.

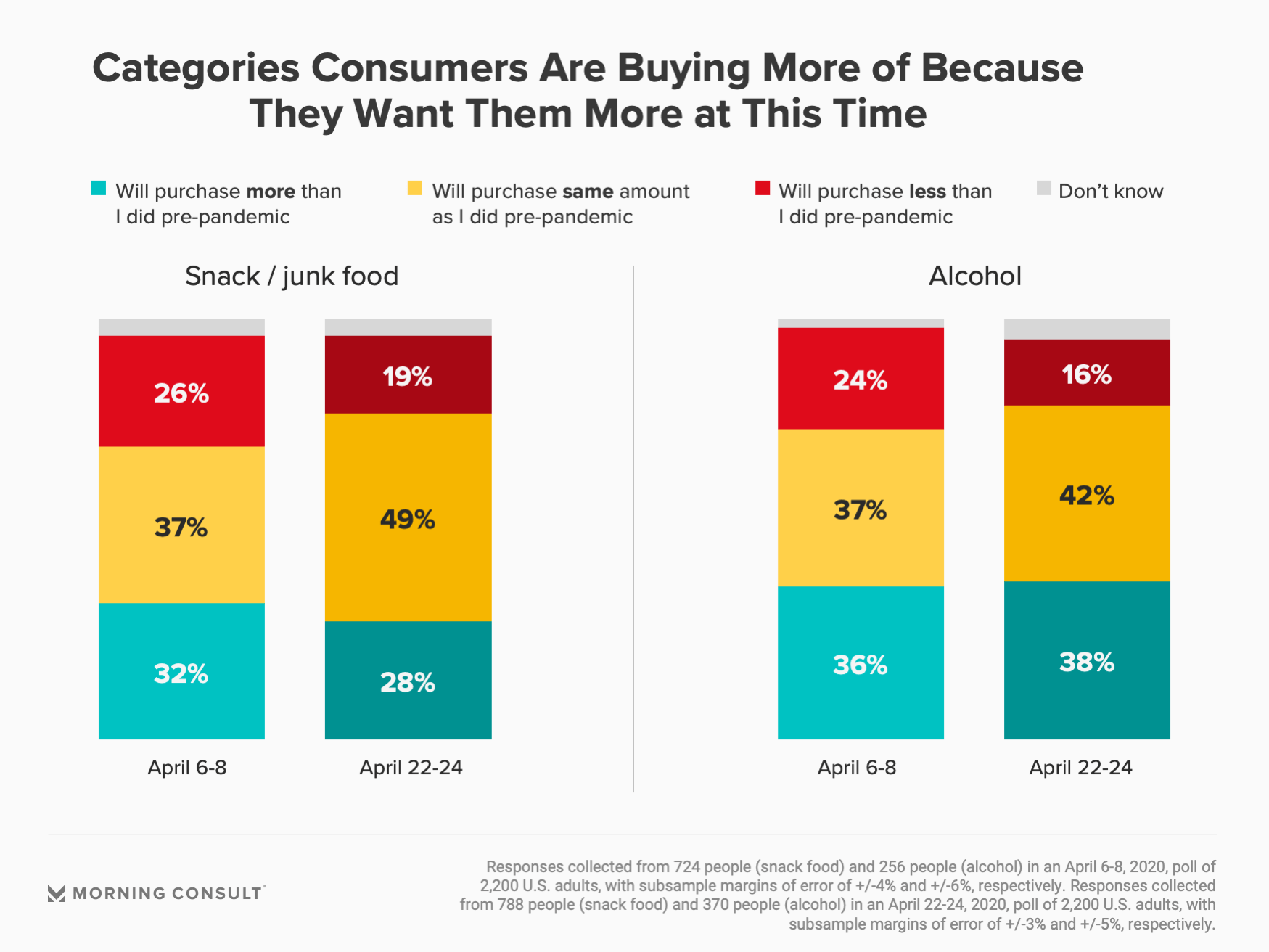

But consumers buying more snack and junk food and alcohol because they simply want them more at this time are mixed in their anticipated post-pandemic purchasing levels. While they are about as likely to purchase more alcohol as they are to revert to pre-pandemic consumption levels, they are quite likely to revert to pre-crisis levels of snack and junk food consumption.

The risk of reduced purchasing in each of these categories is clear, and with at least 24 percent of Americans expecting to cut back on spending in these categories just a few weeks ago, brands in these discretionary categories have strategic battles to fight: Remind consumers why they’ve always loved the brand, especially in pre-pandemic times, or remind them that the brand was there for them during trying times? Regardless, a company’s decision to focus on those sure to return to its products and category versus striving to forge sticky relationships with new users and those currently turning to its products for comfort will have important implications for promotions, messaging and positioning.

The implications are clear: While people will revert to purchasing at least as much, if not more, of what they always perceived as a necessity, the real opportunity exists for brands in traditionally non-necessity categories that are seeing increased usage at this time.

- In categories consumers are embracing more out of pandemic-induced need, consumers will almost certainly not purchase the same amount of these items as they did pre-pandemic -- but they are also not any more or less likely to purchase more or less of those items. With the right strategy, consumer insights and messaging, brands have the opportunity to sway these consumers toward increased post-pandemic purchasing, and away from stark drop-offs when normalcy returns.

- But among those purchasing more products in non-necessity categories out of desire, nearly a quarter of consumers planned to purchase less of these items, though this portion has marginally declined in recent weeks. Again by leveraging the right strategies, consumer insights and messaging, players in these categories will need to appeal to consumers to purchase at least as much as they were before, if not more, once life begins to return to normal. This will likely require unique positioning to avoid associating with the coronavirus; instead, players in these indulgence categories should endeavor to leverage any foundational relationship established during this situation to evolve the conversation and create new, more positive associations.

Brand experimentation represents an opportunity to woo ‘fence sitters’

Consumers are experimenting with new products in all categories seeing increased purchase volume during the pandemic, but this is notably more true in the ready-made meal and personal care product categories, where increased purchasing is driven predominantly by temporary need (i.e. “not usually a necessity but is more so during social distancing and self-quarantining”).

This further reinforces the significant opportunity within the “fence sitter” audience outlined above: If nearly half of all consumers buying more in now-essential categories are experimenting with new brands in those categories, and if they’re equally as likely to purchase more of these items as they are likely to purchase less of these items post-pandemic, brands in these categories need to more quickly and capitalize on the opportunity to build affinity among this newly gained and high-potential “fence sitting” audience.

The data also shows that men are more open to experimentation at this time: They are more likely than women to have tried a new brand in a number of categories, including healthy food, snack and junk food, ready-made meals, both alcoholic and non-alcoholic beverages and even personal care items. This suggests that brands in those categories will have to work harder to both acquire new female customers at this time and to retain males who may be quick to experiment with a new brand of product and then move on.

Conversely, this trend may have broader implications for customer loyalty. In a time when many consumers are quick to purchase new brands simply because their go-tos are unavailable, this may signal that women are more inclined to pass on products with which they are unfamiliar or don’t already have a trusting relationship. Brands in these categories would be wise to reward loyal female shoppers during this unique time in which availability can all too easily precede loyalty.

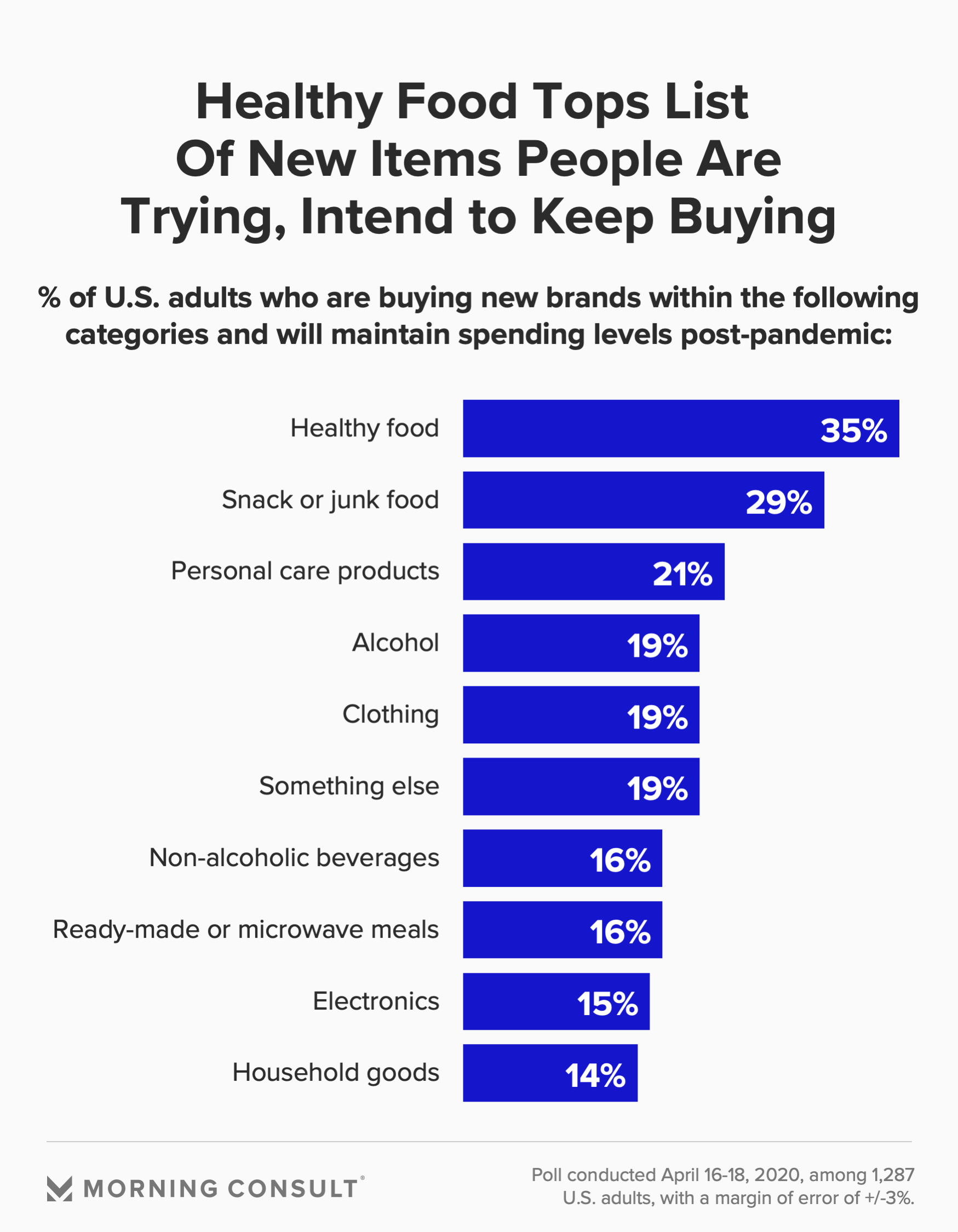

At least a few categories in which consumers have tried new products since the COVID-19 outbreak can be optimistic that some of those new customers won’t disappear. Thirty-five percent of Americans spending more on new healthy food items expect to continue buying new items they’ve tried in recent weeks and 29 percent said the same of snack foods, though it remains to be seen how habits adjust once a sense of normalcy returns, as consumers predict their absolute consumption levels of these near-opposite categories to look quite different as life transitions back to “normal.”

With 26 percent of the population planning to purchase less snack and junk food post-pandemic compared to the 45 percent expecting to buy more healthy food post-pandemic, healthy food brands must go on the defensive, entrenching customer relationships and highlighting value propositions to reinforce shoppers’ current desires to continue purchasing post-pandemic. Meanwhile, more indulgent snack brands should begin thinking about the new ways they’ll appeal to consumers when the strained reality of sheltering in place and social distancing begins to lessen.

Categories seeing less spending: Are consumers missing or kissing good-bye?

Categories such as beauty services, clothing, household goods and beauty products are being purchased less by at least a quarter of Americans, but across most categories currently being purchased less, consumers plan to return to pre-pandemic purchase levels, though some nuances exist:

- Consumers are nearly as likely to purchase electronics, snack or junk food, alcohol and ready-made meals less than they used to pre-pandemic as they are likely to purchase the same amount as they did prior.

- Though the majority of consumers currently buying fewer personal care items and relaxation-related products expect their purchasing of these items to return to pre-pandemic levels, a notable portion plans to purchase more of these items post-pandemic than they did before.

Still, brands should be aware that 44 percent of U.S. adults agree that there are brands or companies they are spending less on that they’ve realized they don't miss and can live without. This is especially true for Gen Z, more than half of which agree with this statement, and notably less true for Boomers, as just over a third of this generation agrees. But while younger generations seem quick to be trimming their short lists, they’re also most likely to be anxiously awaiting the return to certain favorite brands. This same trend holds with higher income and higher education levels, who are more likely than their peers to have brands they’ve realized they don’t miss but also brands they’re eagerly waiting to repurchase again.

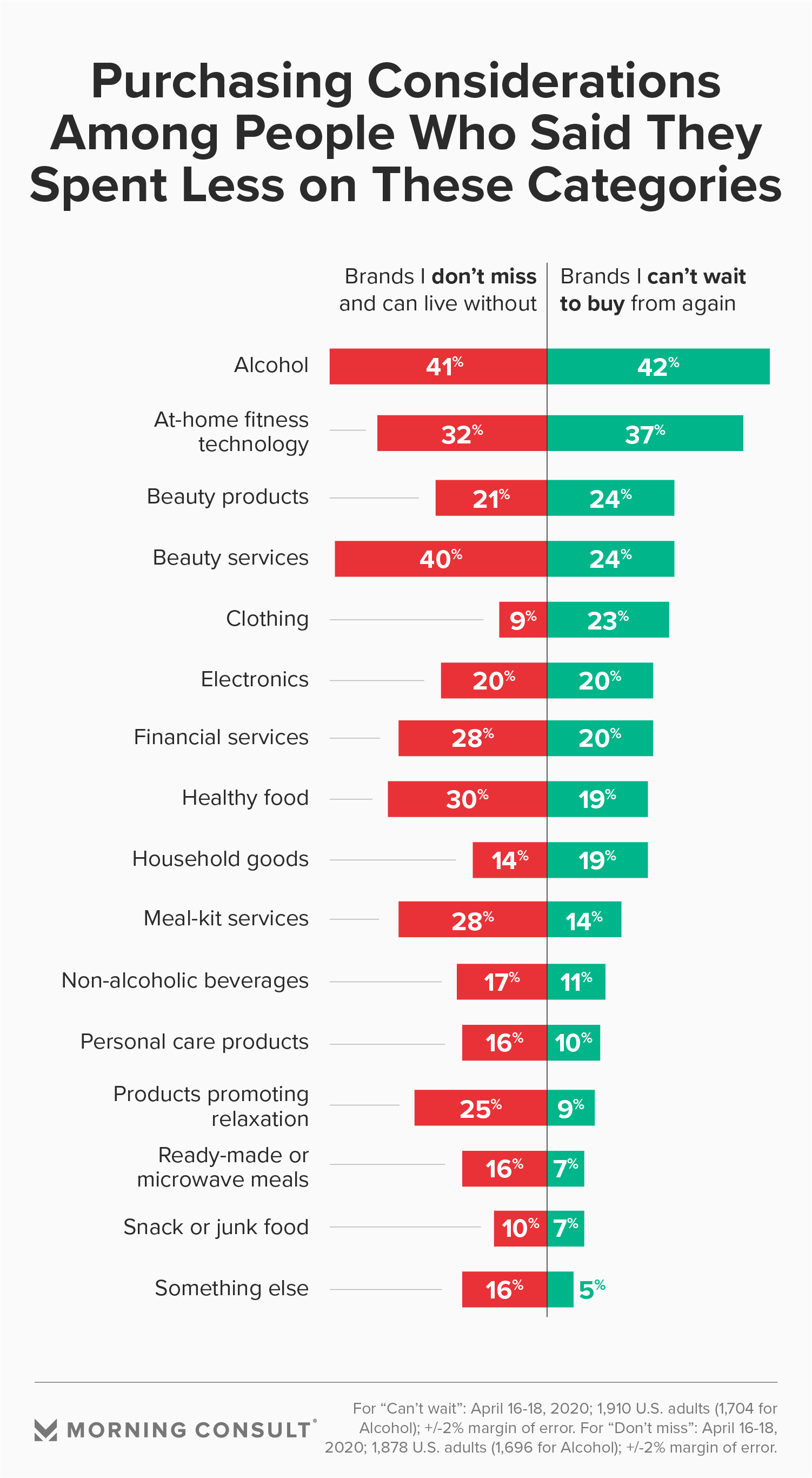

Digging deeper into which categories those most-missed and hardly missable brands fall into, it’s evident that -- separate from the categories which adults expect to spend more on -- certain brands will need to work especially hard to reinvigorate demand post-pandemic. In the short term for brands, maintaining and potentially building on relationships with existing customers should be the top priority, whether by continuing to communicate, engaging in new ways or somehow pivoting a product or offer to create new appeal during a time when corporate innovation and creative problem-solving are being rewarded by consumers.

It’s also key for companies to consider that people who’ve realized the forgettability or interchangeability of their product or category may spread the word to any peers not yet in the “can’t live without” group, and unleash a challenging (and costly) ripple effect.

Victoria Sakal previously worked at Morning Consult as a brands analyst.