The New Apple Savings Account Aligns With What Consumers Want

Key Takeaways

Apple’s new savings account is enticing for current Apple Card owners — the majority (69%) said they would be likely to consider opening an account. There’s also interest in the account among consumers who do not own the card, particularly Apple’s core audience of Gen Zers and millennial adults.

Digital wallets are generally trusted by consumers, but lingering concerns about financial safety and fraud could impede further adoption for some.

The continued blurring of lines between tech and finance has the potential to invite additional regulatory scrutiny at a time when tech is already under a microscope.

For the latest global tech news and analysis delivered to your inbox every morning, sign up for our daily tech news brief.

Apple last week announced that it would offer Apple Card holders the ability to hold funds in a new high-yield savings account. Its 4.15% savings rate — much higher than what’s offered by traditional banks and other financial institutions — as well as its absence of fees or account balance minimums, are likely to be very enticing to users of Apple’s credit card. The offering also stands to attract consumers from outside the Apple ecosystem.

A recent Morning Consult survey shows that the features of Apple’s new offer line up well with what consumers are looking for in a savings account, and many in the company’s core audience of affluent and young people are primed to consider an Apple version of the product.

Apple’s core audience of Gen Zers and millennials are interested in its new savings account

In the days following Apple’s announcement, the majority of Apple Card owners (69%) said they would consider opening a new savings account with Apple in the next six months. A near-equal share (71%) also reported hearing about Apple’s new savings account, compared to just 21% of non-Apple Card owners. The high level of awareness and consideration among current Apple Card owners can be attributed to the brand loyalty inspired by the company’s deep ecosystem of products and services.

For Apple, and for this offer to succeed, the better question is whether the company can convert Apple Card nonowners (85% of U.S. adults). On its face, the large gap in consideration for opening a savings account with Apple between Apple Card owners and nonowners may be an early sign that Apple has a lot of work to do in promoting the new product. However, Apple does not need to convert everyone — just those already primed to consider its offerings.

Apple Card owners tend to be male, young and high earners

Given that owning Apple’s credit card is a prerequisite for opening the company’s savings account, it’s important to understand the demographic details of an Apple Card owner. An owner is more likely than a nonowner to be male, Gen Z or millennial, highly educated, high earning, a parent and Black or Hispanic.

This is also consistent with frequent users of other Apple products, such as Airpods, MacBooks and iPhones, according to Morning Consult Brand Intelligence data, though Apple Card owners are much more likely to come from high-income households.

Regarding those who are not current Apple Card users, our data shows encouraging signs that millennials and Gen Z adults in particular are more willing than the average U.S. adult to apply for the card with the express purpose of accessing Apple’s savings account. High-income nonowners are also more likely than their lower-earning peers to consider applying for an Apple Card to open a savings account.

Apple has over the years built a great deal of credibility and loyalty among young and affluent people, which appears to be paying off for its financial services offerings.

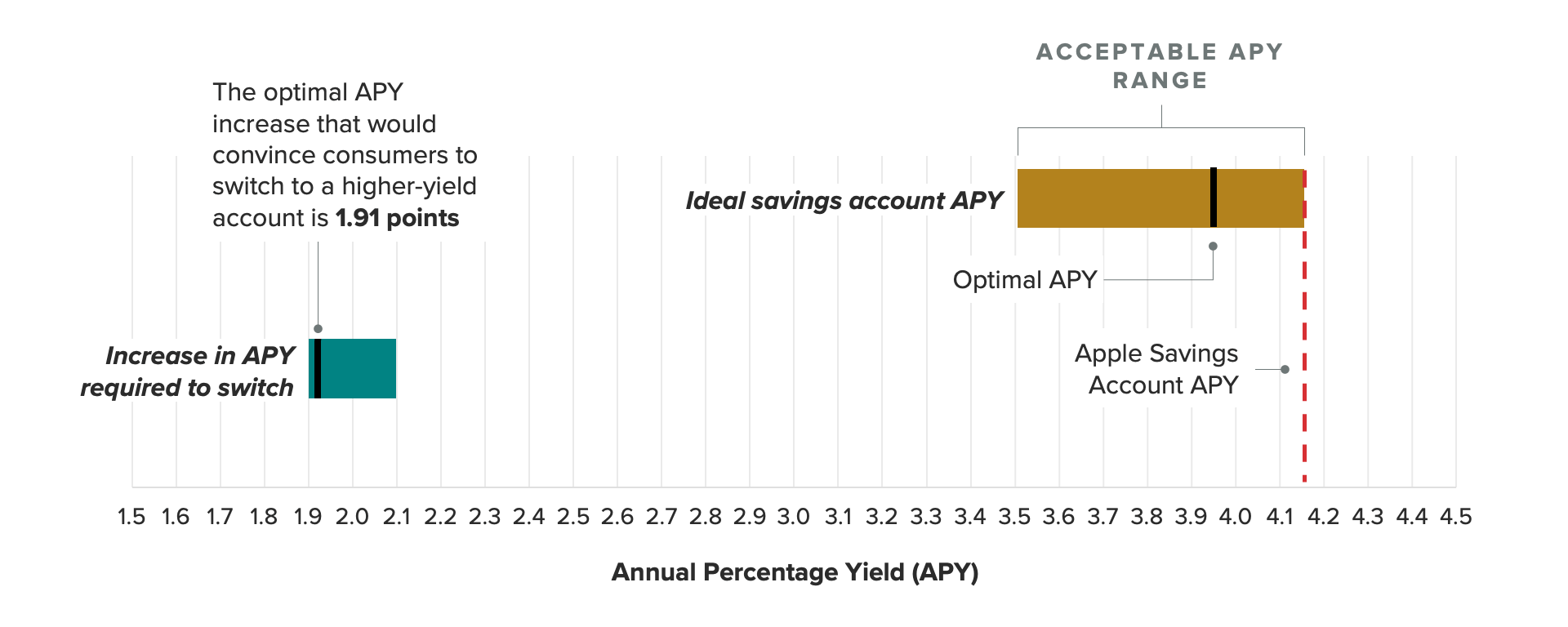

Apple’s savings account rate of 4.15% lines up with the 3.94% rate consumers say they want

A survey conducted by Morning Consult last month before the latest Fed rate increase indicates that peoples’ ideal annual percentage yield for savings accounts hovers around 3.94%, and it would take an increase of 1.94 points to convince people to consider a savings account provider other than their own. With the average savings account yielding around 0.39%, Apple’s offer is very enticing at face value and its APY is above that which consumers consider optimal.

Another factor that works to Apple’s advantage is recent turbulence in the banking sector, which coincides with an increase in the share of high-income adults who are willing to start a relationship with a new banking provider. Apple Card holders (37%) are much more likely than nonholders (13%) to have a household income of $100,000 or more, making that group more receptive to Apple’s financial services products.

Compared with December 2022, adults who report $100,000 or more a year in household income said they were 10 percentage points more likely to start a relationship with a new bank, and 7 points more likely to start a relationship with a new digital bank.

Digital wallets have trust, but Apple still needs to address concerns about financial data security to drive adoption

At the brand level, roughly the same share of consumers said they trust Apple (58%) as the share who said they trust Chase Bank (59%) regarding their financial data’s security and privacy, a good sign for the tech company as it wades deeper into the financial services pool.

More generally, people are more likely than not to trust digital wallets and tech companies with their financial data’s security and privacy. While most adults say they trust tech companies with their financial data (54%), trust is higher with digital wallets (60%) and even higher with online banks (72%), indicating that how tech companies position their financial services operations makes a difference in their perceptions.

While digital wallets are generally trusted by consumers (they made up some of the most trusted financial services brands last year), that’s not to say that consumers don’t have lingering concerns about the services. At the top of their list of concerns is theft if a device is misplaced or stolen — an understandable fear for those of us who have left a phone behind in an Uber — though Gen Z adults are the least likely to be phased by this possibility and are most likely to be concerned about fraudulent purchases.

While digital wallets have made their mark and have even become essential services for many, lingering concerns around data security and the integrity of peoples’ finances are factors that should be adequately addressed — especially among Gen Z and millennials — to drive further digital wallet adoption.

Apple’s entrenchment in the financial world could invite more regulatory scrutiny

But there is one risk Apple is running with its play: Its new savings account is yet another indicator that tech brands and financial services brands have become more and more inextricable, and with the government’s eyes on tech this year, Apple’s foray into another sector could drive further scrutiny.

This year is already a difficult one for the tech industry from a regulatory perspective. Both Democrats and Republicans (65% and 61% respectively) said they agree with the legal default that tech companies that offer savings accounts should be regulated as financial services companies, indicating that this move could just be one more regulatory hurdle for Apple as it continues to fight antitrust suits.

Jordan Marlatt previously worked at Morning Consult as a lead tech analyst.