Key Takeaways

Coming out of the depths of the pandemic, tight supply and strong demand have coalesced to drive up prices for homes and autos for the U.S. consumer.

More recently, high prices and rising interest rates have diminished the appetite for these major purchases. According to the latest data from Morning Consult Economic Intelligence, these factors are now beginning to weigh more heavily on consumers.

While weakening purchasing intentions portend less spending, supply constraints will also continue to influence the trajectory of U.S. home and vehicle prices.

Following the initial shock of the pandemic, demand for housing and autos rebounded strongly in the United States. Related lifestyle changes (e.g., spending more time at home, a sharpened focus on upgrading living space and a greater preference for private transportation) contributed to greater demand for new homes and vehicles. At the same time, reduced spending on services during lockdowns, boosted disposable incomes from government stimulus payments and low interest rates fueled consumers’ ability to afford these major purchases.

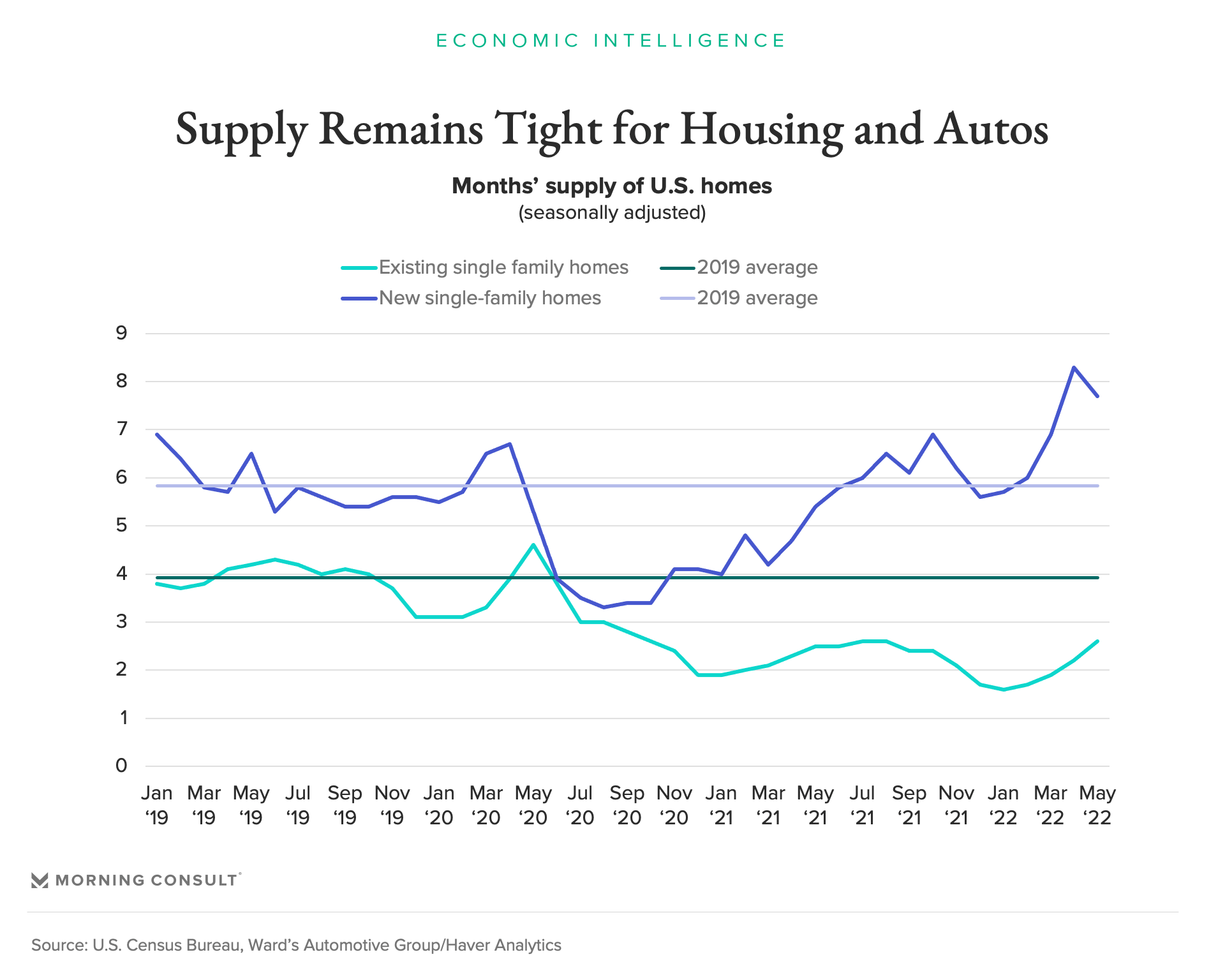

As demand picked up in the wake of COVID-induced lockdowns, both the housing and vehicle purchase markets grappled with supply constraints. For housing, a depleted inventory of homes available for sale — driven by years of relatively modest additions to the housing stock — was compounded by pandemic-driven construction delays arising from shortages of materials and labor. Similarly, auto production during this period was held back by a global semiconductor shortage that continues to limit production schedules.

Unsurprisingly, the combination of robust demand and tight supply yielded rapid price growth in these markets, with increases in housing and vehicle prices far exceeding overall inflation during this period. Purchases of homes and vehicles began to show signs of easing earlier this year as affordability concerns mounted due to rising inflation, which began to eat into the disposable income gains over the past two years. Going forward, Morning Consult surveys suggest that growth in spending on homes and autos could be poised to weaken further.

Consumers are increasingly backing away from major purchases

Morning Consult’s Supply Chain Indexes of Consumer Inflation Pressures can help us to better understand how purchasing decisions for homes and autos are being affected by current demand and supply conditions in these markets. The five indexes measure unavailability, price sensitivity, substitutability, purchasing difficulty and delivery delays from the perspective of consumers. As shown below, forgone purchases in May due to sticker shock (Price Sensitivity Index) and trading down to cheaper substitutes (Substitutability Index) were more common for large durable goods like new and used vehicles and housing than for nondurables like groceries and gas and services other than housing, as were supply constraints (Unavailability and Delivery Delays indexes).

More information on how to interpret the five indexes can be found here.

These results echo the broader theme that both housing and auto purchases are responding to intensifying pressures on affordability. As further evidence of this fact, Morning Consult data shows that the share of prospective home and apartment shoppers who executed these purchases fell from 43% in February to 36% in May of this year. Similarly, the share of consumers who said their household purchased a new or used vehicle in the past 12 months was down 3 percentage points for both categories year over year in May 2022. These figures align with a 13% decline in light vehicle sales from April to May 2022, according to the Bureau of Economic Analysis, and a 3% drop in existing home sales over the same time period, according to the National Association of Realtors.

Increasingly higher prices and shrinking inflation-adjusted disposable incomes make major purchases less affordable for the U.S. consumer. Moreover, rapidly rising interest rates are also beginning to weigh on affordability, with more increases on the horizon as the Federal Reserve looks to cool broader aggregate demand and temper inflationary pressures. All of these concerns are being reflected in negative perceptions of current auto-purchasing and homebuying conditions, which can be seen in Morning Consult’s high-frequency measures of consumer sentiment as well as the most recent University of Michigan Survey of Consumers.

Morning Consult’s latest Household Finances and Consumer Spending report suggests that U.S. consumers are increasingly backing away from major purchases in this environment, with purchases of large durable goods leading the way. As longer-lasting products, durables are often easier to defer than items like food, which is consumed immediately, and they have resale value, enabling expectations of future prices to directly influence current purchasing decisions. Durable goods spending is, therefore, often the first category to show signs of weakness when the U.S. economy slows and, as such, can be used as a leading indicator for overall consumer spending.

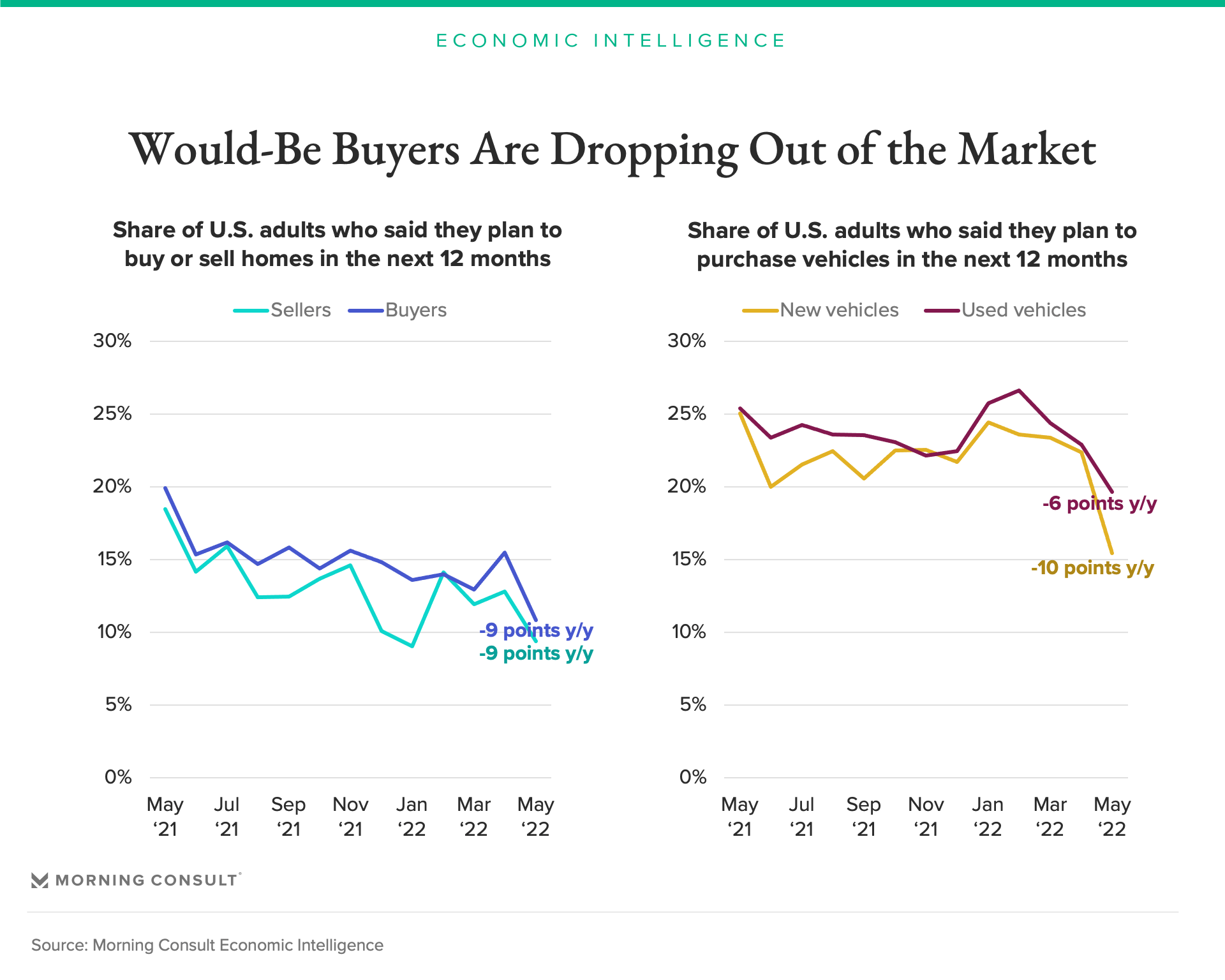

Forward-looking data from the same Morning Consult report suggests that these trends are likely to continue: In May, the share of adults who plan to buy autos over the next year declined sharply, posting annual declines of 9.6 and 5.7 points, respectively, for new and used vehicles. Furthermore, the share of adults planning to buy homes reached its lowest level since tracking began in January 2021, with the share of adults who are planning to sell over the next 12 months dropping by 9 points, from 18% in May 2021 to 9% in the same month in 2022.

What does this mean for prices?

Despite weaker demand in recent months, home and vehicle prices have remained elevated and continue to rise, largely as a result of ongoing supply constraints. The degree to which home and auto prices respond to weaker demand going forward may ultimately be tempered by how quickly supplies can be replenished. Lower demand will help, but supply matters as well.

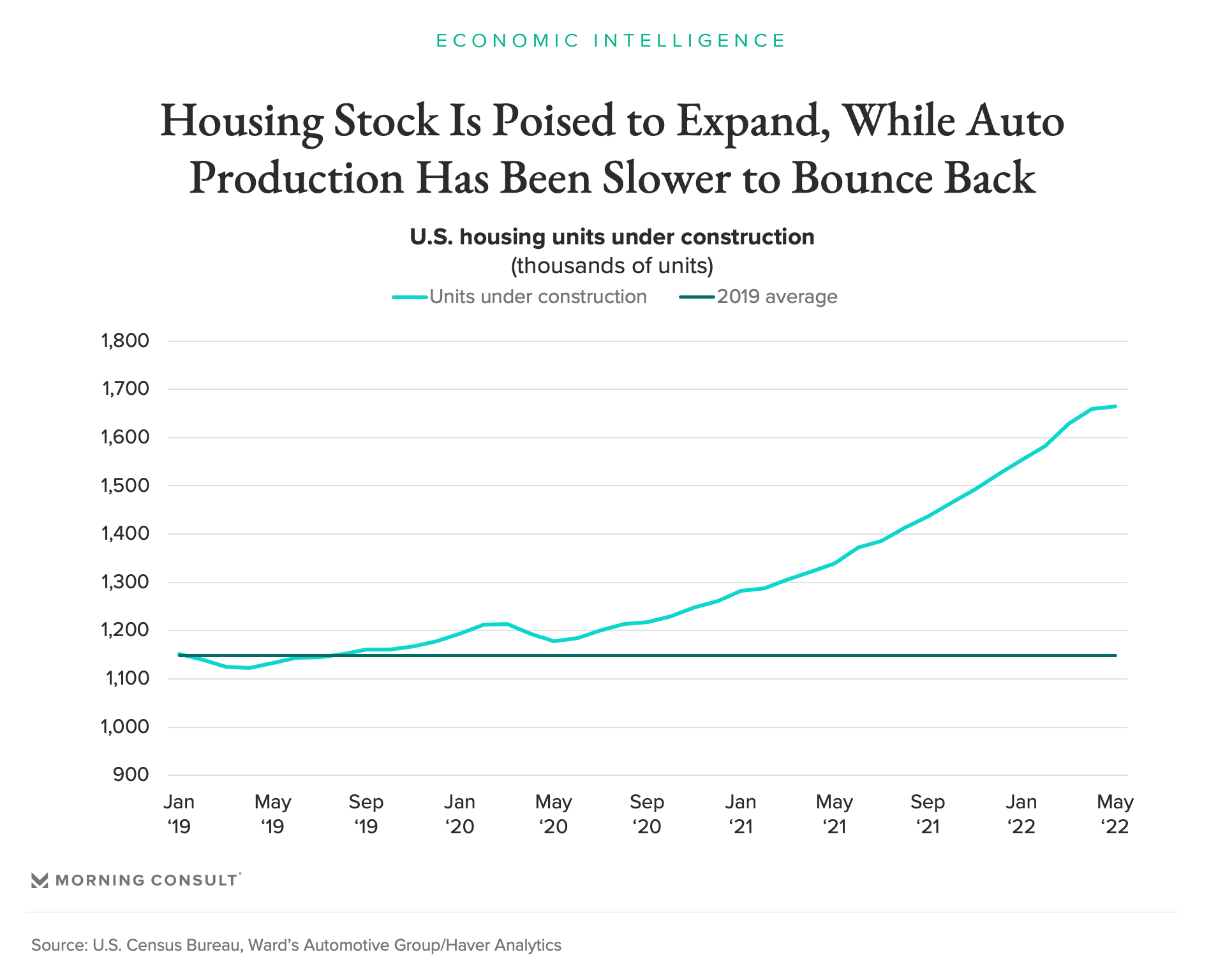

Increased supply may help loosen conditions for the housing market sooner than is likely to be the case for the auto sector, where production remains constrained and industry forecasts point to only modest growth in 2022. A robust pipeline of new home construction is poised to eventually deliver an influx of new home supply. As of May, the U.S. Census Bureau reported that nearly 1.7 million homes were under construction — the highest level on record and representing a little more than 1% of the existing stock of housing. As those units are completed, increased supply and softer demand should dampen the rise in home prices.

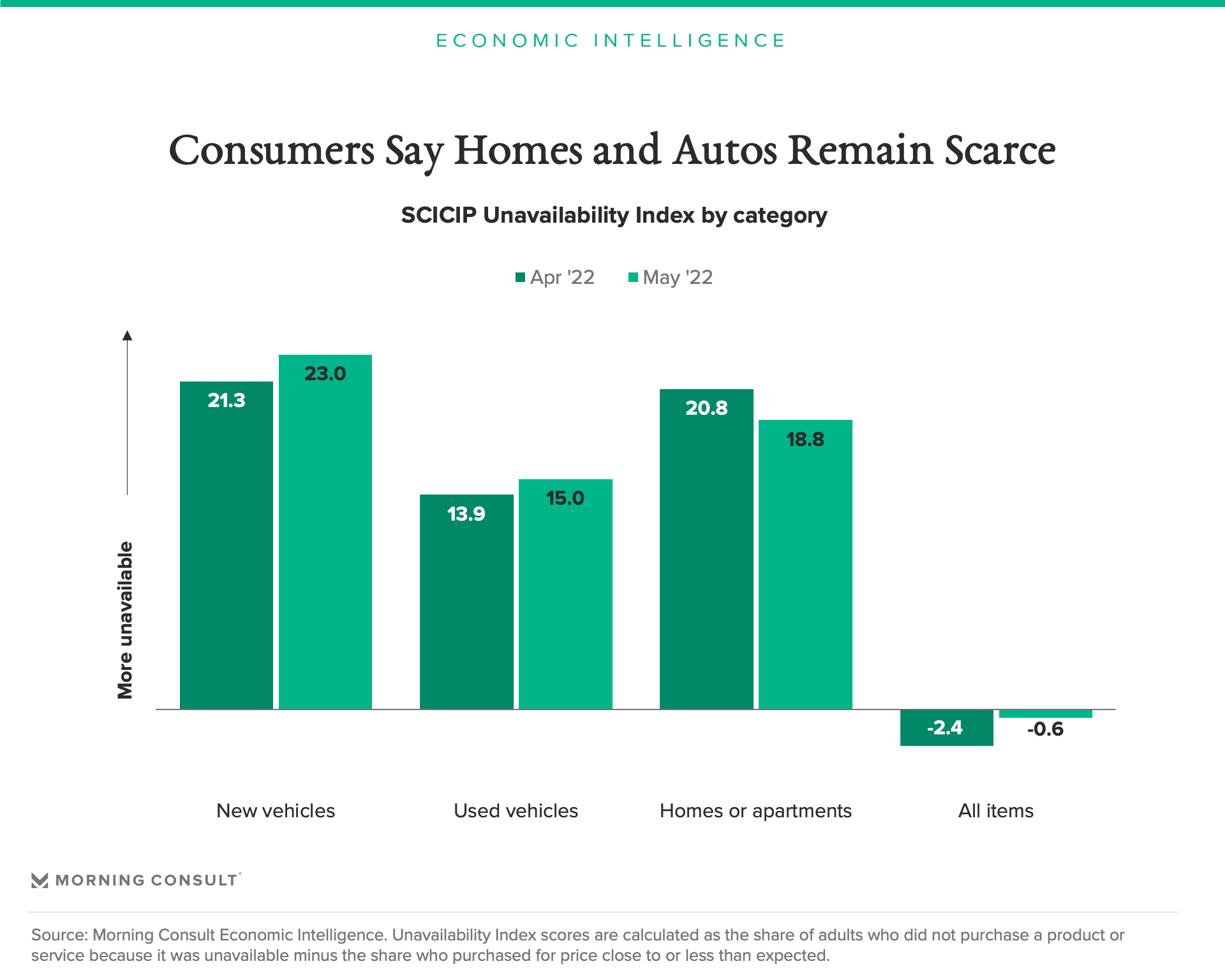

Morning Consult’s latest Supply Chains & Inflation report suggests that we may be seeing some early signs of easing housing supply constraints, with Unavailability Index scores for homes and apartments declining from April to May of this year. However, the same cannot be said for new and used vehicles: Consumers reported in May that availability continued to decline. Without significant improvements in supply — or at very least a leveling off in the supply chain disruptions in the auto industry — upward pressure from supply constraints on vehicle prices is likely to continue.

The outlook for homes and autos

Looking ahead, much of the potential demand loss from higher interest rates in the housing and auto markets has yet to be realized. While Morning Consult’s surveys show that consumers have already begun to push back against price increases for homes and cars, it is future buying intentions over the next 12 months that have weakened the most. As these softer purchasing intentions play out in the coming months, price pressures are likely to recede to some degree — especially for the housing market, which is also poised to absorb a large influx of new supply.

Kayla Bruun is the lead economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency economic data. Prior to joining Morning Consult, Kayla was a key member of the corporate strategy team at telecommunications company SES, where she produced market intelligence and industry analysis of mobility markets.

Kayla also served as an economist at IHS Markit, where she covered global services industries, provided price forecasts, produced written analyses and served as a subject-matter expert on client-facing consulting projects. Kayla earned a bachelor’s degree in economics from Emory University and an MBA with a certificate in nonmarket strategy from Georgetown University’s McDonough School of Business. For speaking opportunities and booking requests, please email [email protected]

Scott Brave previously worked at Morning Consult in economic analysis.