Key Takeaways

Morning Consult’s latest data suggests that core CPI inflation is likely to increase in November after falling dramatically in October — but it is unlikely to increase as much as it did in September, implying a further decline in the pace of annual inflation.

In October, as inflation retreated to its slowest annual pace since January, all five of Morning Consult’s SCICIP declined, reflecting broadly easing supply constraints and improving purchasing power.

Previous large and unanticipated declines in inflation this year were immediately followed by a rebound the following month. However, the underlying details of the SCICIP suggest that some of the recent inflation relief may persist into November.

All five of Morning Consult’s Supply Chain Indexes of Consumer Inflation Pressures showed signs of easing in October — the first time this has happened since tracking began in March. Their movements also coincided with a substantial decline in the rate of Consumer Price Index inflation, as consumers experienced a welcome reprieve from the sting of rapid price growth, particularly for “core” (excluding food and energy) prices. Below, we take a closer look at the results from Morning Consult’s latest Supply Chains & Inflation survey with an eye toward understanding whether we can expect this development to continue in November.

Consumers experienced some welcome inflation relief in October

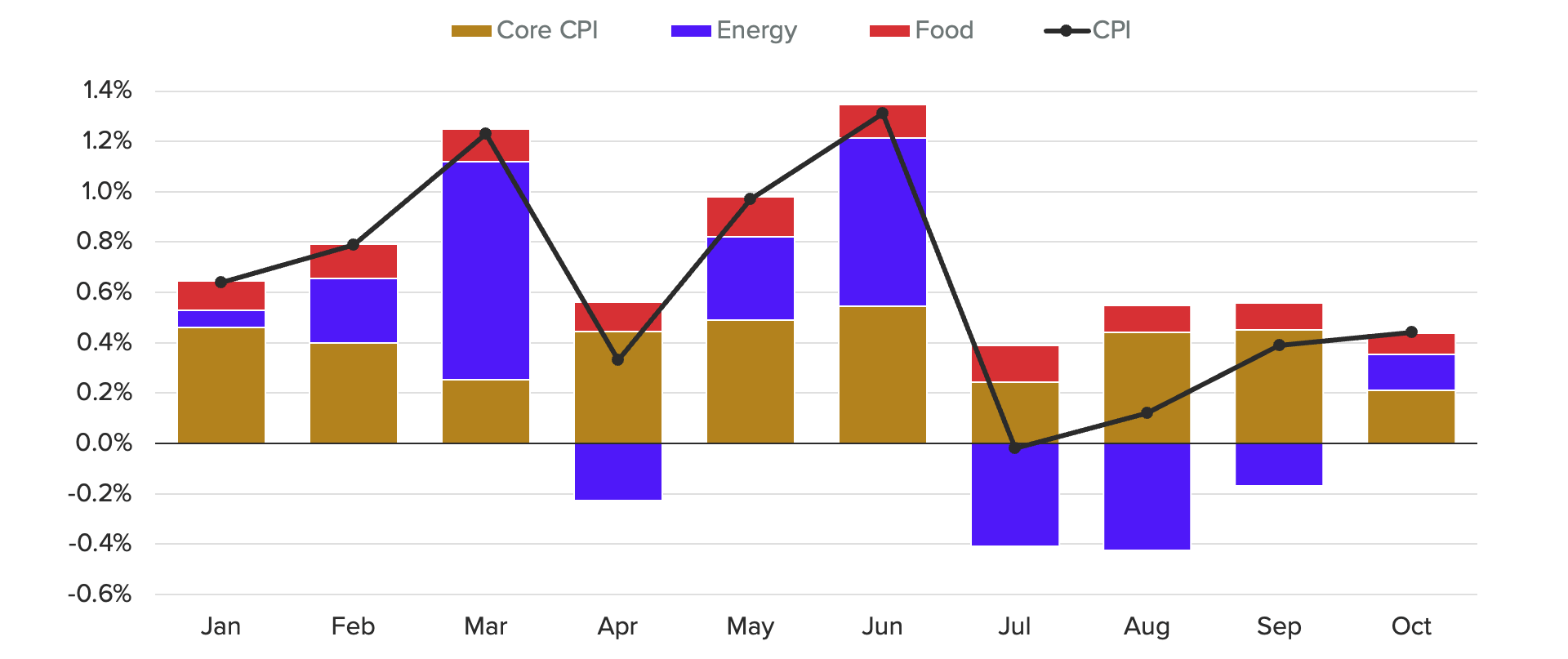

Before we jump in, allow us to recap some recent developments in the CPI: Month-to-month increases in CPI were already quite large by historical standards as we entered 2022, but they intensified in March following the onset of the Russia-Ukraine war. Both food and energy prices were particularly affected by the developments in the spring, driving year-over-year CPI inflation to a 40-year high by mid-2022. CPI inflation began to slow as gasoline prices came down over the summer, but both food and core inflation remained stubbornly high.

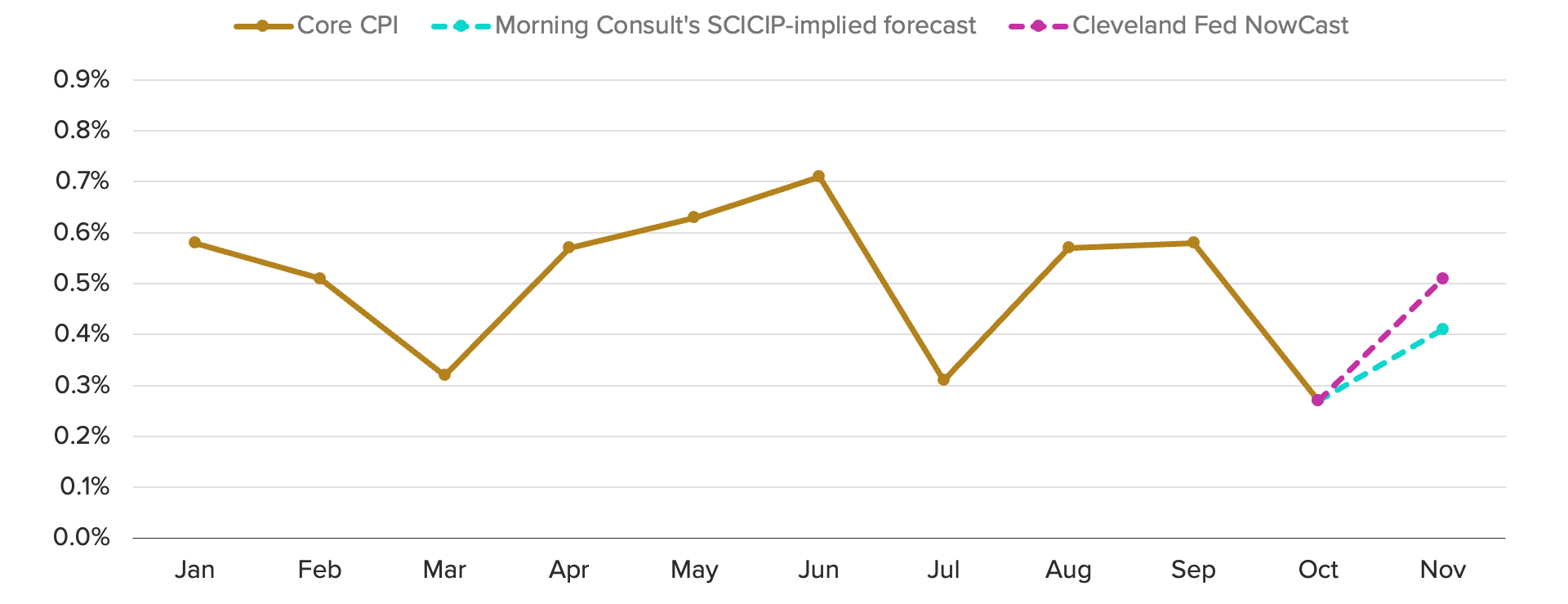

The figure below shows how these developments have affected CPI inflation throughout 2022. In August and September, the improvement in CPI inflation from falling energy prices was mostly offset by increases in core CPI inflation, driven in large part by price growth for services such as housing, transportation and medical care. Services make up a much larger share of the consumption bundle than goods, and inflation for these categories tends to be more persistent than for commodities, giving them an outsize influence on core CPI inflation.

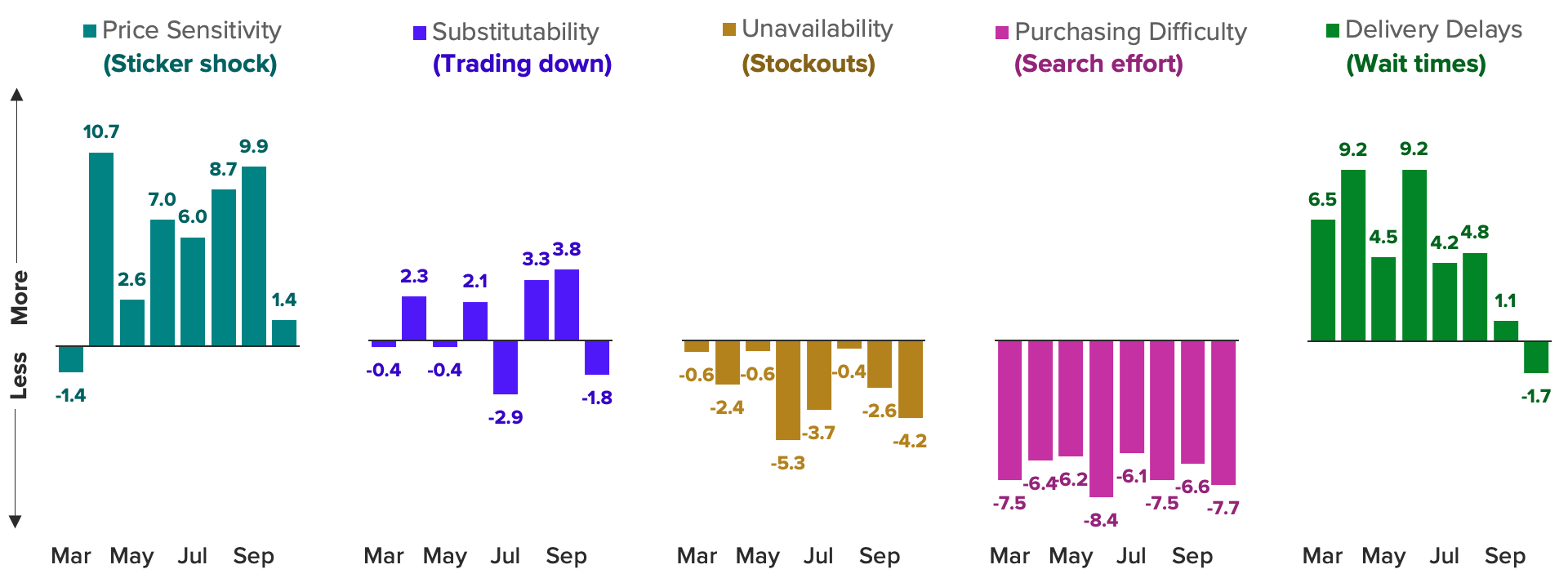

Rising core inflation in August and September coincided with an increase in inflation avoidance behaviors by consumers, as seen in Morning Consult’s Price Sensitivity and Substitutability indexes, which measure sticker shock and trading behavior, respectively, and form the SCICIP’s demand-focused component. October, however, appeared to mark a reversal of this trend: Core inflation posted its smallest gain of 2022, and both sticker shock and trading-down behaviors subsided substantially. All five of the SCICIP declined last month, with the more supply-focused Unavailability, Purchasing Difficulty and Delivery Delays indexes also signaling easing supply conditions for stockouts, search effort and wait times for online orders.

Unlike earlier this year, softening inflationary pressures appear to be broad-based

October was not the first time that core inflation has slowed this year. Similar decelerations occurred in March and July as well, but each time they were followed by a rebound in the rate of inflation the subsequent month. In each instance, there were particular categories where prices made outsize contributions to the slowdown in core inflation. For example, in October, medical care prices declined 0.6%, accounting for close to 20% of the deceleration in core CPI inflation from September to October. Perhaps not surprisingly, some forecasters anticipate this scenario playing out again for November core CPI inflation.

The SCICIP, however, provides several pieces of evidence that the rebound may not be as large as what was experienced in August. For one thing, October was the first time all five SCICIP indexes simultaneously declined. In July, the last time core inflation slowed, only three of the indexes retreated, with stockouts and search effort instead tightening that month. This time, inflation relief is being felt on both the demand (Price Sensitivity and Substitutability) and supply sides (Unavailability, Purchasing Difficulty and Delivery Delays), suggesting that a deeper shift may be at play, with a more persistent impact on November’s CPI inflation rate.

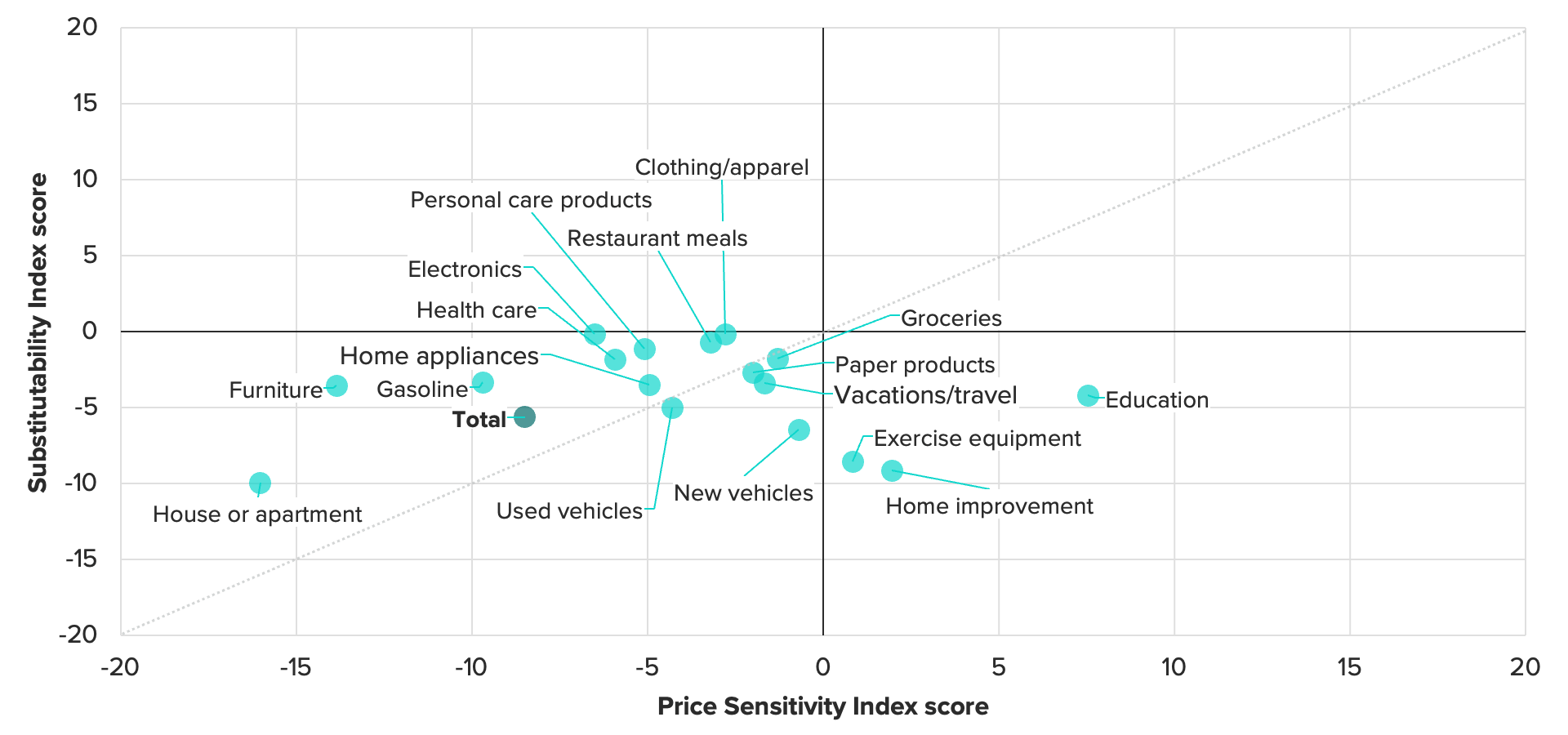

Additionally, signs of inflation relief in the category-level SCICIP were more broad-based in October than they were in July. On the demand side, the net changes in the Price Sensitivity and Substitutability indexes affected nearly every category last month in a positive way (i.e. less sticker shock and trading down), whereas from June to July they were largely driven by just a few categories. A comparison of the net changes in these indexes in each of these months is shown below: In October, all 17 underlying components registered improvement in either trading down, sticker shock or both, compared with only 10 in July. A wide-reaching shift like October’s seems less likely to reverse itself quickly than a narrowly driven one such as took place in July.

Positive signs for consumers, but inflation is far from conquered

That a broad-based trend is likely to be more lasting than a targeted one is intuitive, but objective, statistical analysis of historical relationships supports this conclusion as well. The Cleveland Fed’s nowcast for core CPI inflation is currently pointing to a rebound in November, but at 0.51% it would still mark a downshift from the roughly 0.6% monthly core inflation rates in August and September. Morning Consult’s SCICIP suggests an even more subdued rebound may be possible, pointing to potential downside risk in forecasts such as the Cleveland Fed’s.

To quantify this risk, we construct a SCICIP-implied forecast for November core CPI inflation from a Bayesian regression with data-driven hierarchical shrinkage priors. This forecast exclusively relies on the five SCICIP, therefore translating the indexes in October to a core CPI inflation scale. Shown below in comparison to the Cleveland Fed nowcast, Morning Consult’s SCICIP-implied forecast for November calls for a 0.41% increase in core CPI inflation — higher than in October, but still the fourth smallest increase this year.

Should this SCICIP-implied forecast bear out, it would be a welcome sign for consumers in the critical weeks leading up to the holiday season. Through September, inflation increasingly weighed on demand according to the SCICIP and Morning Consult’s related Consumer Purchasing Power Barometer, with the effects coinciding with several disappointing real retail sales reports. Continued inflation relief could reverse that trend through the end of 2022.

Slower inflation would also indicate progress for the Federal Reserve in its efforts to cool the economy. However, this progress would almost certainly constitute just one step in the right direction on what likely remains a long road: The SCICIP-implied forecast projects annual core CPI inflation of 6.2% in November, down from 6.3% in October and just a touch lower than the Cleveland Fed’s nowcast of 6.3%. Both forecasts, however, are well above the Fed’s 2.0% average inflation target. Thus, while October appears to be a step in the right direction, it is likely only one of many that will be necessary to return to normal levels of inflation.

Kayla Bruun is the lead economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency economic data. Prior to joining Morning Consult, Kayla was a key member of the corporate strategy team at telecommunications company SES, where she produced market intelligence and industry analysis of mobility markets.

Kayla also served as an economist at IHS Markit, where she covered global services industries, provided price forecasts, produced written analyses and served as a subject-matter expert on client-facing consulting projects. Kayla earned a bachelor’s degree in economics from Emory University and an MBA with a certificate in nonmarket strategy from Georgetown University’s McDonough School of Business. For speaking opportunities and booking requests, please email [email protected]

Scott Brave previously worked at Morning Consult in economic analysis.

Sofia Baig is an economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency data. Previously, she worked for the Federal Reserve Board as a quantitative analyst, focusing on topics related to monetary policy and bank stress testing. She received a bachelor’s degree in economics from Pomona College and a master’s degree in mathematics and statistics from Georgetown University.

Follow her on Twitter @_SofiaBaig_For speaking opportunities and booking requests, please email [email protected]