Housing Costs Likely to Keep Bolstering Inflation in 2024

Key Takeaways

Housing prices are recovering after falling precipitously in response to the Fed’s 10 consecutive rate hikes that began in March 2022.

Rebounding price growth appears to be driven by a combination of chronic undersupply and pent-up demand, overpowering the dampening effect of high rents and mortgage costs.

The impact of rebounding home values on overall inflation is likely to be felt in 2024, presenting yet another challenge to the Fed in achieving its 2% target.

Sign up to get our data on the economy, including trends in consumer spending and consumer confidence.

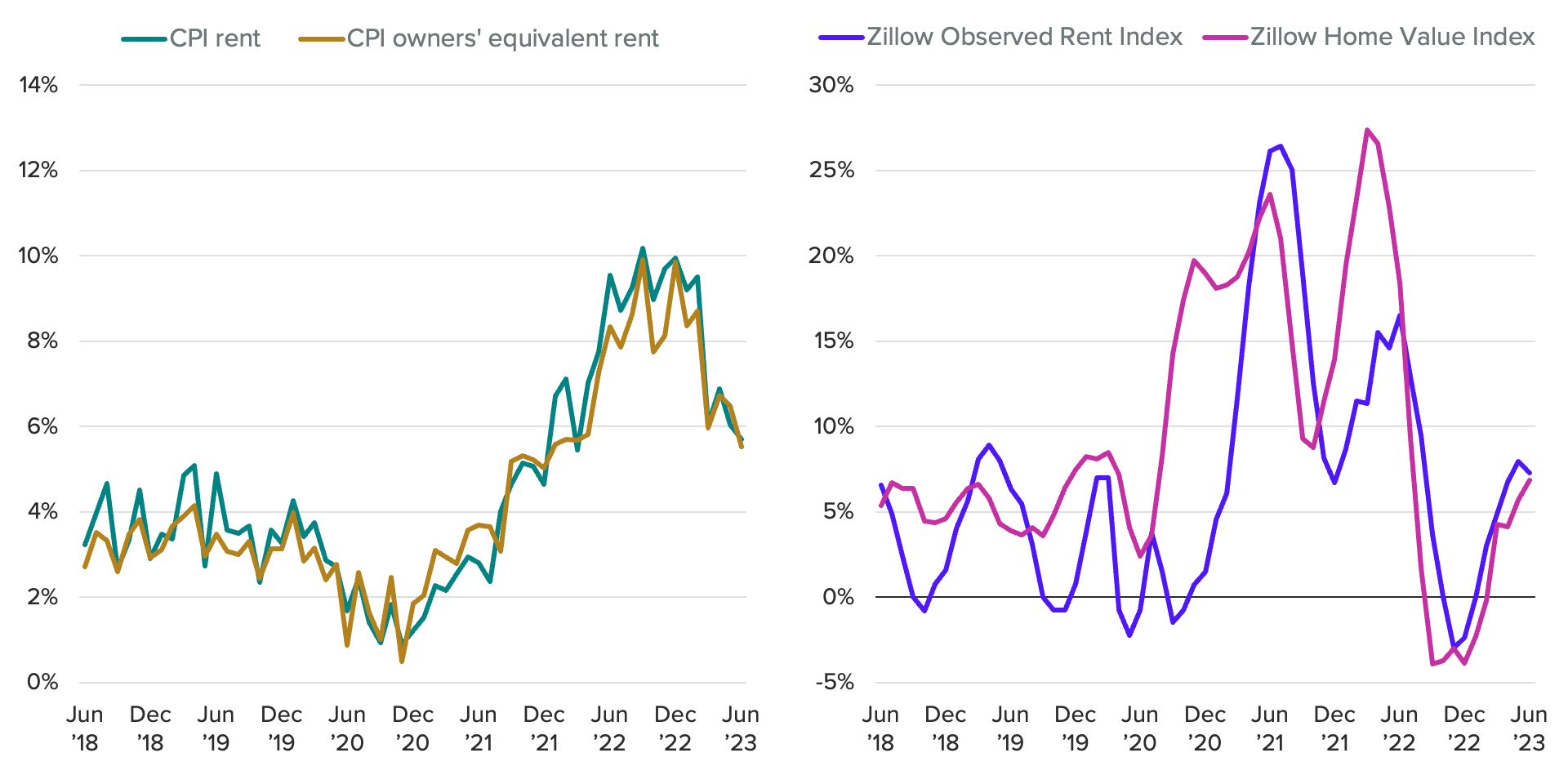

The Bureau of Labor Statistics’ June Consumer Price Index report was met with relief, reinforcing hopes that a soft landing may be attainable. Both top-line and core inflation slowed, driven not only by goods but also by the stickier components including housing and other services.

Due to its lagged nature, the slowdown in the housing price index was not a surprise: More current measures of home values showed a sharp decline last year that was expected to show up in the BLS’ CPI over the second half of 2023. The housing component is likely to slow further over the rest of this year — a critical development toward lowering inflation as the rent and owners’ equivalent rent indexes have on average constituted roughly two-thirds of total monthly core inflation growth over the past six months.

Housing Inflation Measures Are Slowing, but Price Growth Is Poised to Pick Up Again

However, the same measures of price growth that presaged the slowdown are now reversing course: The Zillow Home Value Index and Observed Rent Index have both been climbing for the past several months. Furthermore, despite high prices and elevated interest rates, Morning Consult’s data shows that consumer demand for housing is heating up, while supply remains constrained without much relief on the horizon. Even as top-line and core CPI are just now beginning to show relief from last year’s home price declines, rising price pressures in the housing market may once again push up inflation in 2024.

Homebuying demand is rebounding despite elevated costs

Many prospective homebuyers deferred purchases when the Federal Reserve raised interest rates last year. Those already locked into lower rates were reluctant to give up those mortgages in exchange for steeper interest costs. Through June of this year, Federal Home Loan Mortgage Corp. 30-year fixed mortgage rates have averaged 6.4%, up from 5.3% in 2022 and 3.0% in 2021.

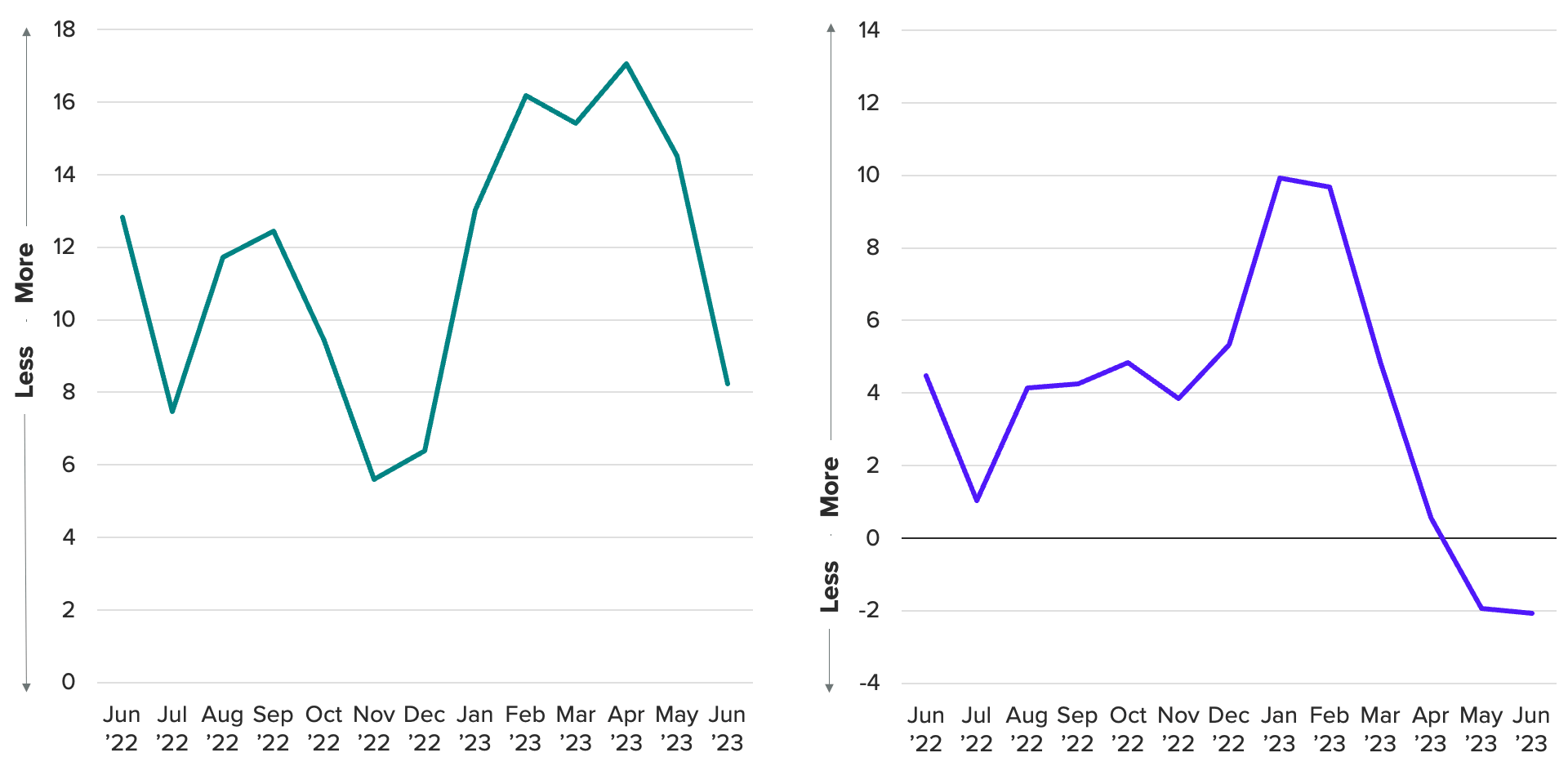

However, pent-up demand appears to have accumulated to the point that buyers are becoming less deterred by high prices and financing costs. Years of limited housing additions relative to population growth have contributed to a backlog of would-be homebuyers, while more recent trends like remote work are encouraging consumers to seek more space, further stoking demand. Over the past few months, Morning Consult’s indexes tracking price sensitivity and trading down for homes and apartments have been declining. Homebuyers are not only less willing to walk away from home or apartment purchases due to price, but they are also less likely to seek out cheaper alternatives. Less trading down may be a result of limited inventory: It’s possible that some buyers might prefer more affordable home options but be unable to locate them.

Consumers Are Increasingly Willing to Make Home Purchases Despite Elevated Costs

3-month moving average

Furthermore, this renewed strength in housing demand looks likely to persist. The share of adults who said they plan to buy a home or apartment in the next 12 months averaged nearly 2 percentage points higher in Q2 2023 compared with the same period in 2022.

Supply remains tight, stoking competition and bidding wars

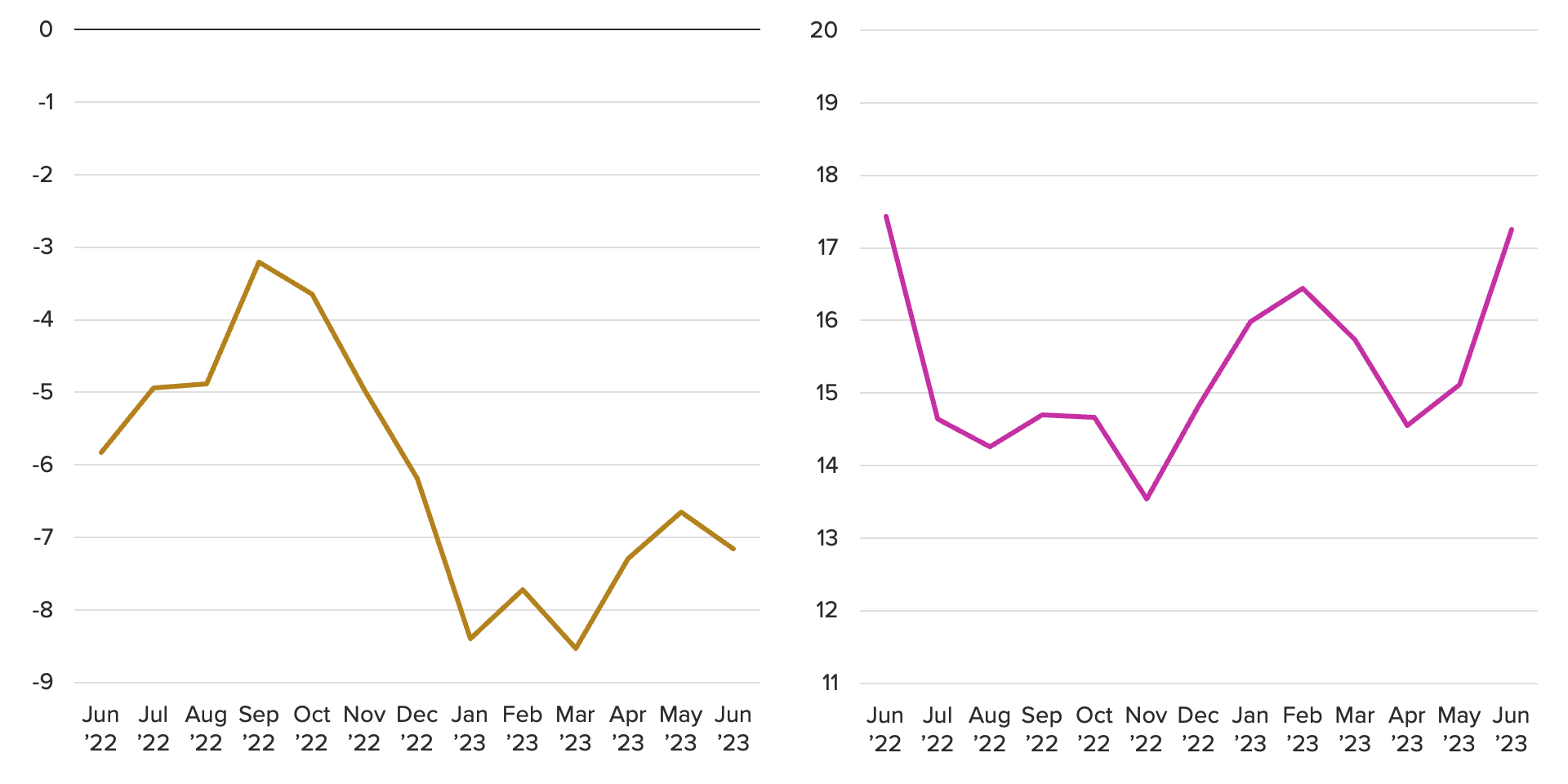

Meanwhile, Morning Consult’s indexes tracking supply pressures in the housing market show that homebuyers are experiencing tighter supply conditions. Both the Unavailability Index and the Purchasing Difficulty Index for housing have rebounded from recent lows. This finding suggests that discouraged buyers are more often failing to complete purchases of homes because they couldn’t find one, rather than because they were unwilling to pay a higher price for one. Stronger demand is likely contributing to scarcity as more buyers compete for — and increase bidding prices on — limited supply.

Finding and Buying Homes Is Becoming More Difficult Amid Scarce Supply, Rising Demand

3-month moving average

Forward-looking housing supply indicators offer little reason to expect much near-term relief. The number of new homes in the pipeline (measured as building permits, starts and under-construction units, from the U.S. Census Bureau data) as a share of total housing stock has been falling since Q1 2022, reversing the long-term trend of gradual recovery following the 2008 financial crisis. Builders are poised to continue adding multifamily units. However, this market — largely composed of renters — is smaller than that of single family homes, with the multifamily pipeline making up only about 1% of total existing housing stock as of Q1 2023.

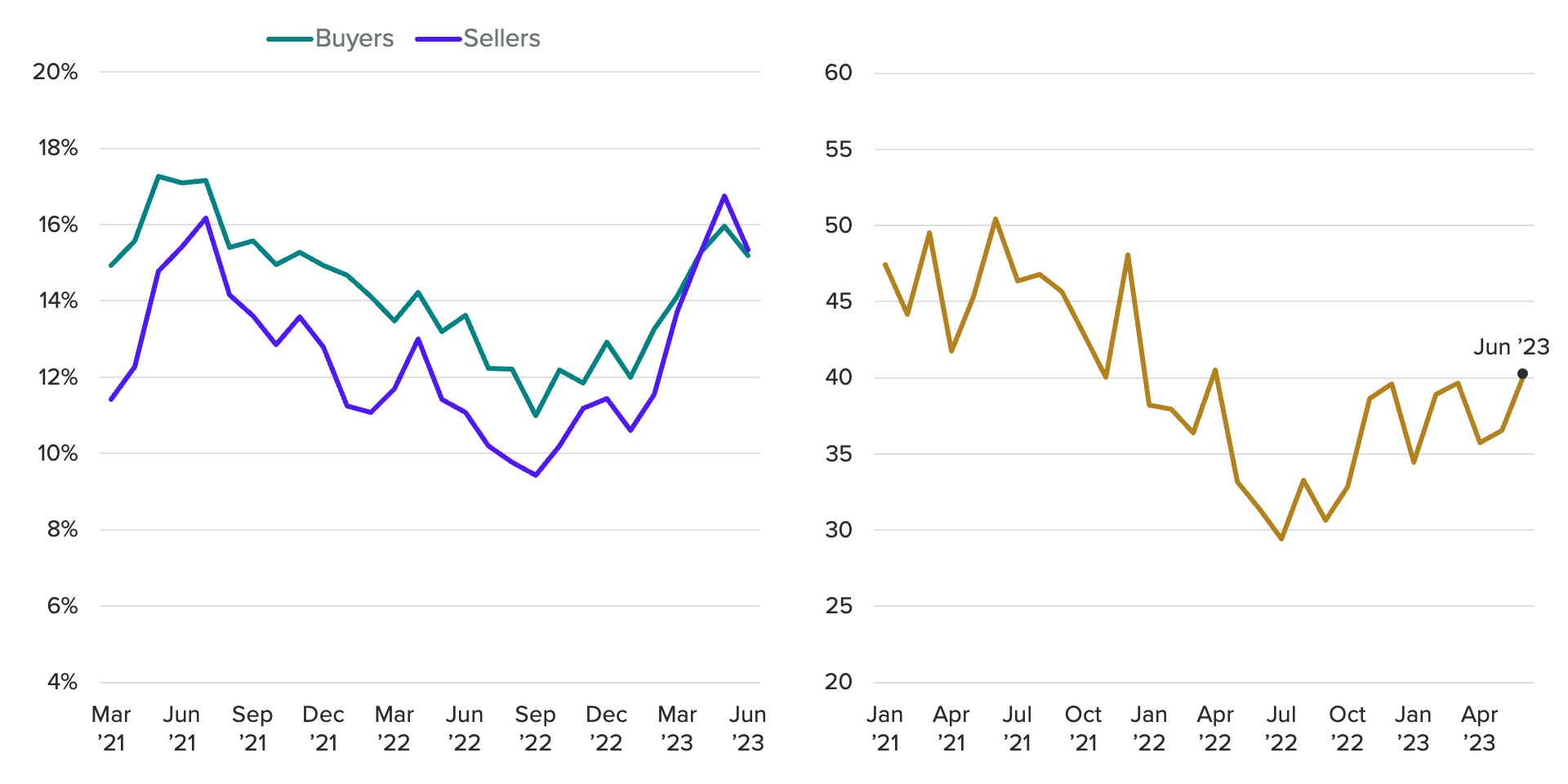

Buying and Selling Are Poised to Pick Up as Home Investment Views Grow Rosier

Although sales of newly built homes have picked up in recent months, existing home sales still made up about 88% of single family purchases over the past year. Morning Consult’s data on homebuying and homeselling intentions offers clues about the direction of the existing home sales market.

What we do that’s different: We survey thousands of U.S. consumers monthly to measure their spending patterns and habits, asking questions on topics including household income, spending, savings, debt, housing payments and more.

Why it matters: Morning Consult’s consumer and spending data provides a detailed assessment of U.S. adults’ self-reported household financial conditions and spending, as well as consumers’ perception of inflation and supply chain disruptions and the impact of both on purchasing decisions.

After the Fed began raising interest rates in early 2022, selling intentions began trending lower. More recently, however, selling intentions have been climbing as home values recover and consumers warm to the idea of homes as investments. In May, the share of adults who said they planned to sell their homes in the next year reached its highest level since tracking began in January 2021, and remained 2 points above its year-ago level in June.

While the prospect of more existing homes on the market may help the undersupply problem, it should be noted that most of these sellers will also be buyers. Any reduction in price pressure from more sellers could be offset by the associated increase in buyers.

Housing components may push up inflation again in 2024

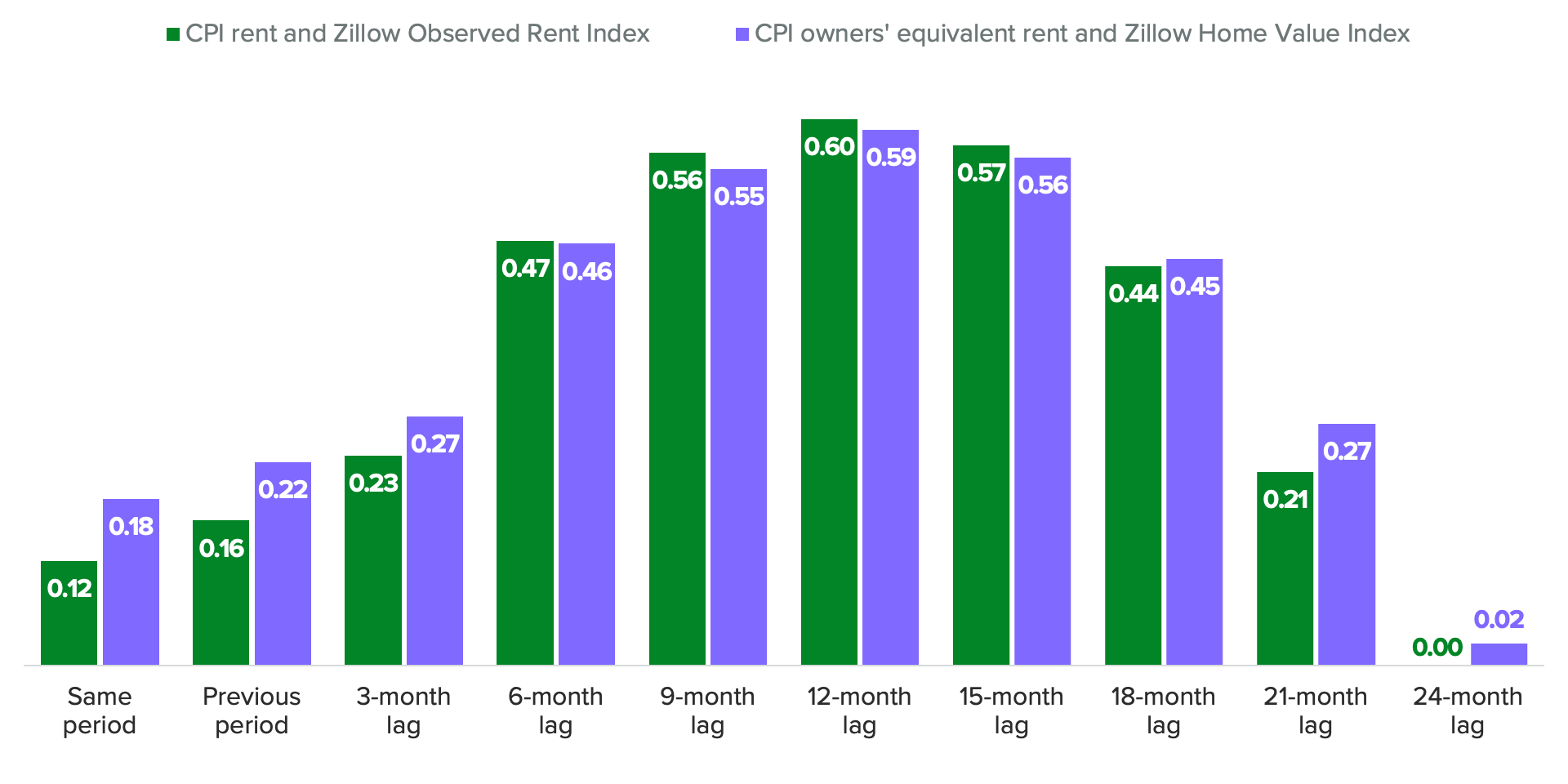

The near-term outlook for the impacts of rent and owners’ equivalent rent on core inflation appears positive in its implications for achieving the Fed’s 2% target. Correlations between rent and owners’ equivalent rent CPIs and their respective Zillow price indexes indicate that changes in home prices typically take about a year to show up in the BLS’ measure of overall inflation. Zillow’s rent and home value indexes showed weak or negative monthly price growth persisting through early 2023, suggesting a period of softer CPI growth is likely to continue through at least the end of this year.

2023 Housing Price Increases Could Push Up Inflation in 2024

However, rebounding home values this summer signal that any slowing in the housing component of the CPI is likely to eventually reverse. Assuming the historical lag relationships hold, the timing of the recent dip and recovery in Zillow’s home and rent prices suggest housing CPI growth will continue slowing through the end of the year before climbing again in 2024. Morning Consult’s forward-looking data indicates that homebuying demand is poised to recover further in the coming months, potentially extending the period of elevated price pressures. Given the large weight of housing on the CPI, escalating price growth for this component could once again be an obstacle to the Fed’s mission to cool inflation down to its 2% target level next year.

Kayla Bruun is the lead economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency economic data. Prior to joining Morning Consult, Kayla was a key member of the corporate strategy team at telecommunications company SES, where she produced market intelligence and industry analysis of mobility markets.

Kayla also served as an economist at IHS Markit, where she covered global services industries, provided price forecasts, produced written analyses and served as a subject-matter expert on client-facing consulting projects. Kayla earned a bachelor’s degree in economics from Emory University and an MBA with a certificate in nonmarket strategy from Georgetown University’s McDonough School of Business. For speaking opportunities and booking requests, please email [email protected]