The Problem With Premium in a Cost-Conscious Post-Pandemic World

Key Takeaways

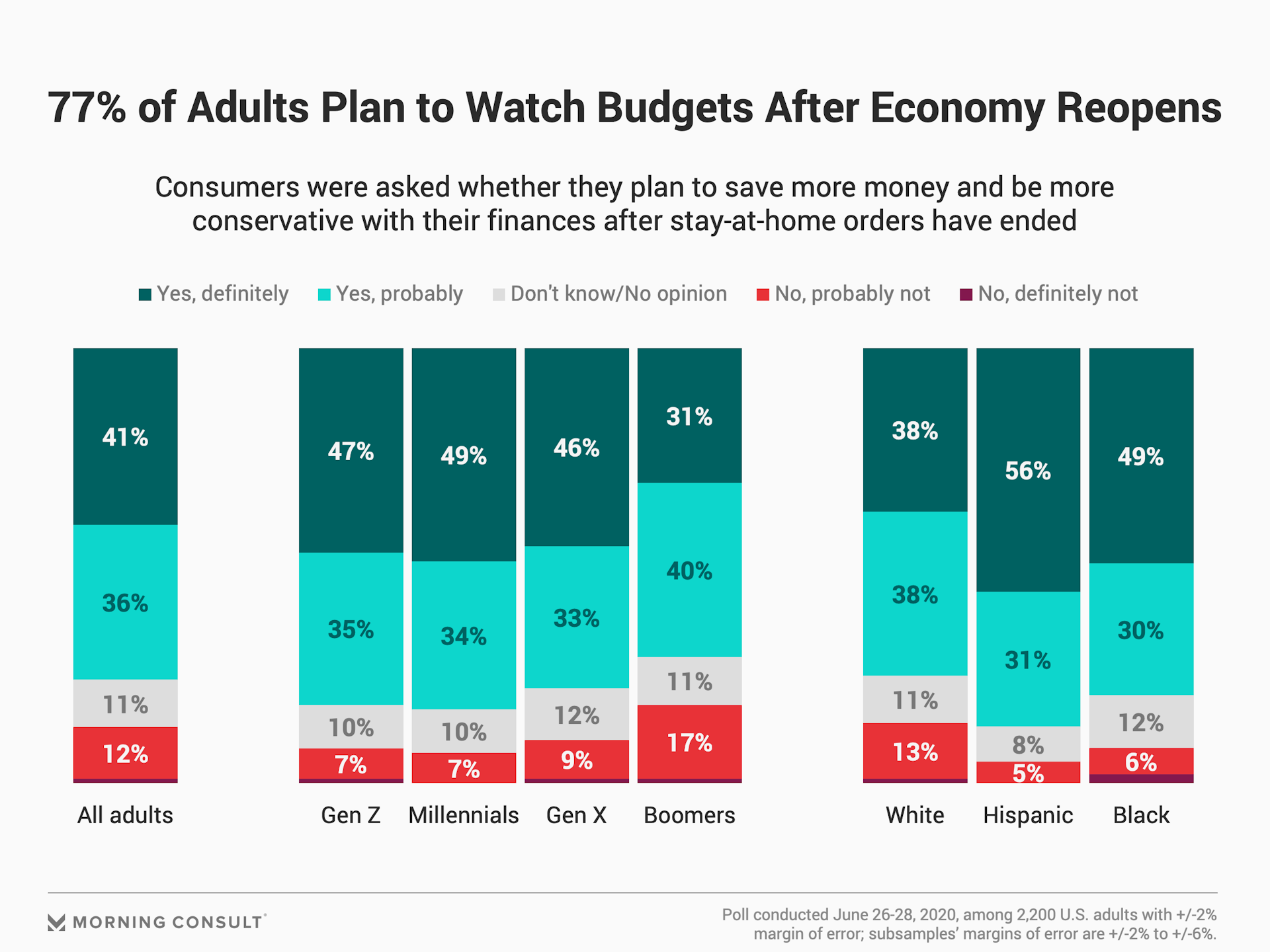

77% of Americans plan to save more and be more conservative with their finances when stay-at-home orders end and economies reopen, 32% plan to save money instead of making purchases more often post-pandemic than they did previously, and 24% say they will compare prices more often post-pandemic.

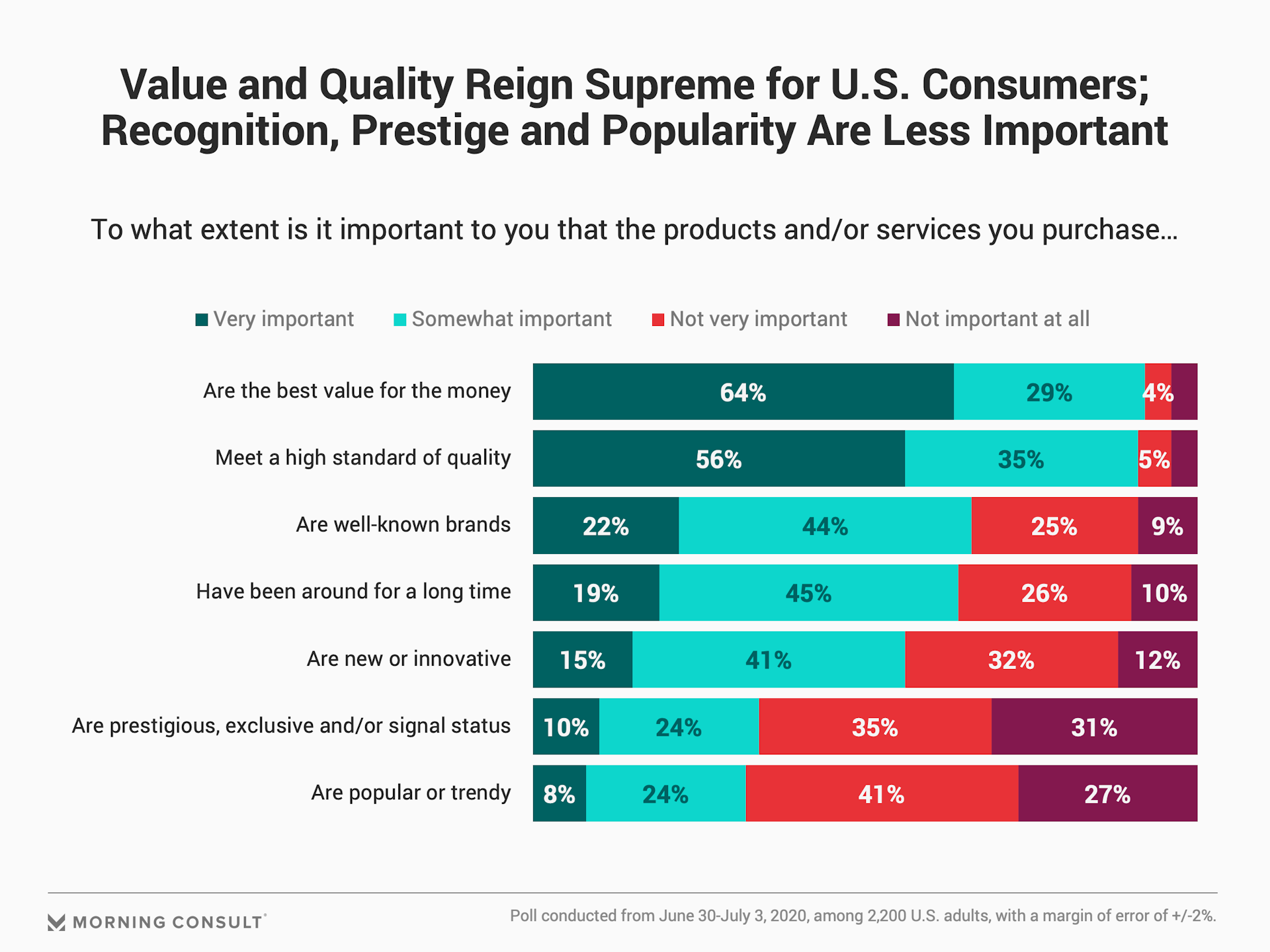

Nearly half of U.S. adults (45%) say that the availability of promotions, discounts or sales is most important to them when considering whether to buy from a company. Also, 93% and 91% of U.S. adults, respectively, indicate that value for money and high quality are must-haves in their purchases these days, while prestige and popularity rank as important for hardly a third of consumers.

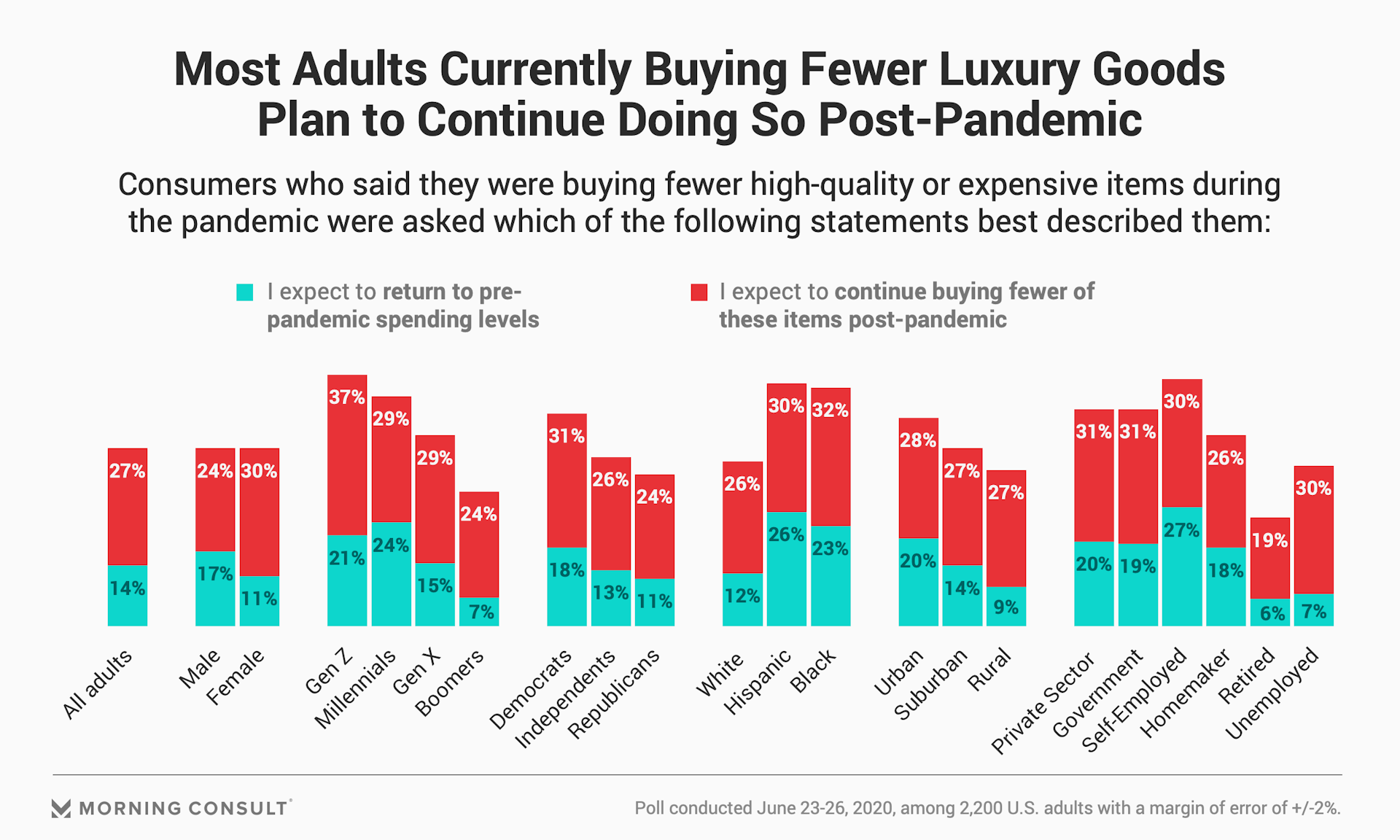

66% of Americans who are currently buying fewer premium items due to the pandemic expect to continue spending less on them post-pandemic; this share rises to 79% among Boomers, 75% among residents of rural communities and 72% among females.

This analysis was authored by Victoria Sakal, Morning Consult’s managing director of Brand Intelligence.

With economic concerns as top of mind as health-related worries these days, it’s no surprise that Americans have been cautious about spending during the COVID-19 pandemic.

But the challenge for businesses big and small lies in whether this trend will fizzle or become a way of life as shelter-in-place mandates lift and consumers have greater freedom to return to their preferred stores, purchasing methods and brands. Amid consumers’ evolving purchasing preferences, the meaning and future potential of value, loyalty, and luxury may be permanently changed in a post-COVID world.

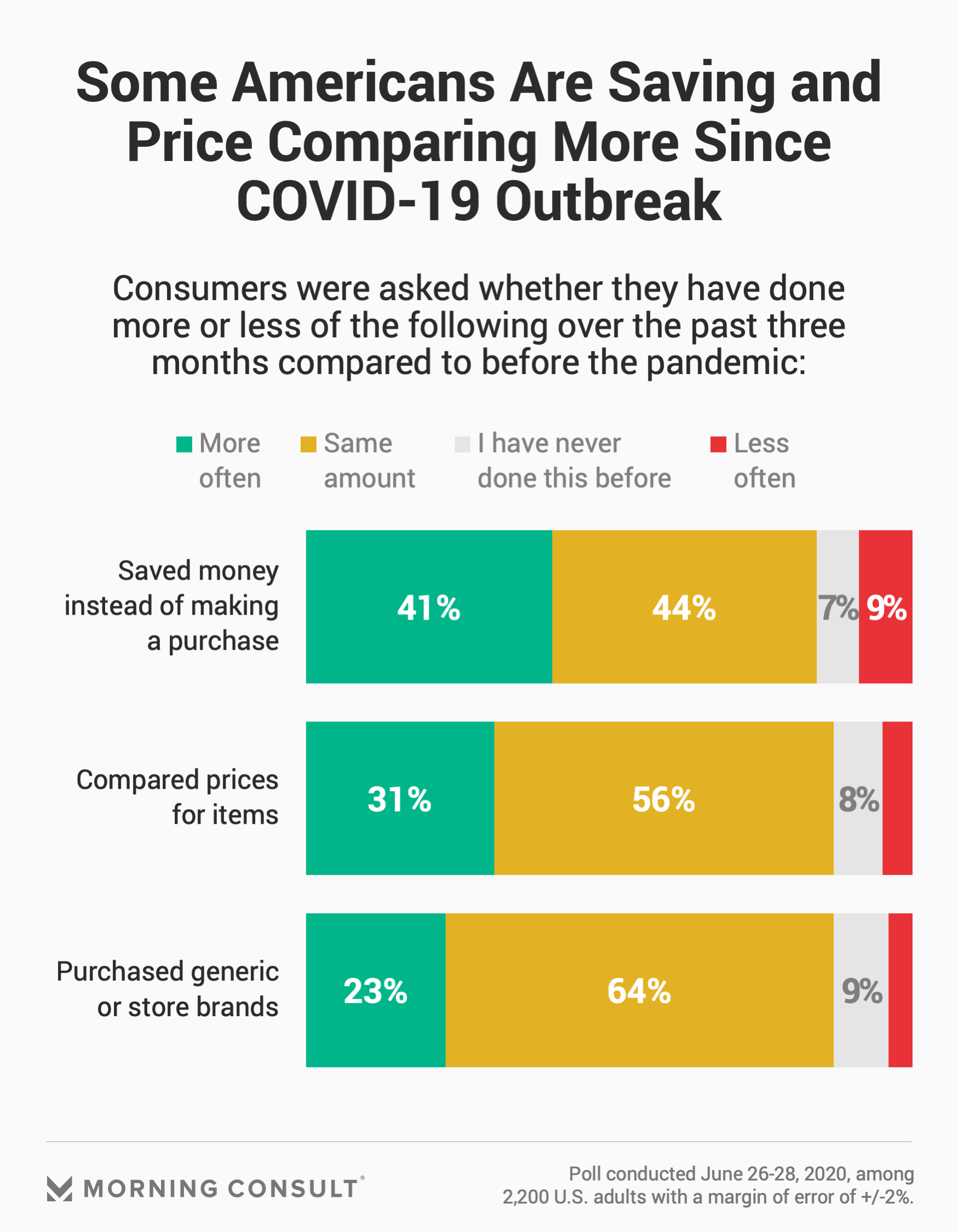

Today, nearly a third of U.S. adults (31 percent) are comparing prices more often before making a purchase, and 41 percent are more frequently opting to save money instead of making a purchase than they tended to pre-pandemic.

When it comes to saving money, Gen Zers are notably more likely than their generational peers to indicate that they've been saving money instead of making purchases since the coronavirus outbreak in March (52 percent say they are doing this more, while 27 percent say they are saving the same amount as they were pre-pandemic). This compares to the near-half of Boomers (51 percent) who are saving about as much as they were previously.

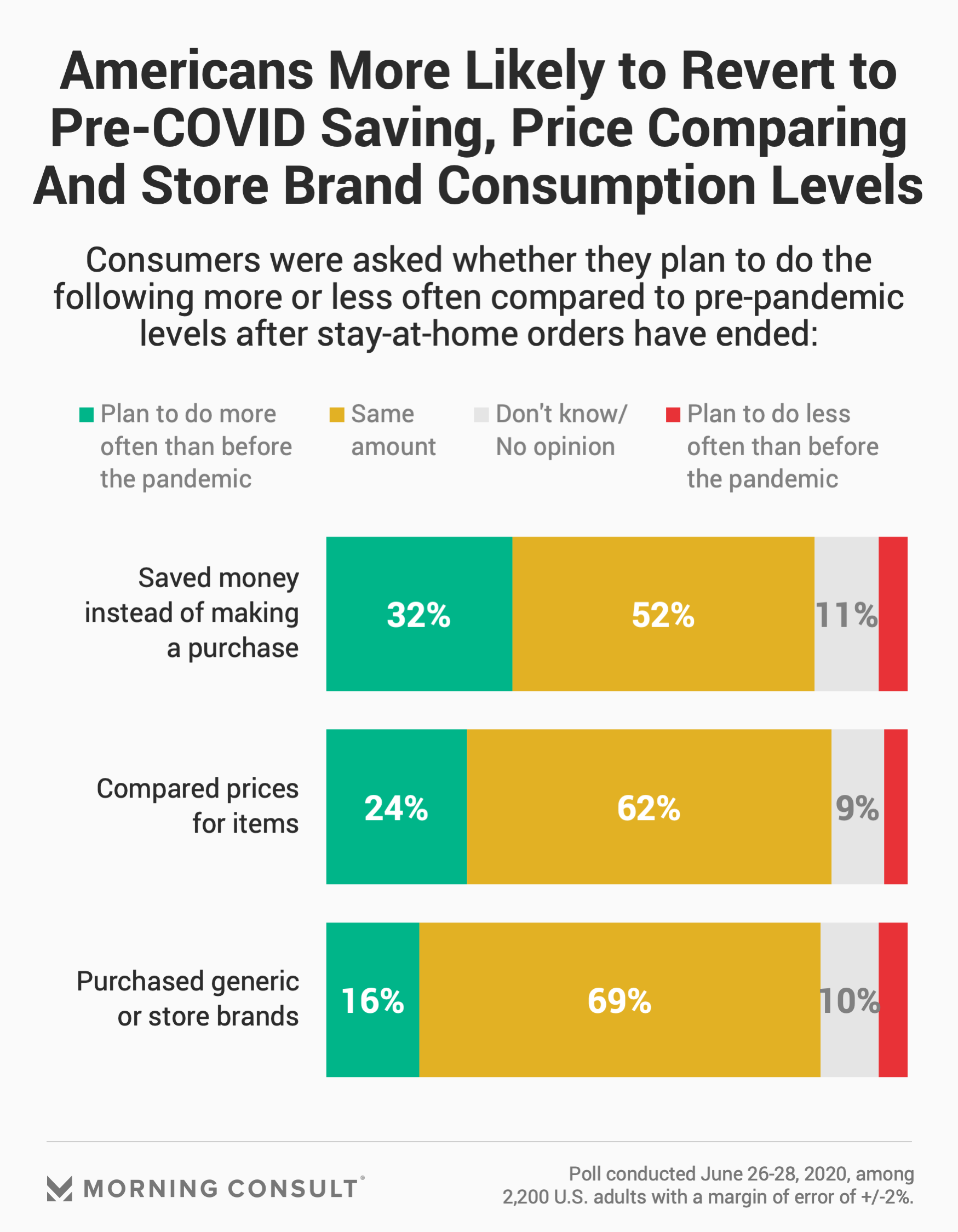

And when stay-at-home orders have ended and economies fully reopen? Fully 77 percent of Americans plan to save more and be more conservative with their finances, with nearly a third (32 percent) indicating they will opt to save money instead of making a purchase more often post-pandemic than they did before, and nearly a quarter (24 percent) indicating they will more often compare prices post-pandemic.

While Gen Z is the generation most likely to indicate they're not yet certain how they’ll behave spending-wise post-pandemic, they are sure of one thing: They're not planning to return to pre-pandemic saving levels. Compared to the 52 percent of all U.S. adults who say they will save money instead of making a purchase the same amount post-pandemic, 36 percent of Gen Z say they will do so, and this generation is also much more likely than elder ones to indicate that they'll do this less post-pandemic.

While Boomers in particular plan to snap back to pre-pandemic spending levels, Gen Z’s relative openness to shifting their post-pandemic spending habits creates opportunities for brands to get noticed by, relate to and form relationships with this increasingly powerful cohort of consumers as groundwork for the next normal.

Still, it’s no surprise that consumers’ rising financial pressures and falling confidence, coupled with uncertainty around the timeline for economic and global health recoveries, tend to most severely handicap big-ticket items, as well as luxury or premium goods.

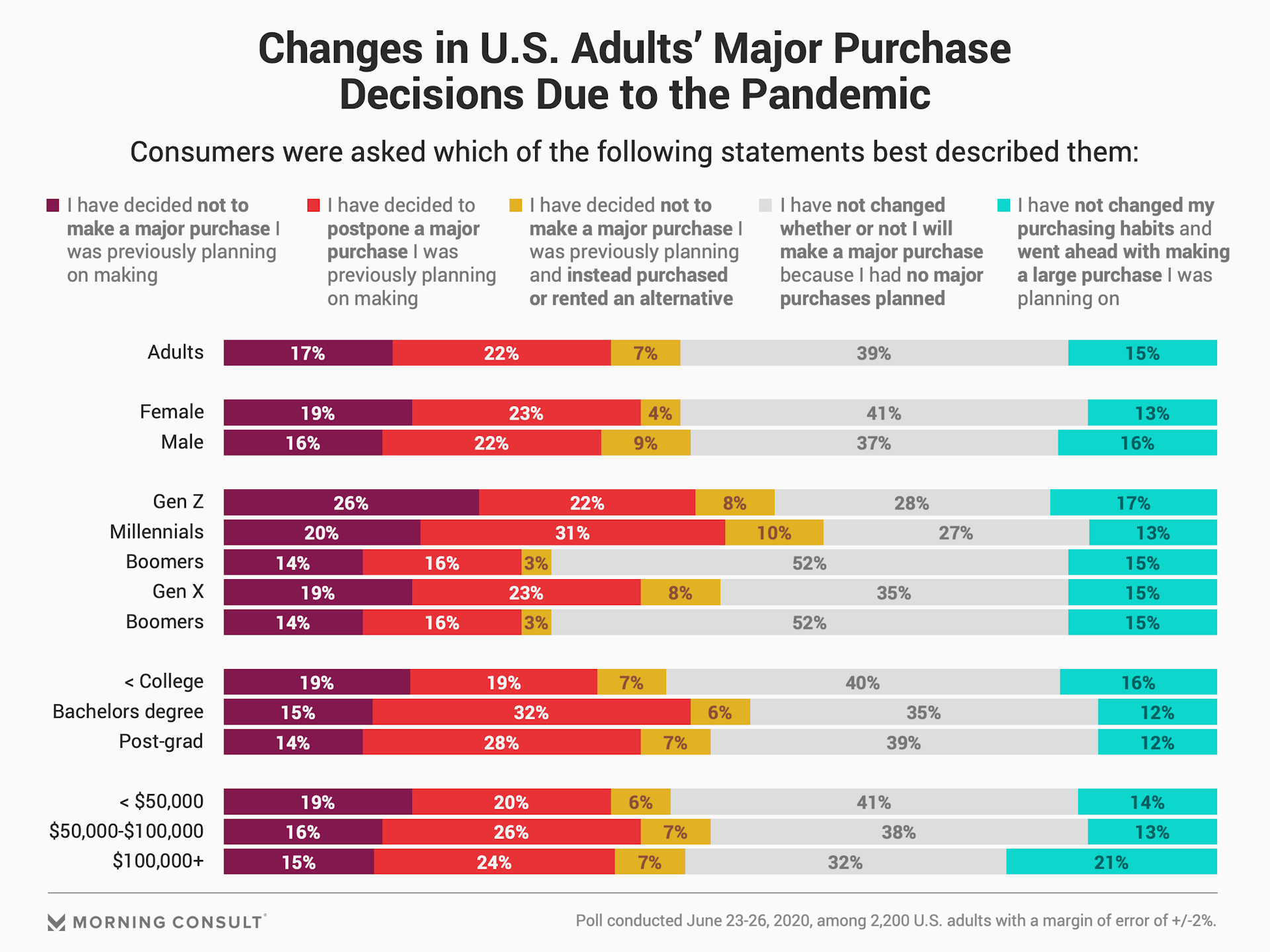

Indeed, the pandemic has led about a fifth of the population (22 percent) to postpone a major purchase due to the pandemic, and another near-fifth (17 percent) has entirely called off a major purchase they were planning to make.

Millennials are significantly more likely than their generational peers to have postponed major purchases, while Boomers are significantly less likely to have done so, though largely because more than half of this generation (52 percent) had none planned in the first place. Men are 5 points more likely than women to substitute a planned purchase with an alternative, suggesting that both spending behaviors and brand loyalties vary along gender lines.

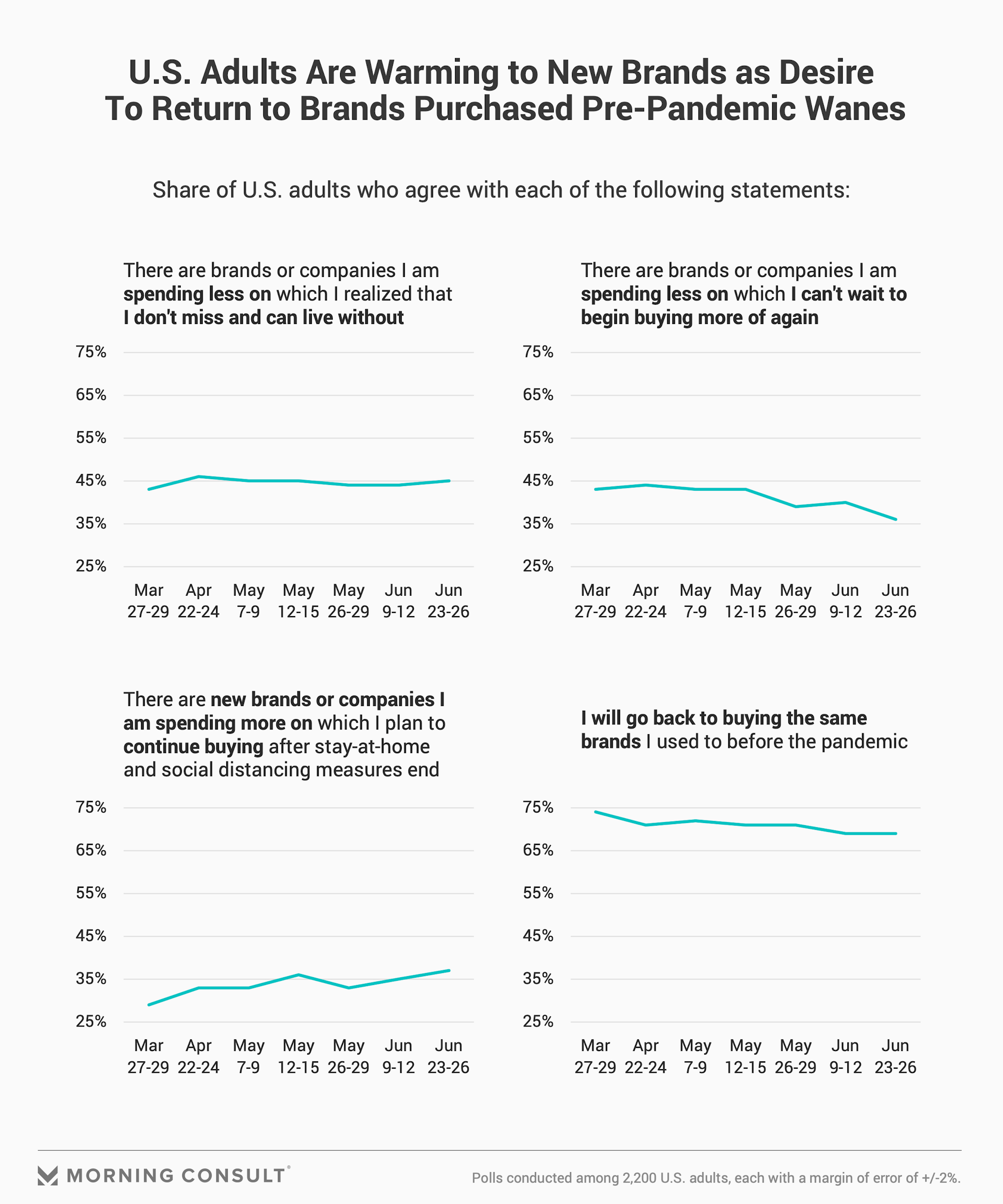

Delayed or canceled purchases are troublesome at a time when brand loyalties are decidedly shifting. Just 7 percent of U.S. adults report having swapped a major purchase for an alternative solution but, more generally, 39 percent of Americans say that moving forward, they will find an alternative for unavailable items. Though a similar portion of adults, 4 in 10, would rather wait to buy a preferred brand or item in the future, ongoing Morning Consult tracking reveals that the share who says there are new brands or companies they are spending more on which they plan to continue buying after stay-at-home and social distancing end has risen by 28 percent since March.

Considered in conjunction with a 16 percent drop in the share of people who can’t wait to resume buying certain brands they’ve been spending less on since the pandemic broke -- and a continued decline in the share of adults who say that they will go back to buying the same brands they used to before the pandemic -- it’s clear that out-of-sight brands, stores and options are very much at risk of being pushed out of mind, whether because exploration has led to adoption, or because pandemic-induced postponement has rendered certain purchases altogether nonessential.

If consumers are embracing either product substitutes or even life without big purchases altogether, it’s worth considering what the future holds for premium and luxury goods, whose livelihood is rooted in not only consumers’ financial stability, but also the prestige and appeal of higher-end goods.

With nearly half of U.S. adults (45 percent) saying that the availability of promotions, discounts or sales is most important to them when considering whether or not to buy from a company, traditionally American dynamics around consumption, loyalty and even materialism may be facing a turning point: 93 percent and 91 percent of U.S. adults, respectively, agree that value for money and high quality are must-haves in today’s purchases, while prestige and popularity rank for hardly a third of consumers.

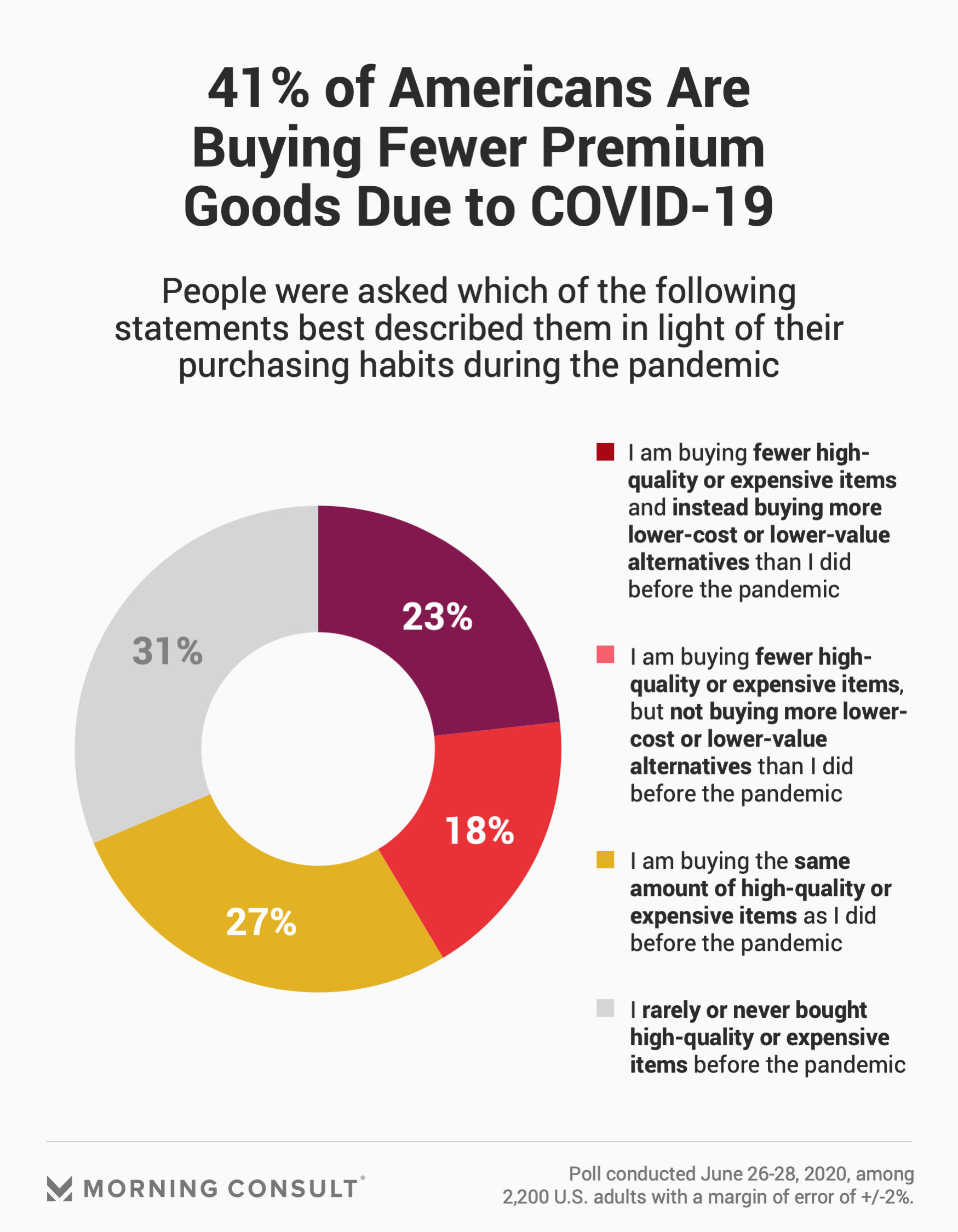

Given these emergent preferences and the economic backdrop, Morning Consult research conducted late June finds most adults (41 percent) buying fewer high-quality or premium items since the outbreak (vs. 31 percent saying they never bought these items in the first place, and 27 percent buying the same amount). Of those buying fewer premium items, about half are trading down to lower-quality alternatives. This mirrors trends observed in Morning Consult Brand Intelligence tracking data since the coronavirus outbreak in March, where luxury brands have endured a more pointed drop in favorability, value and even likelihood to recommend than all brands on average have.

Looking to the future, when finances are freer and options are more abundant, a clear majority of adults buying fewer premium goods at this time (66 percent) expect to continue doing so. This share rises to 79 percent among Boomers, 75 percent among those living in rural communities and 72 percent among women, meaning premium brands targeting these audiences have an especially uphill battle ahead of them.

The implications for luxury brands are clear, if not multifaceted: For the near-quarter of the population that hasn’t cut back on premium purchases, maintaining (and strengthening) relationships is critical for defending this core customer base. With those who indicate that they have reduced spending on high-quality and premium goods only temporarily, brands would be wise to sustain awareness via communication and engagement -- perhaps even expressing empathy for customers’ strained circumstances while also stoking excitement for a brighter future -- to increase likelihood of nearer-term purchases as “normalcy” returns. And finally, playing defense through strategic use of data, insights and hyper-relevant offers will be essential for winning back consumers otherwise happy to defect from luxury spending altogether.

Strained spending has been compounded by increased exploration, wavering loyalty and a waning sense of reliance on material goods to create a perfect storm of new purchasing habits. As consumers increasingly embrace conservatism, interchangeability and value, high-end goods anchored on exclusivity, popularity and the luxuries of life may need to forge a new path to purchase in a post-pandemic world.

Victoria Sakal previously worked at Morning Consult as a brands analyst.