As Forbearance Protections End, Nonbank Mortgage Lenders Face High-Volume Processing Tests, Ginnie Mae Risks

Key Takeaways

A strong housing market has eased concerns about a widespread wave of defaults, but questions about nonbank mortgage servicers’ ability to handle the expected high volumes of loan modification requests and foreclosures remain.

Nonbank mortgage servicers dominate the Ginnie Mae market, which includes more first-time homebuyers and people of color.

Tech-savvy millennials fled to the suburbs during the coronavirus pandemic, fueling a hot housing market that enabled nonbank and fintech mortgage companies to grab a big piece of the growing market share, churning out loans at a faster pace than more traditional bank lenders.

That booming market has so far shielded a vulnerability. Homeowners had multiple options to buoy their finances, from refinancing opportunities to extra unemployment insurance and stimulus checks. As those programs come to a close this year, most homeowners that took advantage of coronavirus-era policies to delay their loans have now exited forbearance, staving off a widespread, 2008-style foreclosure crisis that many feared at the start of the pandemic.

But for a portion of borrowers -- largely Black, Hispanic and first-time homeowners -- the end of housing programs could pose significant difficulties.

Can nonbanks handle the volume?

The issue has to do with nonbank servicers that have never dealt with the number of loan modification requests and foreclosures that policymakers expect, and who aren’t required, like banks, to hold capital in reserve to offset the costs. These servicers, which handle the day-to-day managing of a mortgage, including foreclosures, have aggressively taken market share since the Great Recession and the regulation of bank mortgage lending that followed.

Mortgage servicers and other industry-watchers were on alert for these issues early in the pandemic, even unsuccessfully lobbying the Federal Reserve for a liquidity facility for nonbank mortgage servicers.

And though a widespread liquidity crisis reminiscent of the 2008 crisis now appears unlikely, experts are worried about logistical challenges with everything from high-touch transactions like loan modifications or foreclosures to a lack of infrastructure to service loans in foreclosure.

“Some of these servicers are not prepared and haven’t been prepared financially for the wave of loan modification requests that are going to be inevitable at the end of the foreclosure moratorium,” said Chris Odinet, a law professor at the University of Iowa who has written about fintech and nonbank mortgage servicers.

Recently, the Consumer Financial Protection Bureau released a rule meant to ease stress on the system and protect some homeowners from foreclosure and usher them into loan modifications, but servicers have complained that such rules could increase compliance costs.

In issuing the rule, the CFPB said that a “potentially historically high number of borrowers will seek assistance from their servicers at approximately the same time this fall, which could lead to delays and errors as servicers work to process a high volume of loss mitigation inquiries and applications.”

Ginnie Mae’s vulnerabilities

The risk is especially high for servicers of Ginnie Mae securities, where nonbanks dominate -- roughly 75 percent as of the end of June, according to the mortgage analytics company Recursion. Ginnie Mae guarantees securities backed by loans insured by the Federal Housing Administration, Department of Veterans Affairs’ Home Loan Program for Veterans, the U.S. Department of Agriculture’s Rural Development Housing Programs and a Housing and Urban Development Office of Public and Indian Housing program.

Ginnie Mae declined to comment on this story.

These borrowers are more likely to default and go into foreclosure than Fannie Mae and Freddie Mac-backed loans because they’re more likely to be vulnerable groups, such as minorities and first-time buyers.

Plus, it can be more costly to service Ginnie Mae guaranteed securities, because it only acts as a guarantor instead of purchasing loans from originators and issuing securities like Fannie and Freddie. That means servicers take on a higher risk in case the borrower defaults.

And not only do nonbanks have a high share of Ginnie Mae-backed securities, they also face more turmoil when, eventually, the end of COVID-era forbearance policies start resulting in foreclosures and modifications.

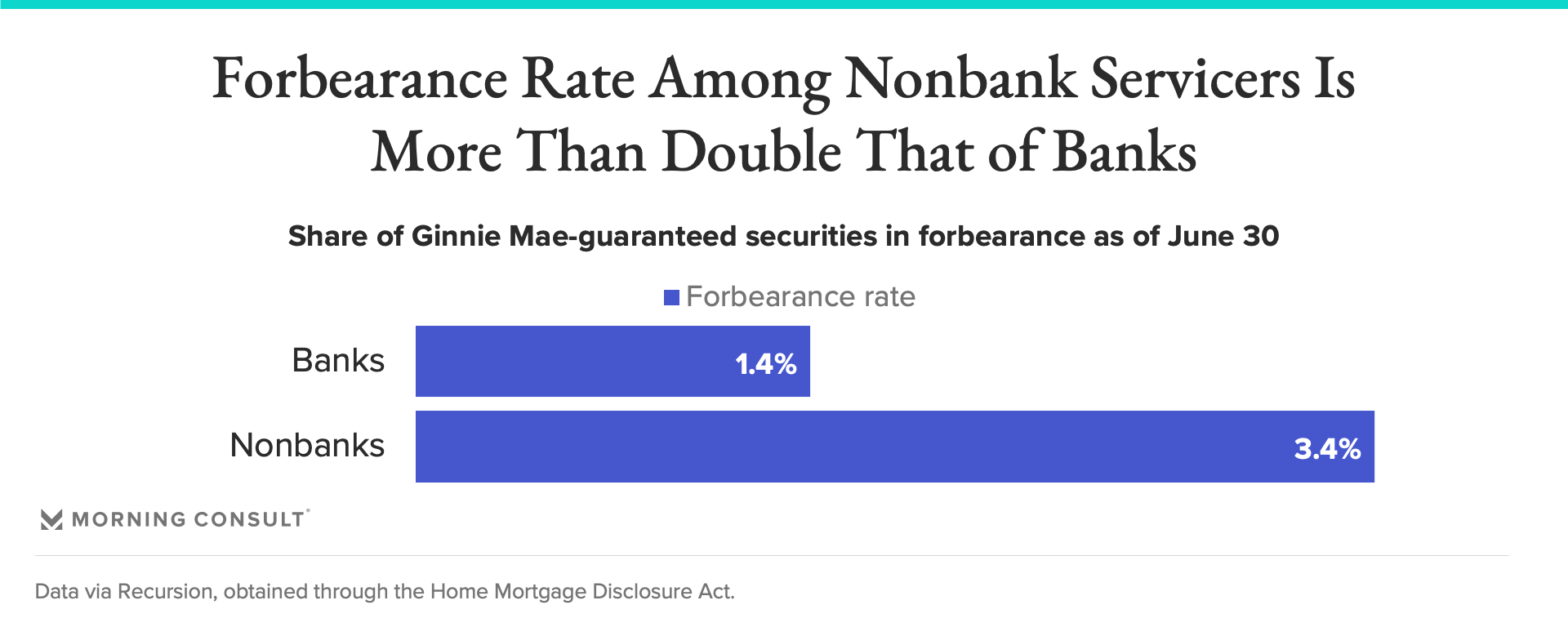

Loans that are serviced by nonbanks have nearly double the forbearance rate of those serviced by banks in Ginnie Mae-backed securities, according to data from Recursion. Both figures are comparatively low to where they were at the height of the pandemic, but the higher nonbank number shows that these companies could be more exposed to a housing downturn.

For borrowers, especially first-time homebuyers or others that are in FHA, VA or other Ginnie Mae-backed programs, that could have dire consequences, such as the “very real fear” of a servicer modifying a borrower’s loan without assessing if that’s the best option because of a lack of training or experience, Odinet said.

Areas of concern and confidence ahead

The cost of servicing a delinquent loan is also more expensive than it was in 2008 due to CFPB regulations, said Richard Koss, chief research officer at Recursion and a former economist at Fannie Mae, putting pressure on this newly powerful crop of servicers.

“During the financial crisis, there were all of these horror stories about people at servicers just not answering their phone calls, and people lost their homes because they just didn’t know what their options were,” Koss said. “Servicing is a money-making machine in a boring market, but if things turn bad and people stop paying, it’s not so fun anymore.”

With climbing housing prices nationally, “most mortgage borrowers have quite a bit of equity in their home, so even if they can't make payments, their foreclosure risk should be quite low,” said Andreas Fuster, a finance professor at the Swiss Finance Institute @ EPFL who’s written about fintech mortgage lending during the pandemic. That dynamic means that if worse comes to worst, homeowners could sell “at a price that is high enough to cover their mortgage.”

Michael Fratantoni, chief economist at the Mortgage Bankers Association, noted that far more people have come off mortgage forbearance than expected in the tail end of the pandemic, and he expects the adjustment to be fairly smooth.

“Be wary of a headline that says foreclosure numbers spiked; remember we’re starting from essentially zero throughout the pandemic,” he said. “Some servicer costs will increase, but hopefully that will be for a relatively short period of time.”

To be sure, the concerns that arose at the beginning of the pandemic could resurface next time there’s an economic shock. Refinancing and homebuying did a lot to buoy borrowers, and without low interest rates, significant government support for consumers and a pandemic in which people specifically went out looking for more space for their families, it’s easy to see how it could have gone another way.

In a report released earlier this month, the Federal Reserve Bank of Cleveland posited “a shock with a less positive outcome: a situation in which servicing income is interrupted and there is no concurrent fall in interest rates and no increase in refinancing activity.”

Claire Williams previously worked at Morning Consult as a reporter covering finances.

Related content

As Yoon Visits White House, Public Opinion Headwinds Are Swirling at Home

The Salience of Abortion Rights, Which Helped Democrats Mightily in 2022, Has Started to Fade