Analysis: How Much Will the $1,400 Stimulus Check Help Financially Vulnerable Americans?

Key Takeaways

There are decreasing economic and social returns for including households that make over $100,000.

Extending unemployment benefits through September and adopting automatic stabilizers mitigate the risk that virus mutations or labor market scarring will limit Americans’ ability to replace support from the government with income from work by August.

The lack of data-driven debate regarding the third stimulus package reflects the scarcity of data on households’ finances. To date, the focus has been on how a stimulus package will impact consumer spending, but it is not clear how President Joe Biden’s proposed $1,400 stimulus check for eligible households will affect Americans’ ability to pay their bills.

Conventional economic data such as gross domestic product and high-frequency consumer spending data both measure economic output. Similarly, aggregate personal saving data offers no insight into the distribution of savings across the population. While these data sources offer important insight into the likely impact of fiscal spending on the economy, they only tell part of the story.

To assess the impact, amount and eligibility of a third stimulus package, Morning Consult analyzed its proprietary tracking data on household finances, which offers insight into the current condition of households’ balance sheets.

Using this data, this analysis argues that a third round of $1,400 stimulus checks more narrowly targeted to low-income adults and parents combined with enhancements to the country’s unemployment benefit system would prevent unnecessary financial hardship and mitigate future economic risks.

$1,400 would help many Americans avoid financial hardship through July

The purpose of fiscal spending during a recession is not only to boost short-term economic activity; it’s also to provide financially vulnerable households with enough money to avoid unnecessary financial harm. As a society, delinquencies and defaults are inefficient and costly uses of resources, and financial uncertainty prevents families from investing in their futures. During recessions, it’s cheaper for the country as a whole to keep people out of financial trouble than it is helping them fight their way back.

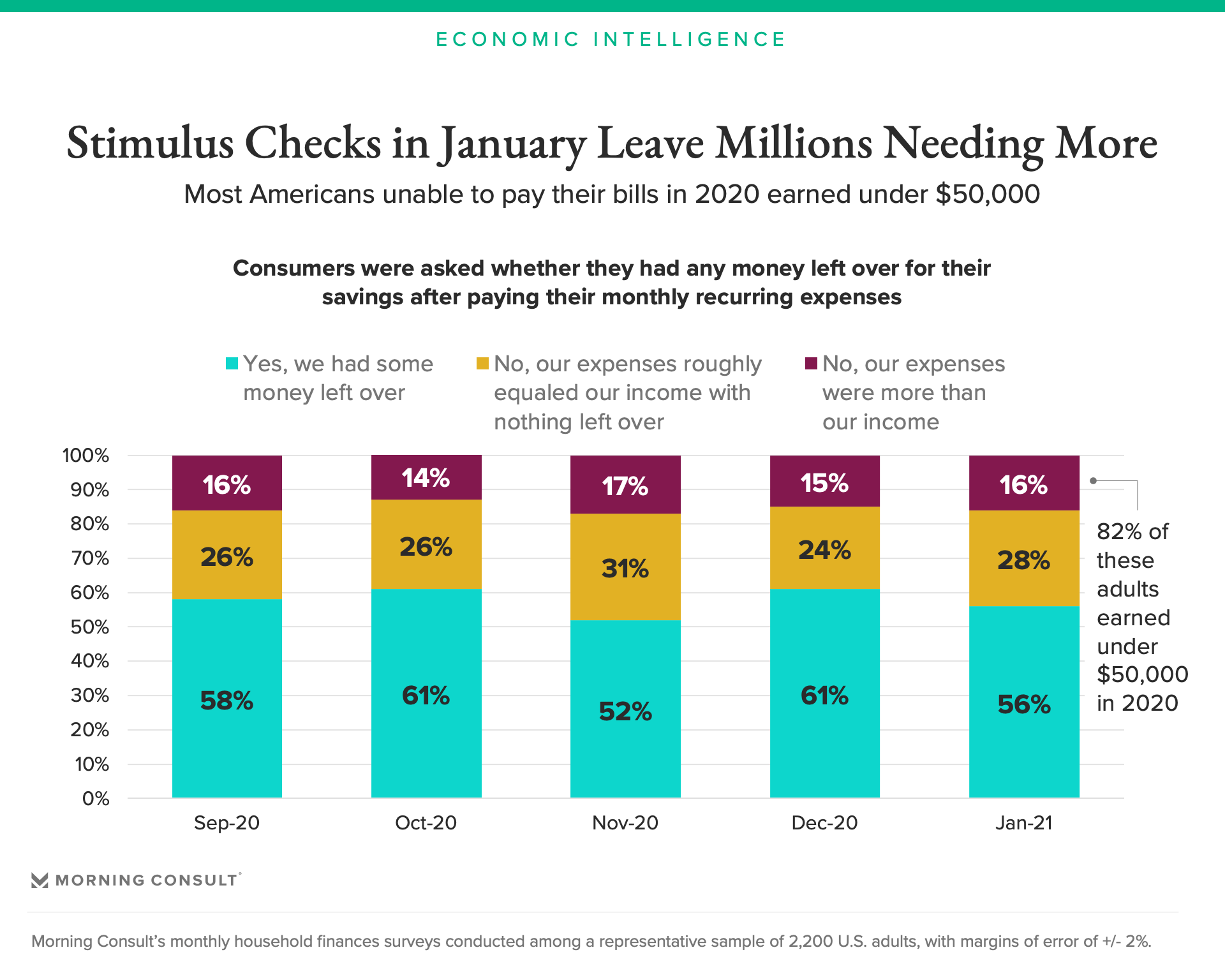

Despite the second round of stimulus checks in January, the number of adults who experienced financial hardship in January remained relatively unchanged from December. In January, 16 percent of survey respondents indicated that their expenses exceeded their incomes for the month, from 15 percent in December. This financial suffering was concentrated among low-income households ($50,000 or less in annual income), underscoring how severely pay losses have been concentrated among low-income adults during this recession.

Based on these survey results, roughly 30.2 million adults in January were unable to pay their bills.

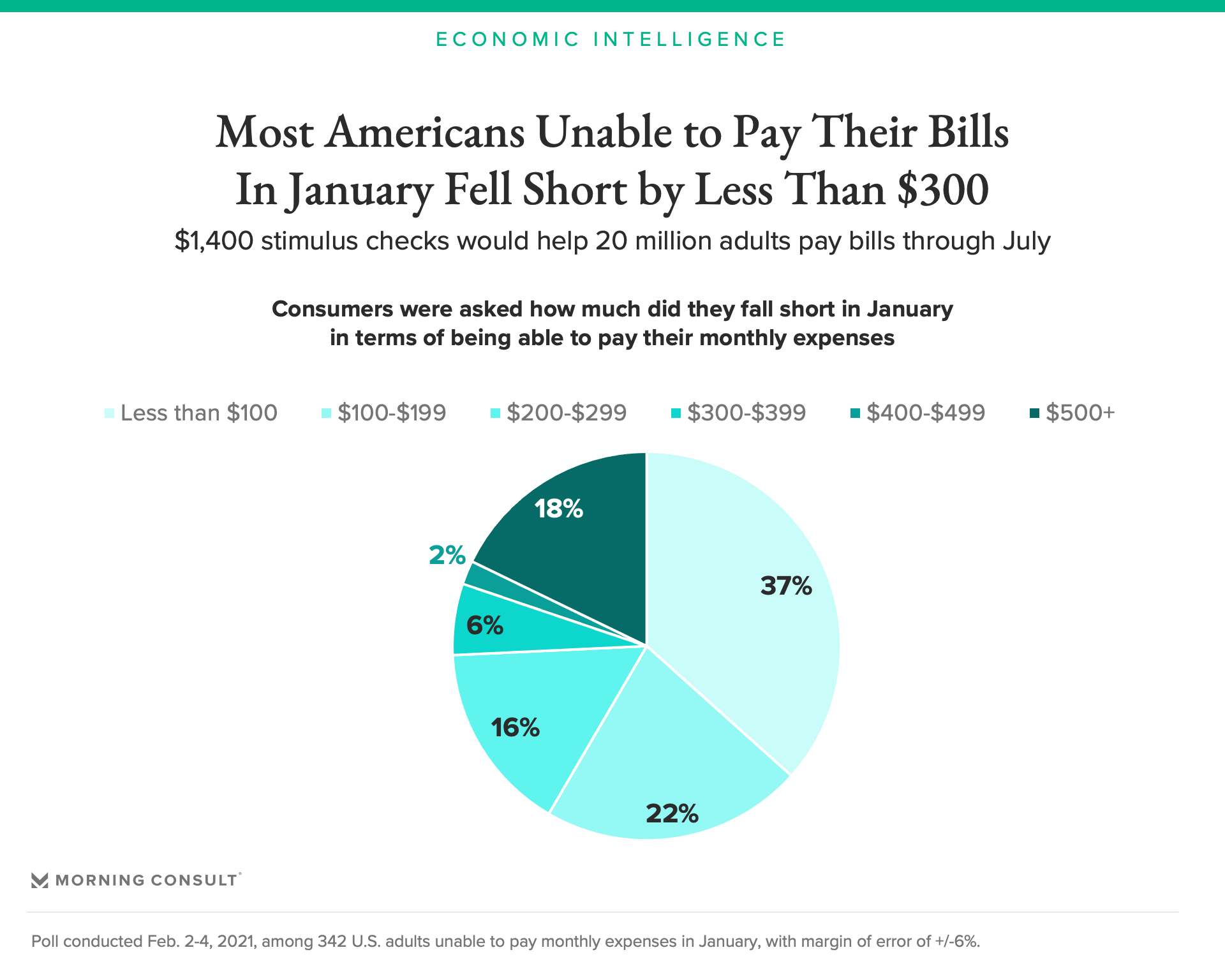

Among these 30.2 million adults, 75 percent of them fell short of paying their monthly bills by less than $300, a 7 percentage-point improvement from December. In other words, the stimulus checks have not dramatically changed the number of people unable to pay their bills, but it brought them closer to paying their bills.

A $1,400 check would allow 22.6 million adults to pay their expenses for at least four and a half months without incurring additional debt or eating further into their depleted savings, assuming that they maintain income from work and unemployment benefits. If the checks are sent on March 1, these payments would allow 22.6 million Americans to pay their bills in full through the middle of July.

The proposed stimulus plan provides noticeably less relief for the remaining 7.5 million adults unable to pay their bills in January. For most of them, their incomes fell short of their expenses by over $500 in January. The cost of protecting them from financial hardship for four or five months would be high, and the economic benefits would be comparatively small since they account for such a small share of the population.

This group needs additional financial help, but stimulus checks are too blunt of a tool for them. The cost of sending significantly larger stimulus checks to everyone far outweighs the benefits of helping relatively few additional Americans.

If the United States is able to successfully achieve widespread vaccinations by the end of June, then economic activity should accelerate in July as increasing consumer comfort drives spending and employment, making government support less necessary during the second half of the year. While vaccine mutations and labor market scarring pose serious risks to this baseline outlook, improvements in unemployment insurance offer the best approach to managing these risks, as detailed below.

Recommendation: Decrease the income thresholds and increase payments for children

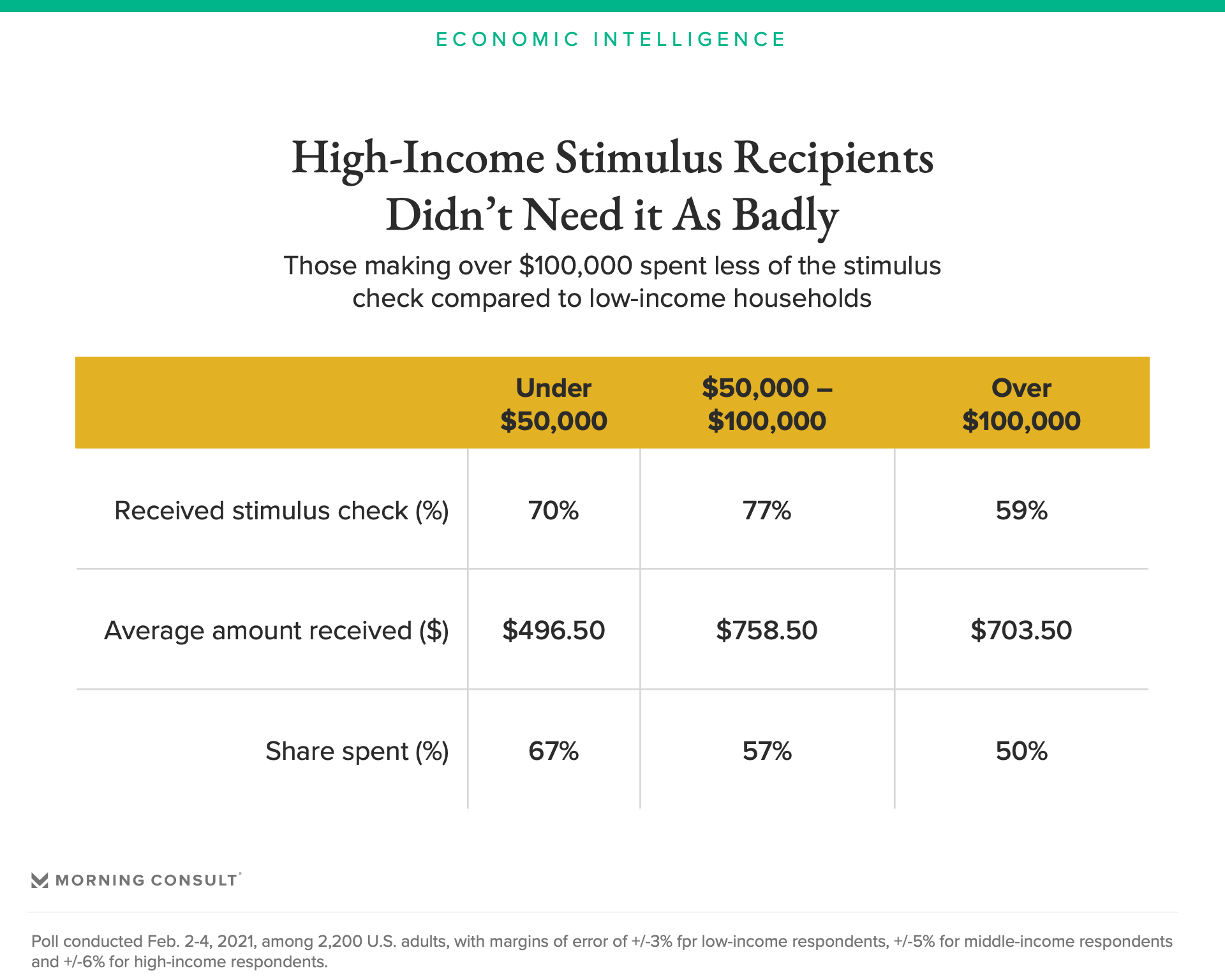

Low-income households and parents were the most desperate to receive their second stimulus checks and are the most likely to need additional stimulus going forward. According to a survey conducted at the beginning of February, Americans with annual household incomes under $50,000 already spent roughly 67 percent of money they received.

Stimulus checks provided to households earning over $100,000 per year and under $174,000 per year were less needed even though two or more people lived in those households. This shows that the income cutoffs for heads of households and jointly filing adults used in the second coronavirus relief package were too high.

Redirecting the money sent to higher-income households to lower-income households or small business assistance would drive consumer spending higher and reduce more financial hardship. For example, if Congress were to drop the upper threshold to $100,000, 20 million Americans would still be able pay their bills through July, a decrease of 2.6 million adults. The money that the government saves from lowering the upper income threshold for heads of households and married couples could be redirected to parents with children or other financially vulnerable groups.

Data on parents also shows how hard the pandemic is hitting them. Single parents spent 70 percent on average of the money they received from the second stimulus check, while two-partner parents spent 65 percent of their checks, compared to 60 percent among non-parents. The third round of stimulus should increase the additional money that eligible parents receive per child.

Recommendation: Extend federal unemployment benefits through September and implement automatic stabilizers to avoid future disruptions in benefits

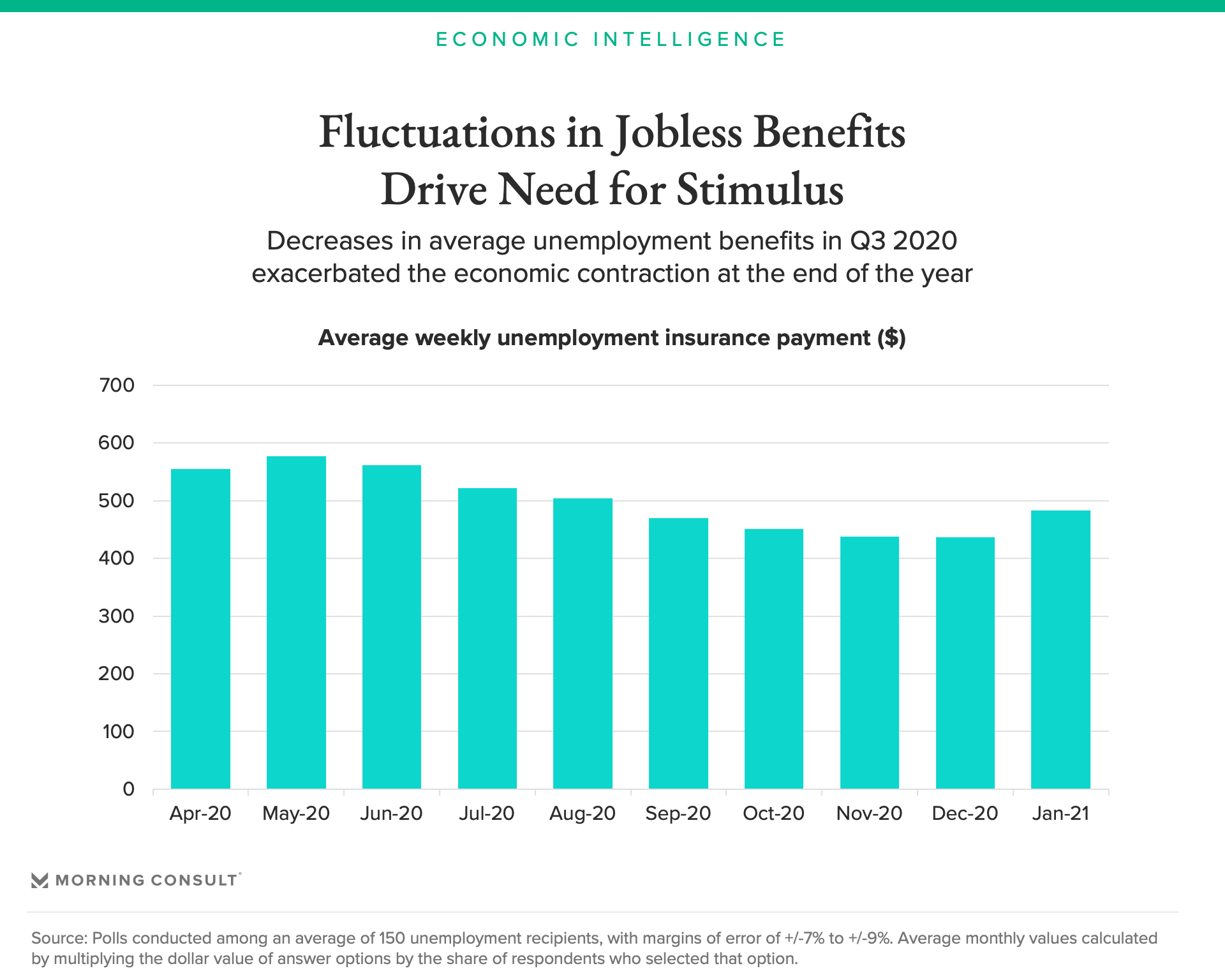

The second coronavirus relief package included a $300-per-week federal unemployment “boost” for those receiving benefits. Due to limitations in states’ processing systems, roughly 1 in 3 unemployment insurance recipients have yet to receive the federal boost, according to Morning Consult’s survey.

Congress should extend the unemployment insurance provisions included in the second coronavirus relief package through the end of September and adopt automatic stabilizers as a risk mitigation strategy against ineffective vaccinations and long-term labor market scarring. Congress exacerbated the economic downturn in November and December by adopting a “wait and see” approach to extending expanded unemployment insurance benefits. There is no justifiable reason to have to learn this lesson a second time.

John Leer leads Morning Consult’s global economic research, overseeing the company’s economic data collection, validation and analysis. He is an authority on the effects of consumer preferences, expectations and experiences on purchasing patterns, prices and employment.

John continues to advance scholarship in the field of economics, recently partnering with researchers at the Federal Reserve Bank of Cleveland to design a new approach to measuring consumers’ inflation expectations.

This novel approach, now known as the Indirect Consumer Inflation Expectations measure, leverages Morning Consult’s high-frequency survey data to capture unique insights into consumers’ expectations for future inflation.

Prior to Morning Consult, John worked for Promontory Financial Group, offering strategic solutions to financial services firms on matters including credit risk modeling and management, corporate governance, and compliance risk management.

He earned a bachelor’s degree in economics and philosophy with honors from Georgetown University and a master’s degree in economics and management studies (MEMS) from Humboldt University in Berlin.

His analysis has been cited in The New York Times, The Wall Street Journal, Reuters, The Washington Post, The Economist and more.

Follow him on Twitter @JohnCLeer. For speaking opportunities and booking requests, please email [email protected]