Key Takeaways

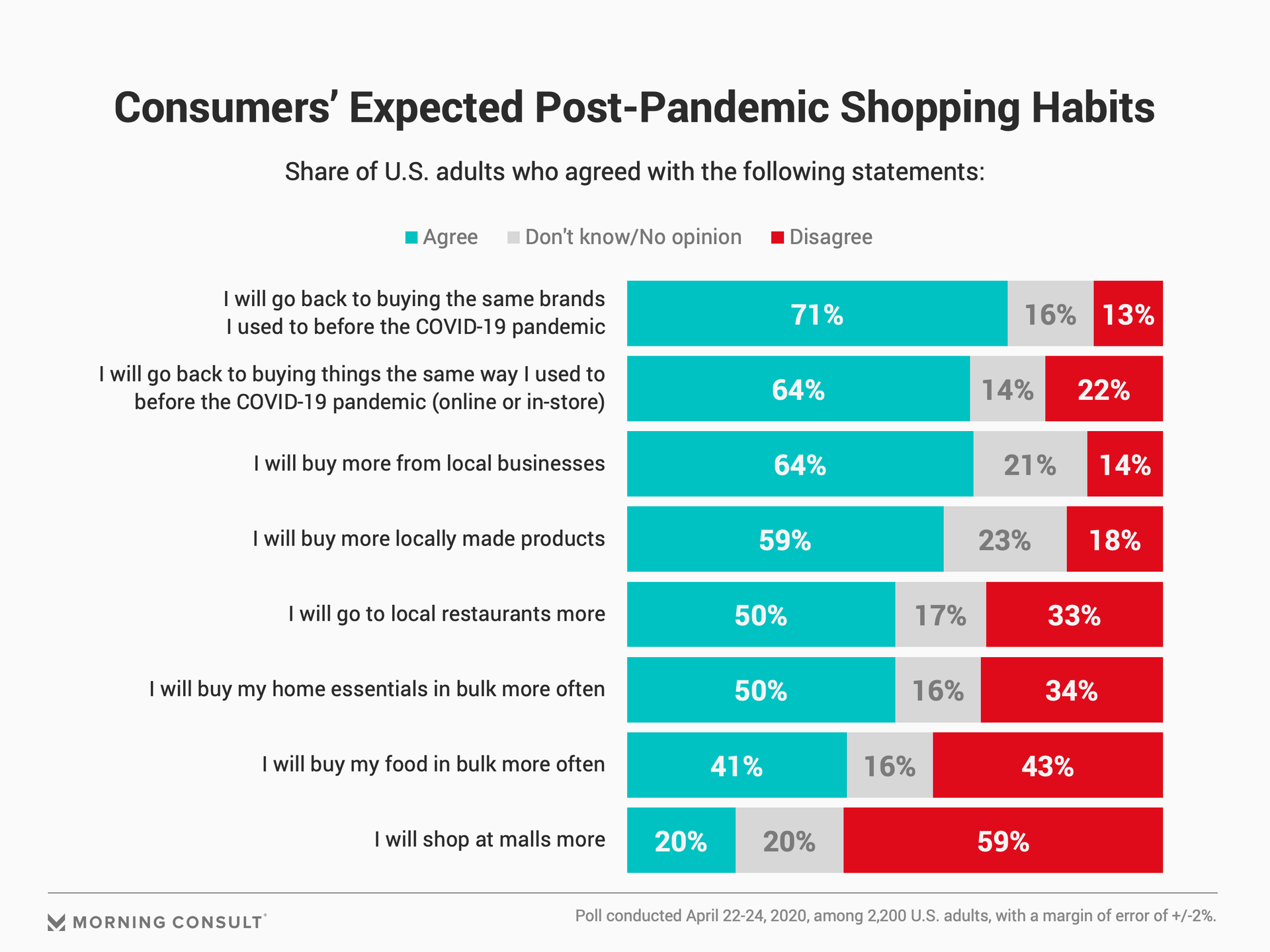

71% of Americans expect to return to buying the same brands they did pre-pandemic, and 64% will revert to the same purchasing channels they used before the outbreak.

But local businesses have reason for optimism: 64% of U.S. adults will buy more from local businesses, 59% will buy more locally made products, and 50% will frequent local restaurants more.

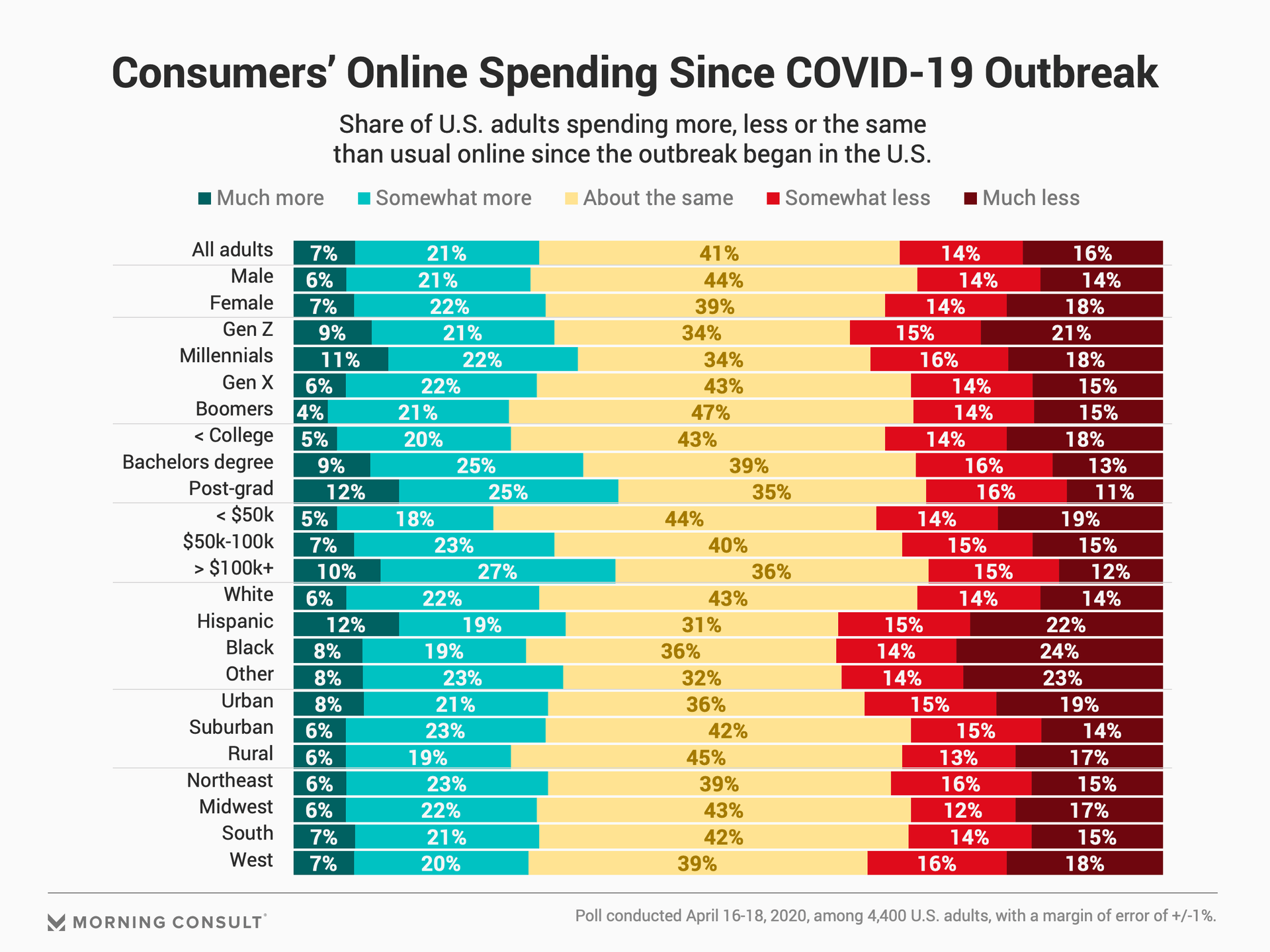

28% of U.S. adults are now spending more online, including as much as 37% of high-income and highly educated groups, and the trend may continue with only 20% of people expecting to shop at malls more post-pandemic.

Morning Consult’s “Favorited or Forgotten” series explores if – and how – consumer behavior will change in a post-COVID-19 world and what business leaders can do to prepare for those changes. Sign up here to receive the latest in your inbox each week.

This analysis was authored by Morning Consult analyst Victoria Sakal.

The challenges presented by the coronavirus outbreak are far and wide, with implications for consumers manifesting in massive drops in consumer confidence, perceivable changes in consumption patterns, and endless frustration around getting products they want and need, when and where they prefer to. Given this environment -- and driven in part by health concerns, social distancing mandates and shelter-in-place measures -- online purchasing and e-commerce as a whole are having something of a moment in the spotlight as shoppers embrace this channel as a safer, more convenient alternative to bricks and mortar. But will this outbreak mean the demise of offline shopping’s popularity once and for all?

Even with decreases in overall spending given employment and economic strains, most Americans are spending about the same on online purchases during the pandemic. Still, 28 percent are spending more online, including as much as 37 percent of high-income and highly educated consumers.

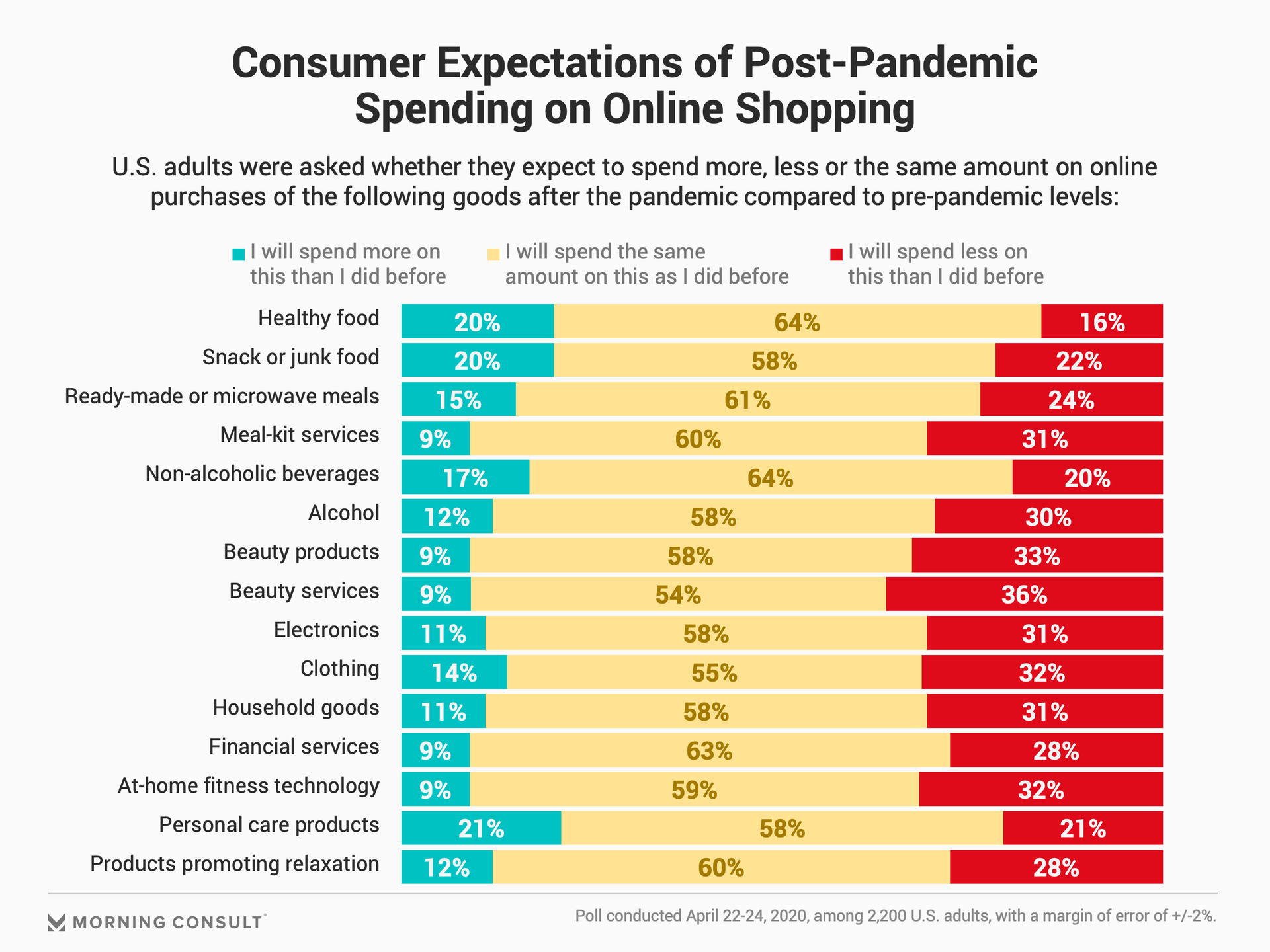

Research conducted in mid-April found that most adults planned to spend about as much post-pandemic on online purchases across most categories, though roughly a third or more of Americans planned to spend less online buying meal-kit services (37 percent), at-home fitness technologies (35 percent), relaxation-related products (34 percent), beauty services (33 percent), alcohol (33 percent) and beauty products (32 percent).

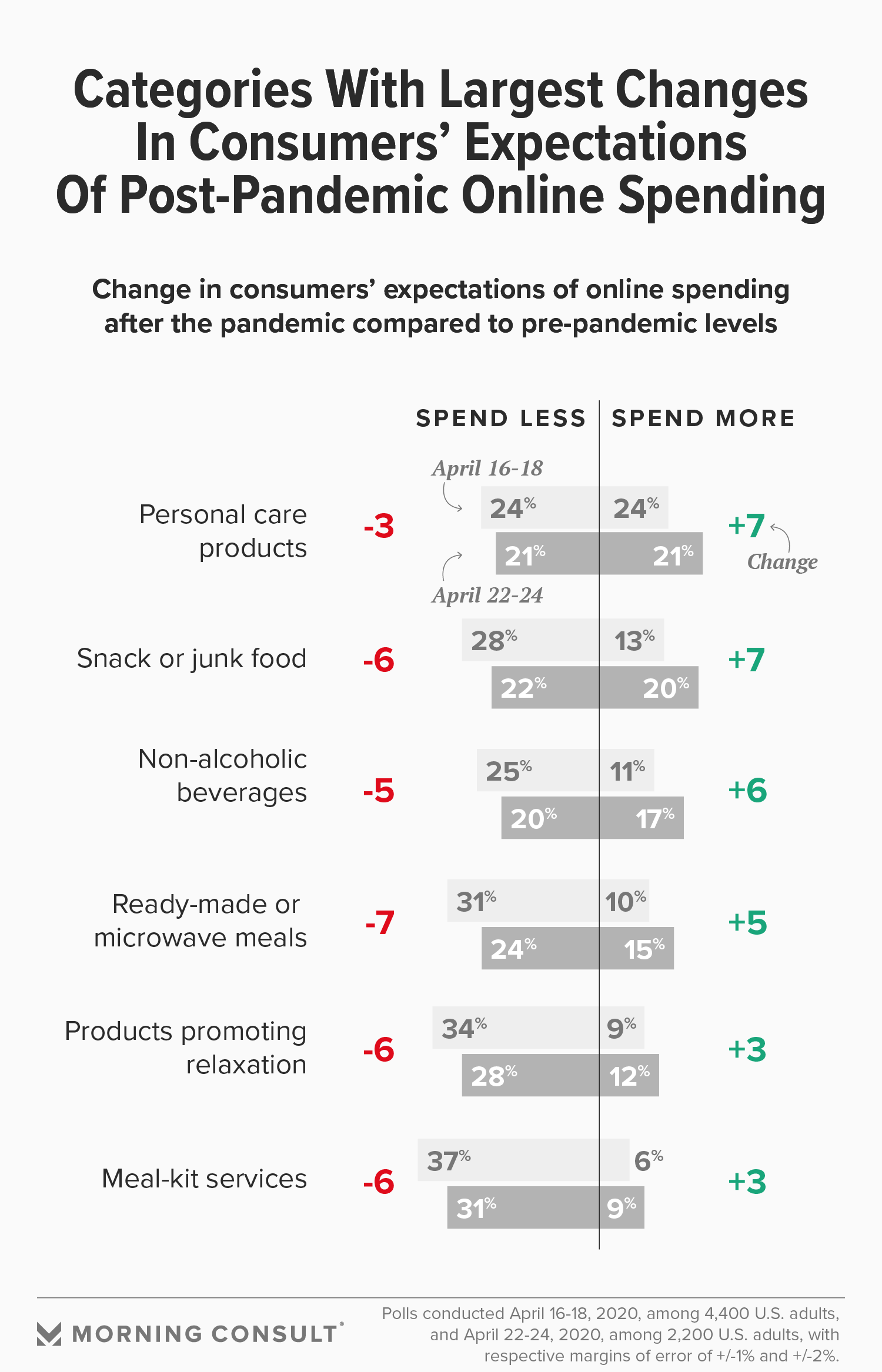

However, it seems that adults are warming to the idea of spending at least as much as, if not more than, they were pre-pandemic on online orders of relaxation-related products and meal-kit services; the portion of Americans expecting to buy these less post-pandemic has dropped to 28 percent and 24 percent, respectively. While this is a trend to continue watching, companies in these spaces may be making inroads in forging lasting connections with their audiences, but they should still be making every effort to deliver experiences that surprise and delight their online customers to ensure that post-pandemic spend levels don't wane.

Beyond these, expected post-pandemic purchasing levels of a few other categories have also seen notable changes since Morning Consult first began tracking this mid-April. Early expected increases in online spending on healthy food, clothing, personal care items and snack and junk food have amplified: In a matter of a week, post-pandemic purchase expectations of these categories trended upward significantly. Our late-April data shows a 7 percent point increase in Americans planning to spend more on online purchases of personal care items and snack and junk food once the crisis is over. Expected post-pandemic online purchase levels of non-alcoholic beverages, ready-made meals and alcohol have increased as well.

Brands in many of these categories can celebrate that more consumers now seem to be coming around to buying more of these products post-pandemic versus less, but only time will tell how this trend unfolds. Regardless, any online-only companies active in those categories clearly face an uphill battle against inertia as across all categories, a clear majority of consumers expect to snap back to pre-pandemic purchasing levels.

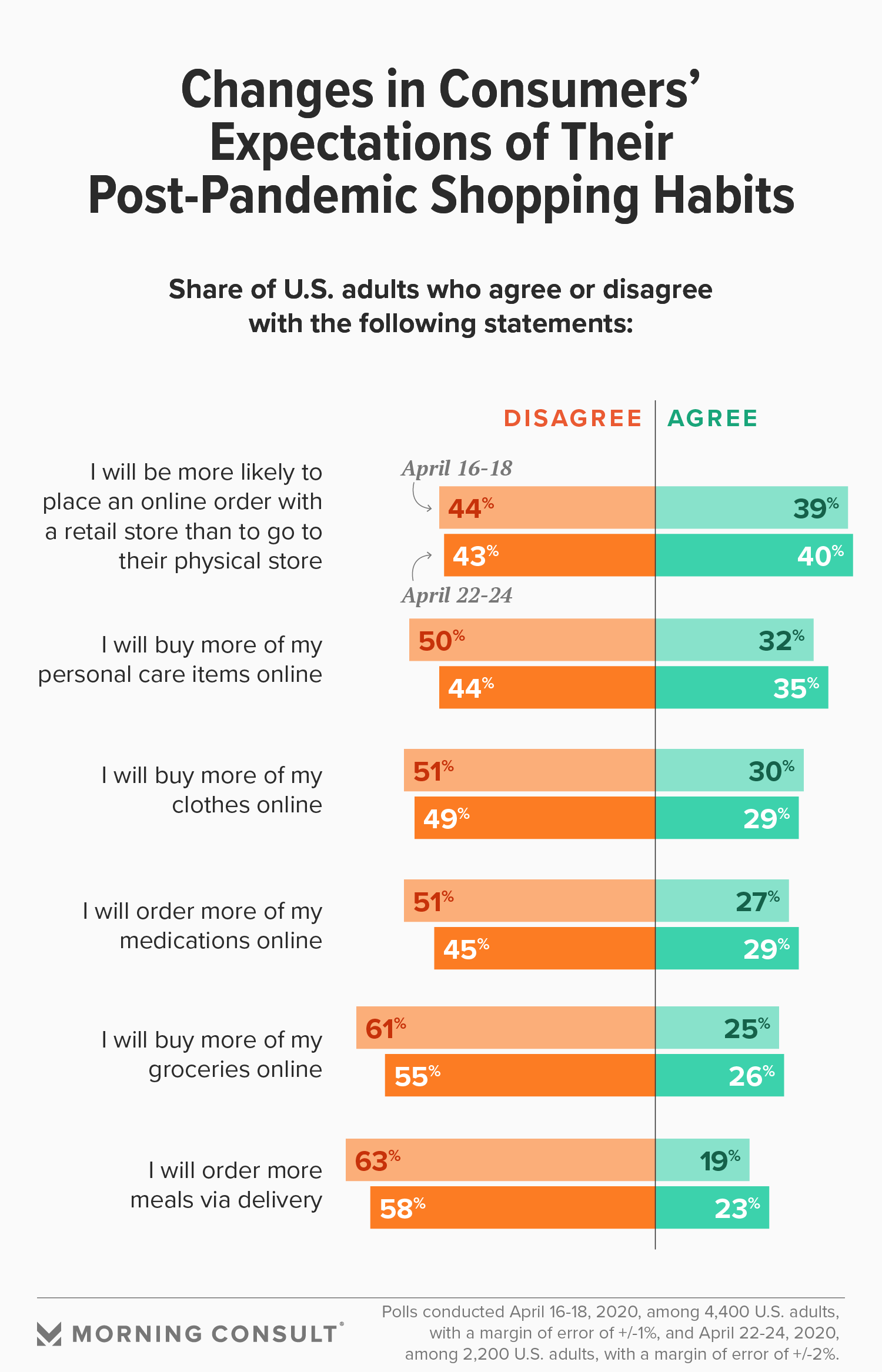

Additionally, even if a majority of adults don’t plan to buy items ranging from personal care and clothes to medications and meal delivery online, they seem to be warming to the idea of doing so. In all cases, the portion of adults disagreeing with the prospect of buying certain product categories online more post-pandemic has declined over time -- by as much as 6 points in the case of online groceries.

Further, companies active in these e-commerce categories should not interpret this as a sure bet that demand for the online channel guarantees demand for their brand. Until the majority shifts to embracing online purchasing, it’s important to remember that while good experiences will increase the likelihood that consumers “favorite” a brand and buy again, bad experiences may very well cause permanent “forgetting.” This has implications not only for individual brands but also for the e-commerce industry as a whole.

Finally, considering shopping habits more broadly, it appears that unless brands can find a way to strategically insert themselves into consumers’ lives and minds through a compelling product, service and offer of value, inertia and muscle memory will win. Seventy-one percent of Americans plan to return to their tried-and-true brands post-pandemic; 64 percent will return to their go-to purchase methods, whether online or in person. Though there’s hope for local businesses, as 50 percent or more plan to support local restaurants, products and businesses more post-pandemic, and while we may see a change in the volume purchased per shopping trip as consumers begin to buy more in bulk, it’s clear that what and how consumers buy is sticky.

Compounded by a challenging purchasing environment and an otherwise complex and confusing time, brands will have to work even harder to cut through and forge new relationships as shoppers rush back to the products, services and stores they miss.

DTC deep dive

As consumers become increasingly comfortable with the nature and convenience of buying online, it’s clear that e-commerce is on the rise, but it’s worth considering how this trend will translate to direct-to-consumer, a category whose brands were founded on the very premise that online-only was the way of the future.

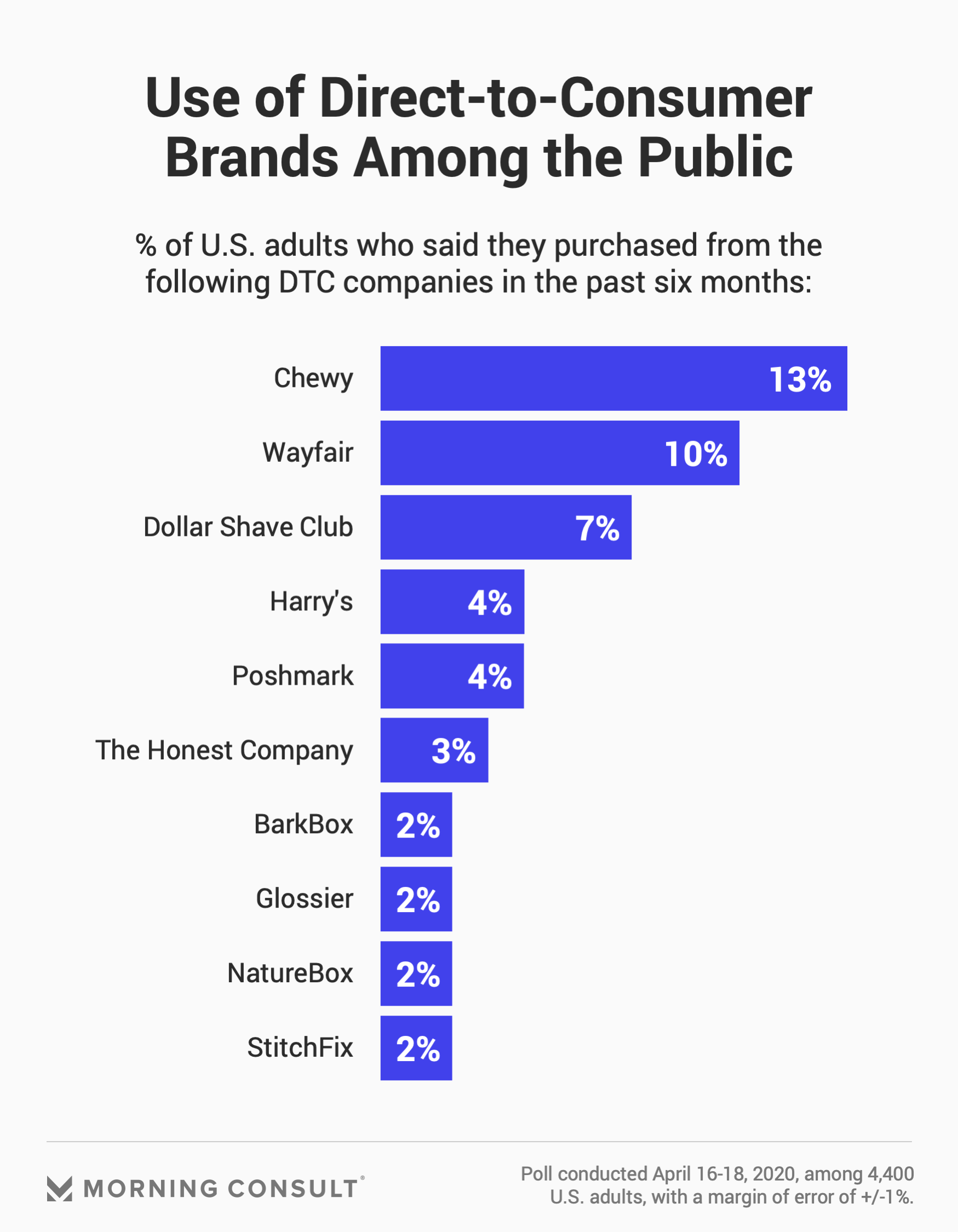

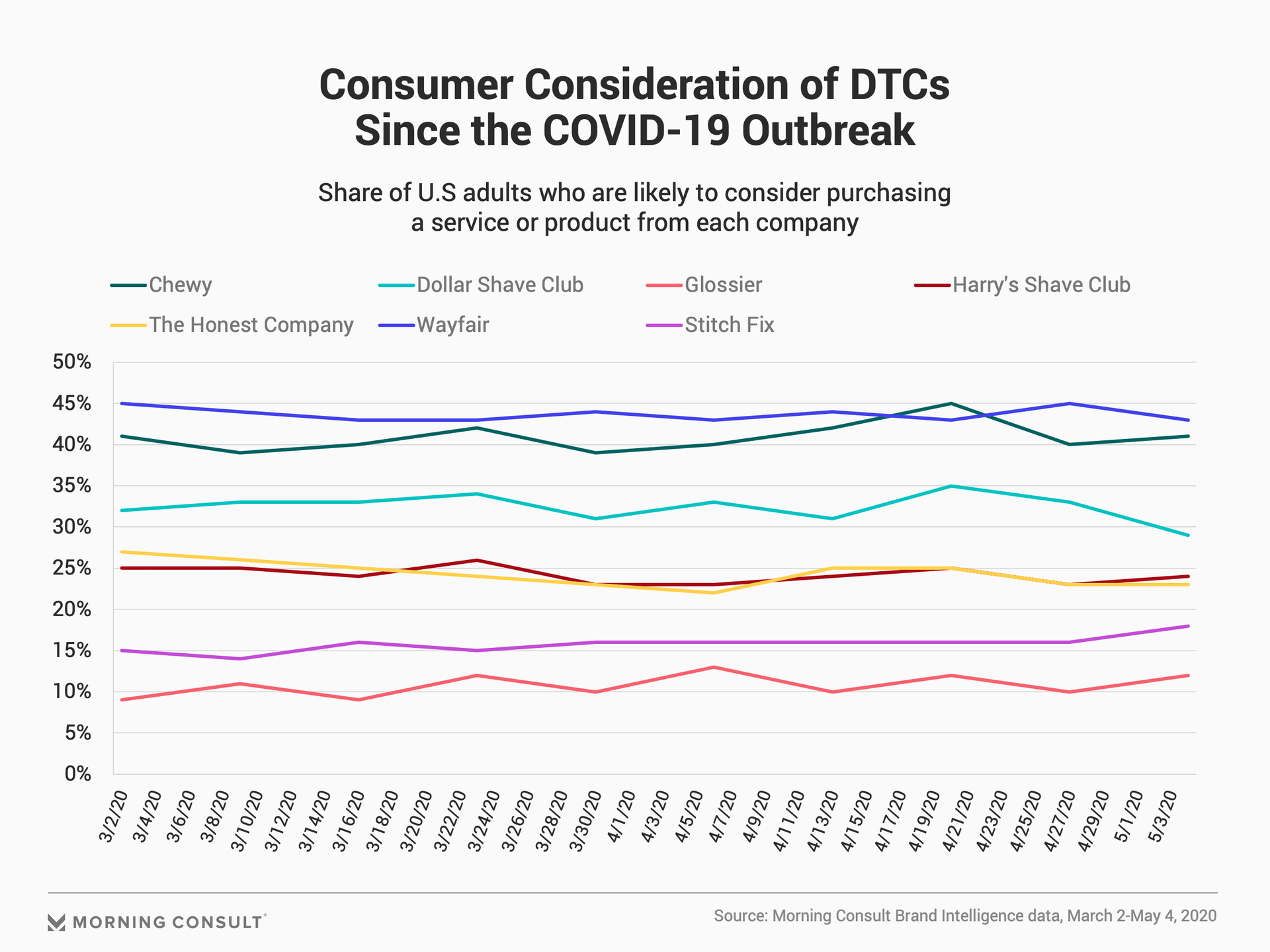

Only a small share of the 4,400 American adults surveyed have purchased from a direct-to-consumer brand in the last six months, with Chewy Inc., Wayfair Inc. and Dollar Shave Club being the most common.

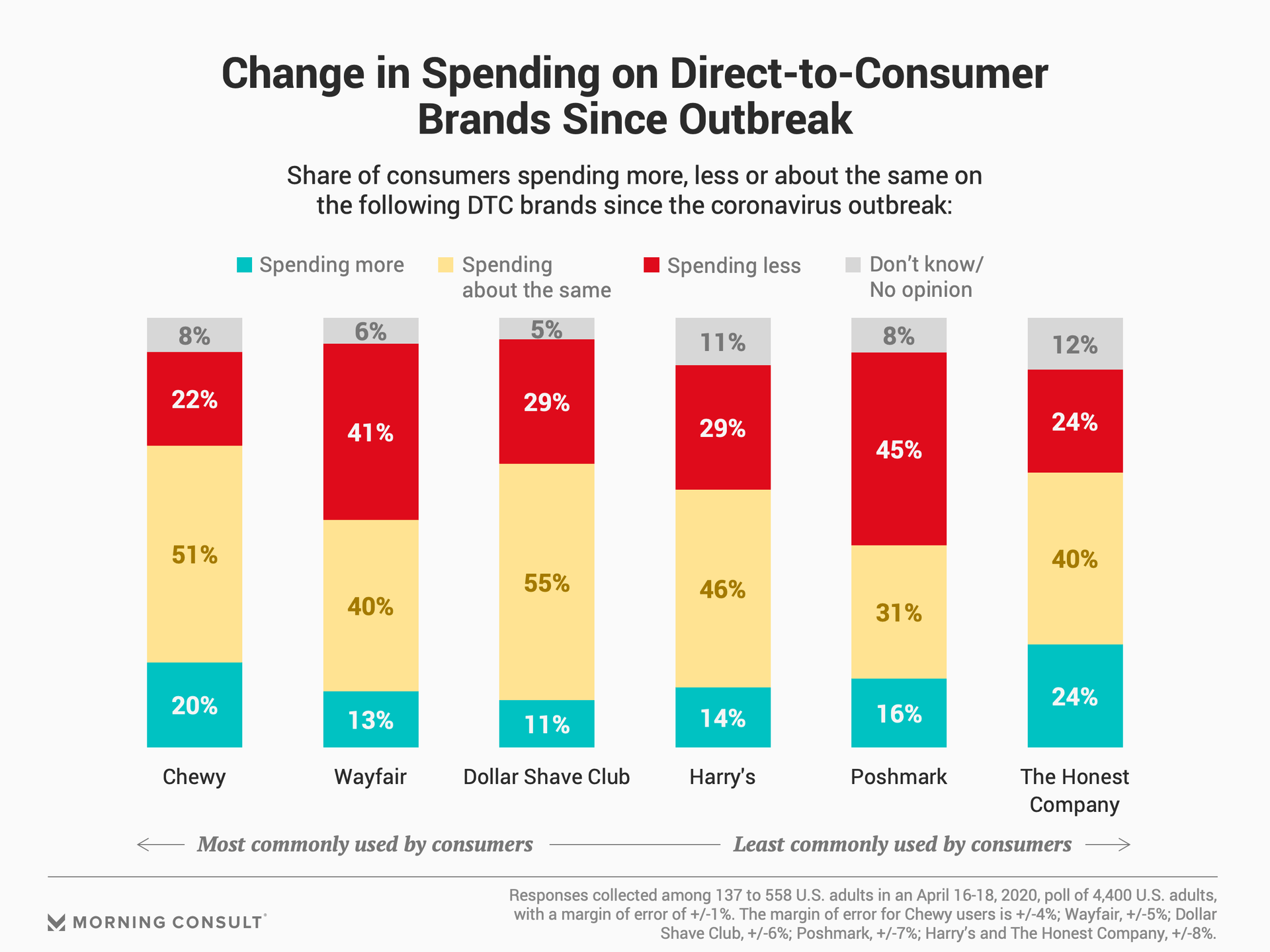

Among the top DTCs Americans buy from, most are spending about as much with these companies as they were pre-pandemic. Users of Poshmark and Wayfair, however, indicate that they’re spending less on these brands since the COVID-19 outbreak. Considering significant purchasing reductions seen in the household goods and clothing categories, these declines are not surprising.

Given its secondhand marketplace model, Poshmark may be particularly less appealing to shoppers whose health concerns have escalated since the pandemic, leading them to overtly avoid strangers and transmission of germs, and who have therefore reduced their purchases from the company.

Wayfair, meanwhile, recently reported a significant sales spike that it attributed to an uptick in newly acquired customers (it added nearly 1 million customers in 2020 alone). But consumers reporting reduced spending at the home furnishing retailer since the outbreak suggests that although the size of Wayfair’s customer base has increased, the value of each of its customers may be on the decline. Retaining new customers will be just as critical as stemming the drop-off in spending across all customer types in the months ahead.

As for The Honest Company, the uptick in purchases since the outbreak may have something to do with the company’s mission to offer safe and natural goods.

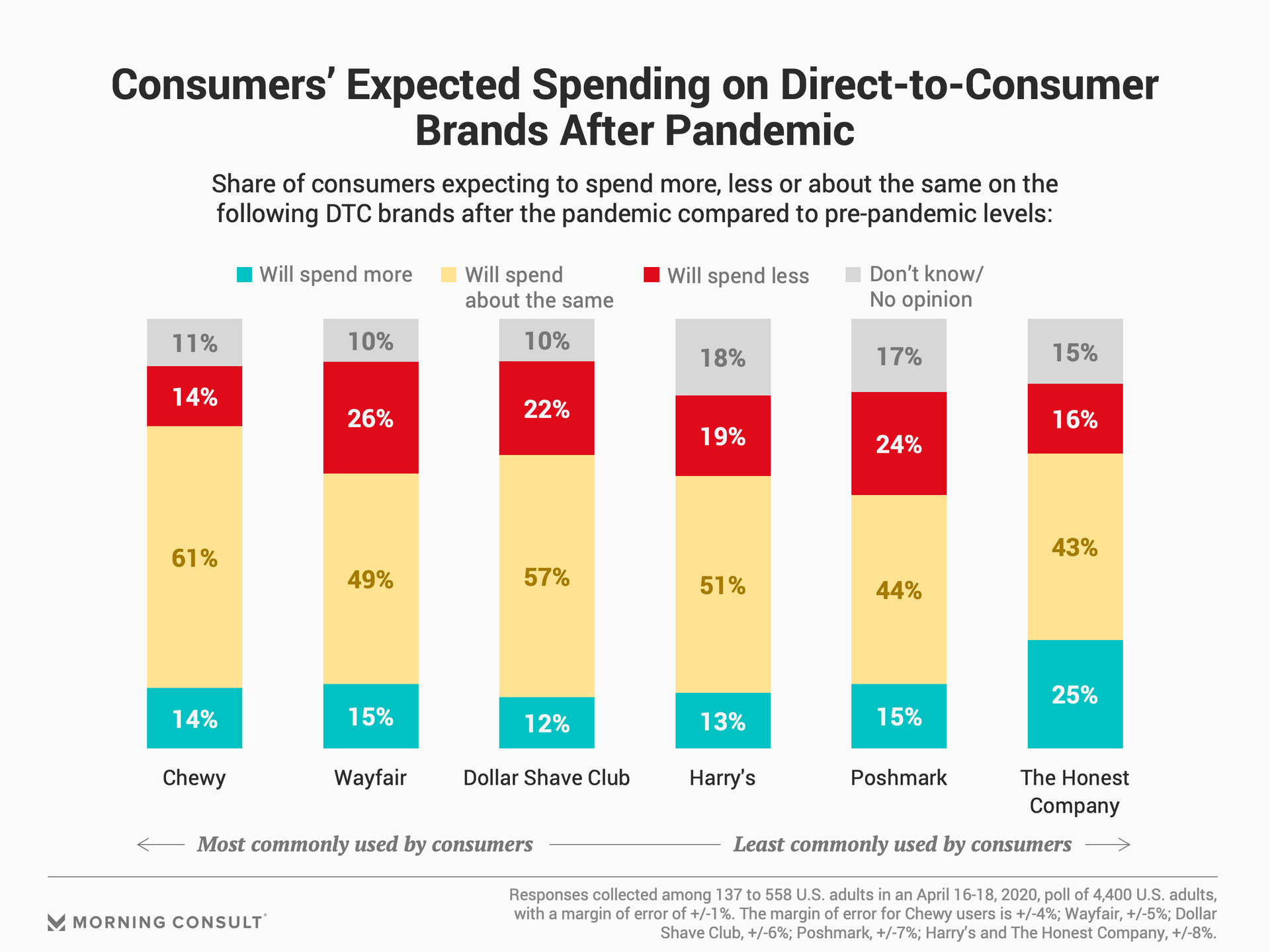

Post-pandemic spending levels on these DTCs largely reflect the trends seen in current spending levels. Though most adults expect to purchase about as much from each of these companies as they did pre-pandemic, about a quarter expect to spend less with Wayfair and with Poshmark; current purchase increases at The Honest Company may very well translate to some increases in post-pandemic purchasing activity, though it’s incumbent on each of these companies to focus on delivering positive experiences, high-value products and ongoing relevance in order to sustain any momentum with increased spenders post-pandemic.

Given this, it’s critical for DTC brands to focus on maintaining their existing customer bases at this time to ensure that consumers’ expectations of returning to pre-pandemic spending levels translate to reality, especially given the unpredictable and likely strained new normal they’ll be returning to. The calculus around customer acquisition costs on the online and social channels characteristically used by these companies may be improving as marketing costs drop during the pandemic, but it’s important for brands to bear in mind the low awareness levels, challenging economic circumstances and relevance of their products for meeting unique consumer needs during this very unique time.

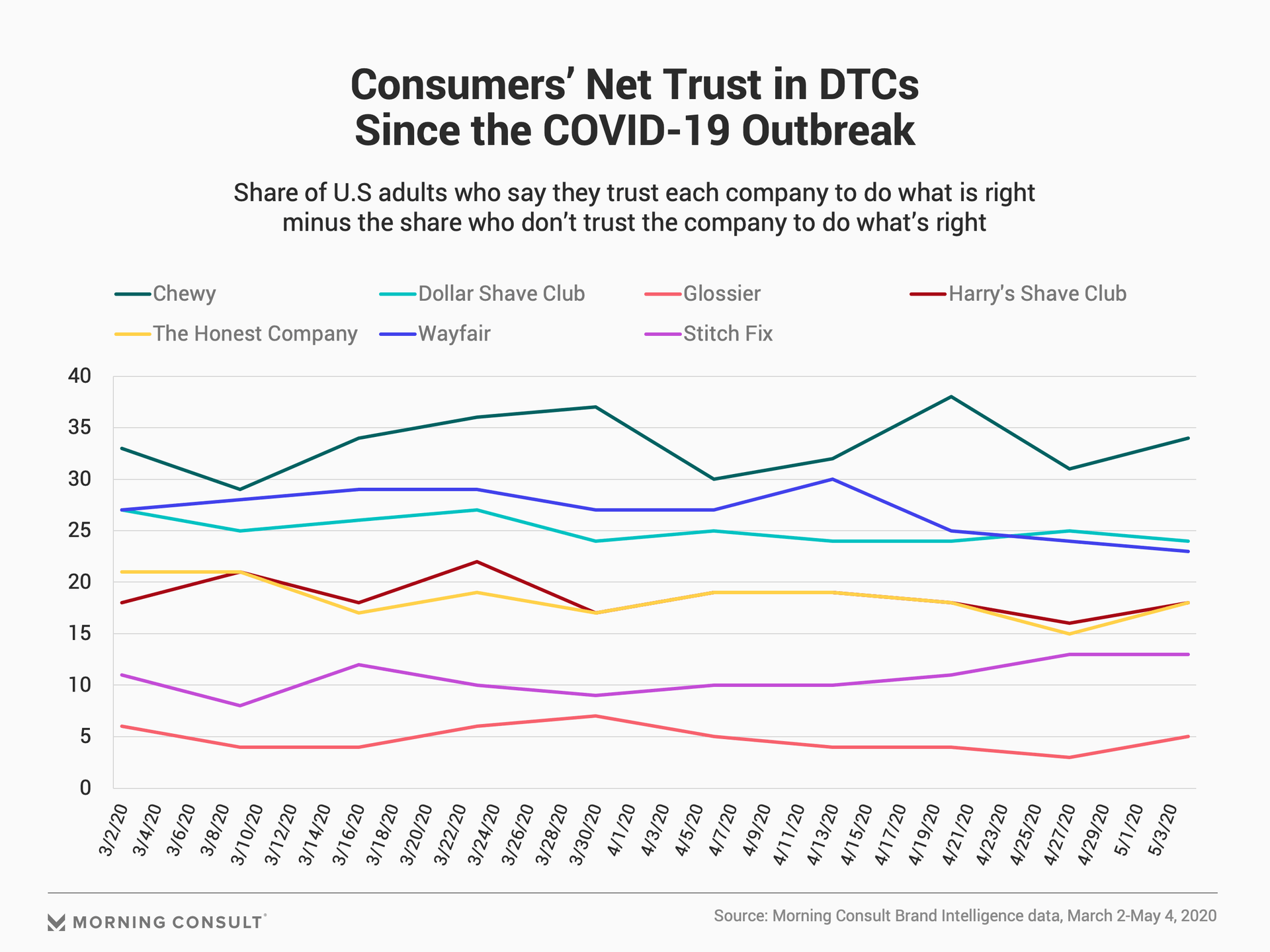

Morning Consult’s Brand Intelligence data echoes this, showing that Chewy and Wayfair usage and consideration have remained strongest; Dollar Shave Club and The Honest Company -- though each seeing their own change in fortune since late April -- are a bit less popular but seem to be hanging onto a decent portion of active customers.

Victoria Sakal previously worked at Morning Consult as a brands analyst.