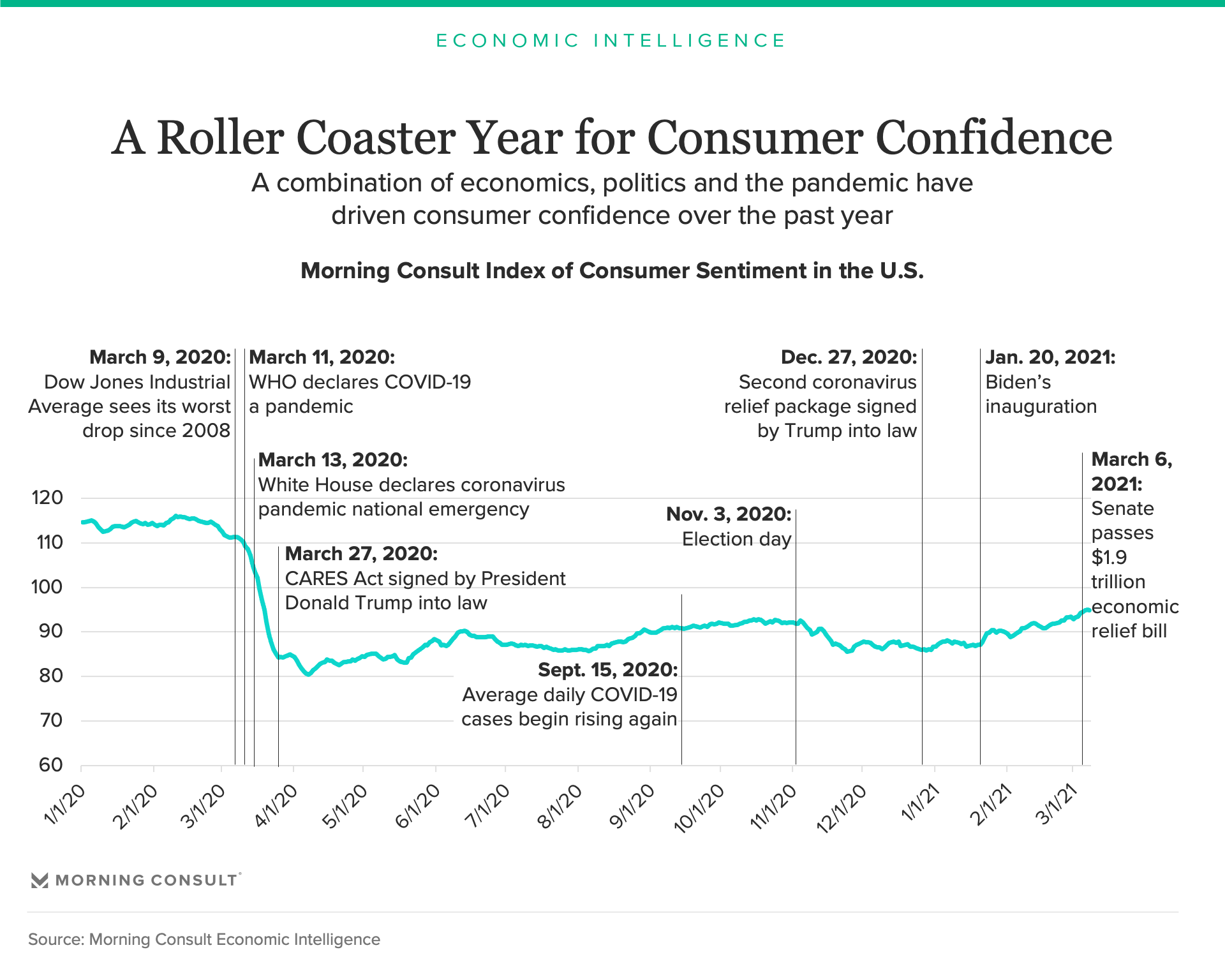

The Five Phases of Consumer Confidence During the First Year of the Pandemic

Consumer confidence in the United States has been on a roller coaster over the past year of the pandemic, driven by a combination of factors related to economics, politics and the virus. The importance of these factors varied over the past 12 months, falling into five distinct phases:

- February-March 2020: Uncertainty during initial outbreak

- April-August 2020: CARES Act mitigates pandemic's economic fallout

- September-October 2020: New cases and waning financial support stop the recovery in its tracks

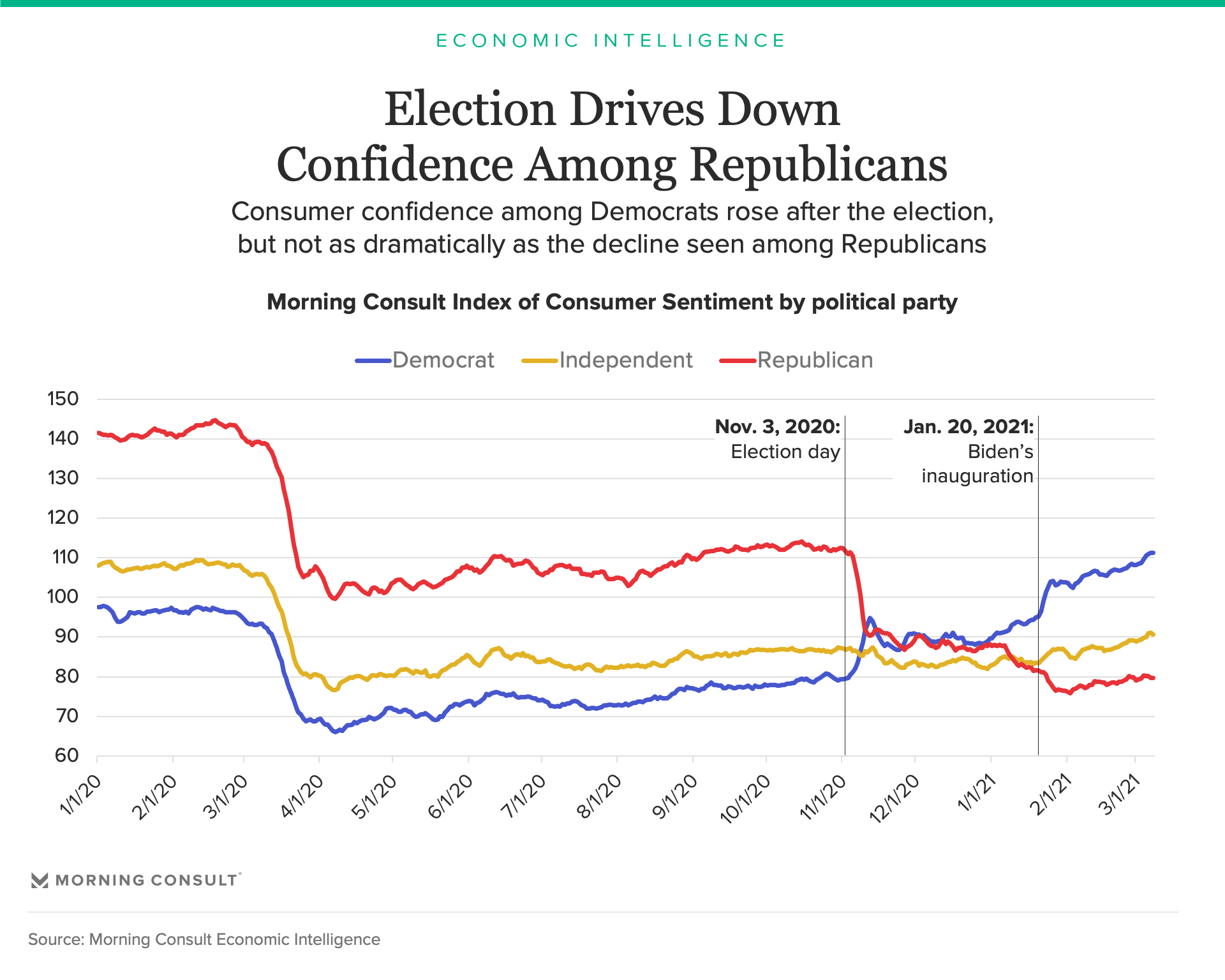

- November-December 2020: Election, pandemic drive volatility in confidence

- January-March 2021: Financial support eases concerns

This analysis measures these events’ disparate impact across key demographics, including generation, income, education and political party, identifying which consumers are faring better than others in the year since the World Health Organization declared the coronavirus outbreak a global pandemic.

Uncertainty during initial outbreak

In late February and early March, it was nearly impossible to forecast the impact of the pandemic on the economy. Initial unemployment claims did not increase until later in March, and stock prices began increasing even before the effect of the pandemic on the broader economy could be measured.

Consumers initially considered the pandemic a problem for the U.S. macroeconomy as a whole, but not for their own personal finances. However, by March 10, consumers updated their assessment, acknowledging that the pandemic would likely harm their future finances.

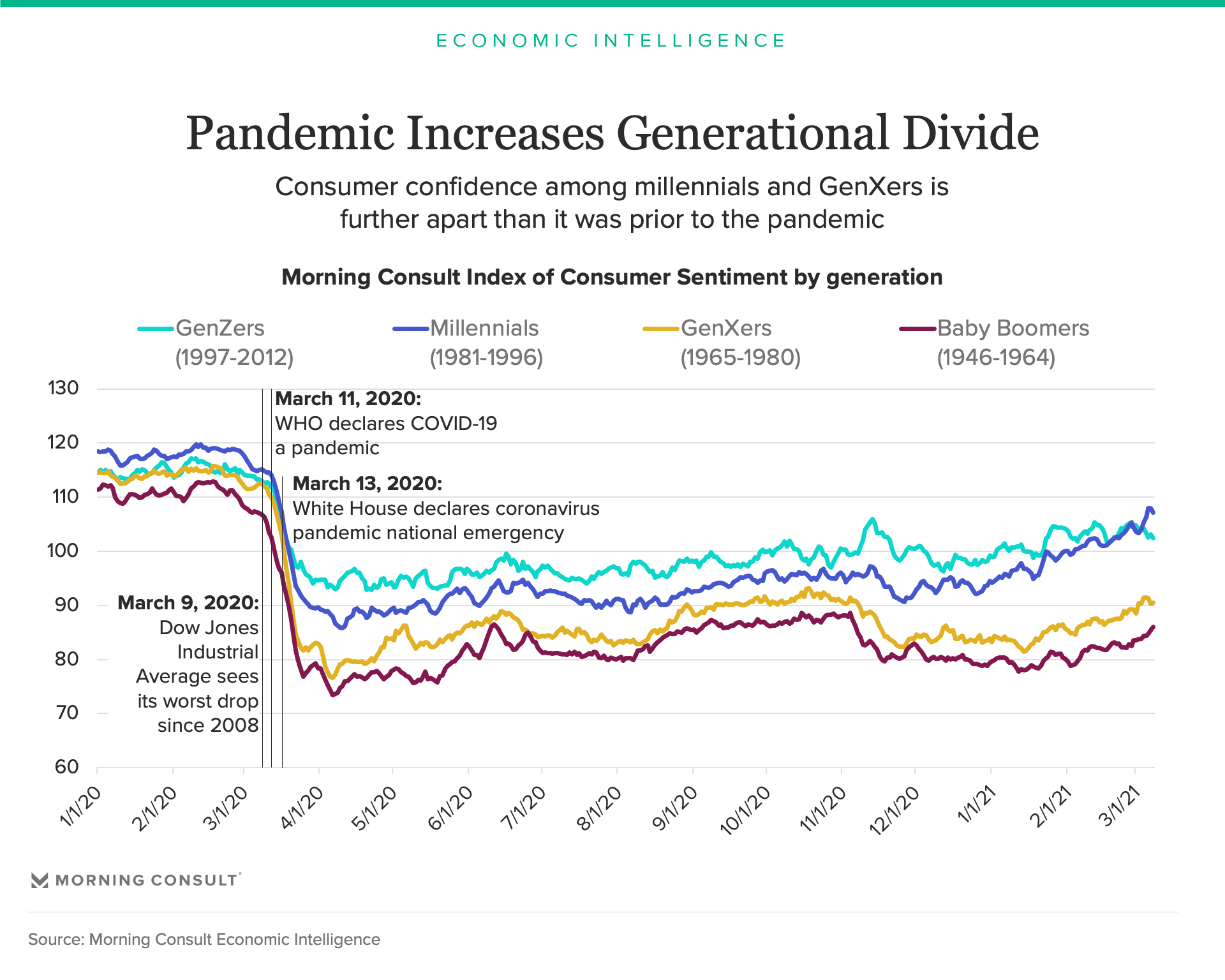

As seen in the graph below, consumer confidence among all generations fell dramatically in early March before the WHO or White House formally acknowledged the economic and health risks facing the country. However, what Americans acknowledged relatively quickly is that the pandemic posed a greater economic and health risk to Baby Boomers than it did to GenZers or Millennials. Not only were Baby Boomers more physically vulnerable to the virus, they also had less time to make up the financial losses incurred during the pandemic. Twelve months into the pandemic, the generational divide in consumer confidence has grown even larger.

CARES Act mitigates pandemic’s economic fallout

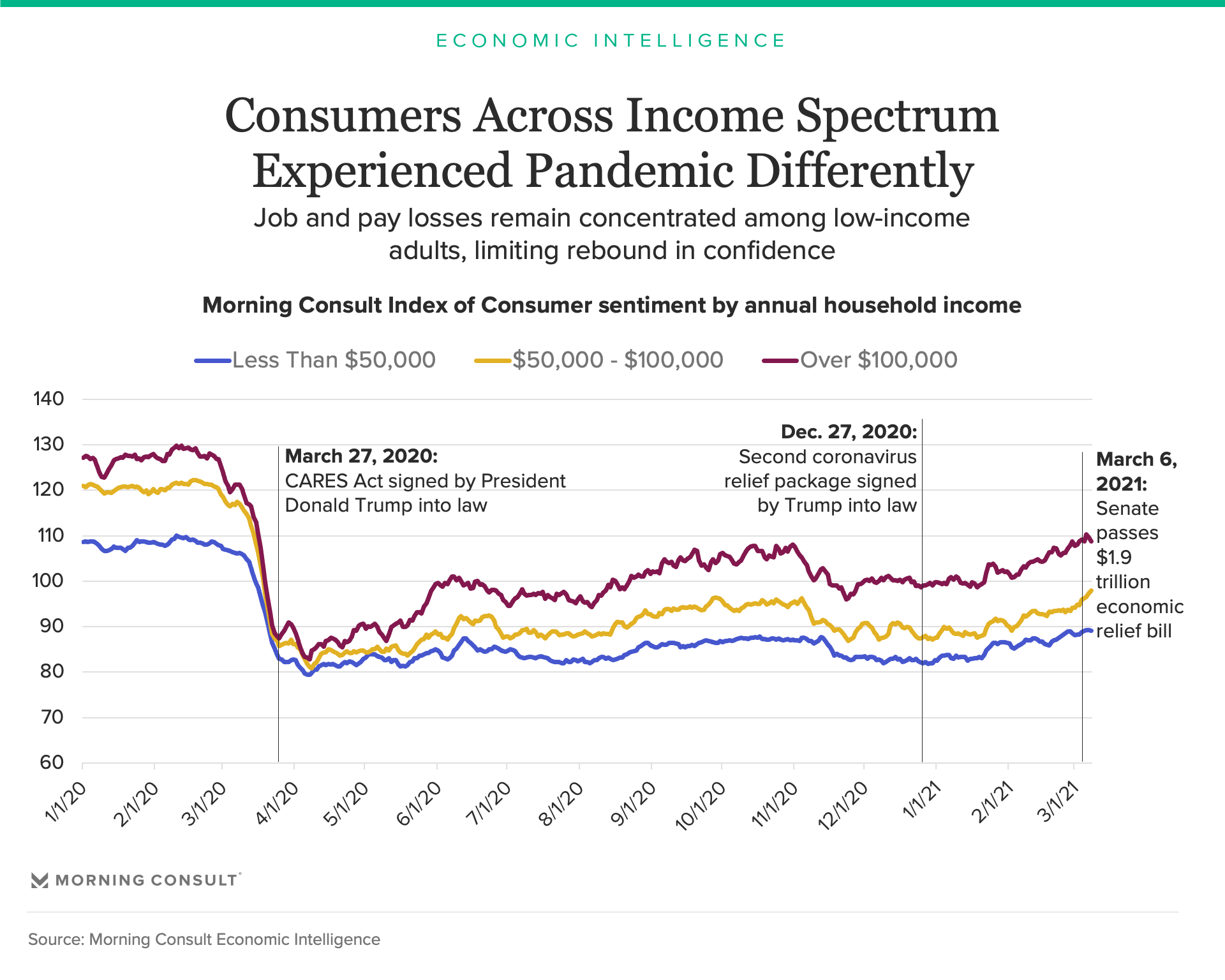

Passage and the signing of the CARES Act on Mar. 27, 2020, limited additional decreases in consumer confidence and set the foundation for the economic recovery over the summer. However, the federal government struggled to disburse stimulus checks in a timely manner, particularly to low-income Americans, and shortcomings in states’ unemployment systems delayed federal unemployment insurance payments. Only once financial support began hitting consumers’ bank accounts did consumer confidence begin to consistently increase.

Additionally, low-income Americans continued to suffer pay and income losses at higher rates than the rest of Americans. As shown in the chart below, confidence among low-income consumers has been the slowest to rebound.

New cases and waning financial support stop the recovery in its tracks

By the end of the summer, the economy was facing the perfect storm: Direct financial assistance to consumers via stimulus checks and federal unemployment benefits was winding down, and new cases began increasing.

Political pressure to reopen the economy also mounted during this time, with the idea that the benefits from increased economic activity would outweigh costs in terms of lost lives and sicknesses. However, based on the strong negative correlation between daily consumer confidence and the spread of the virus, I concluded at the time that “[r]eopening the economy in an environment of depressed consumer confidence is unlikely to generate adequate economic activity to justify the health risks.”

Unfortunately, as average new cases began increasing again in mid-September, the recovery in confidence lost momentum. In short, rather than balancing the need to support the economy while controlling the virus, the United States sacrificed both.

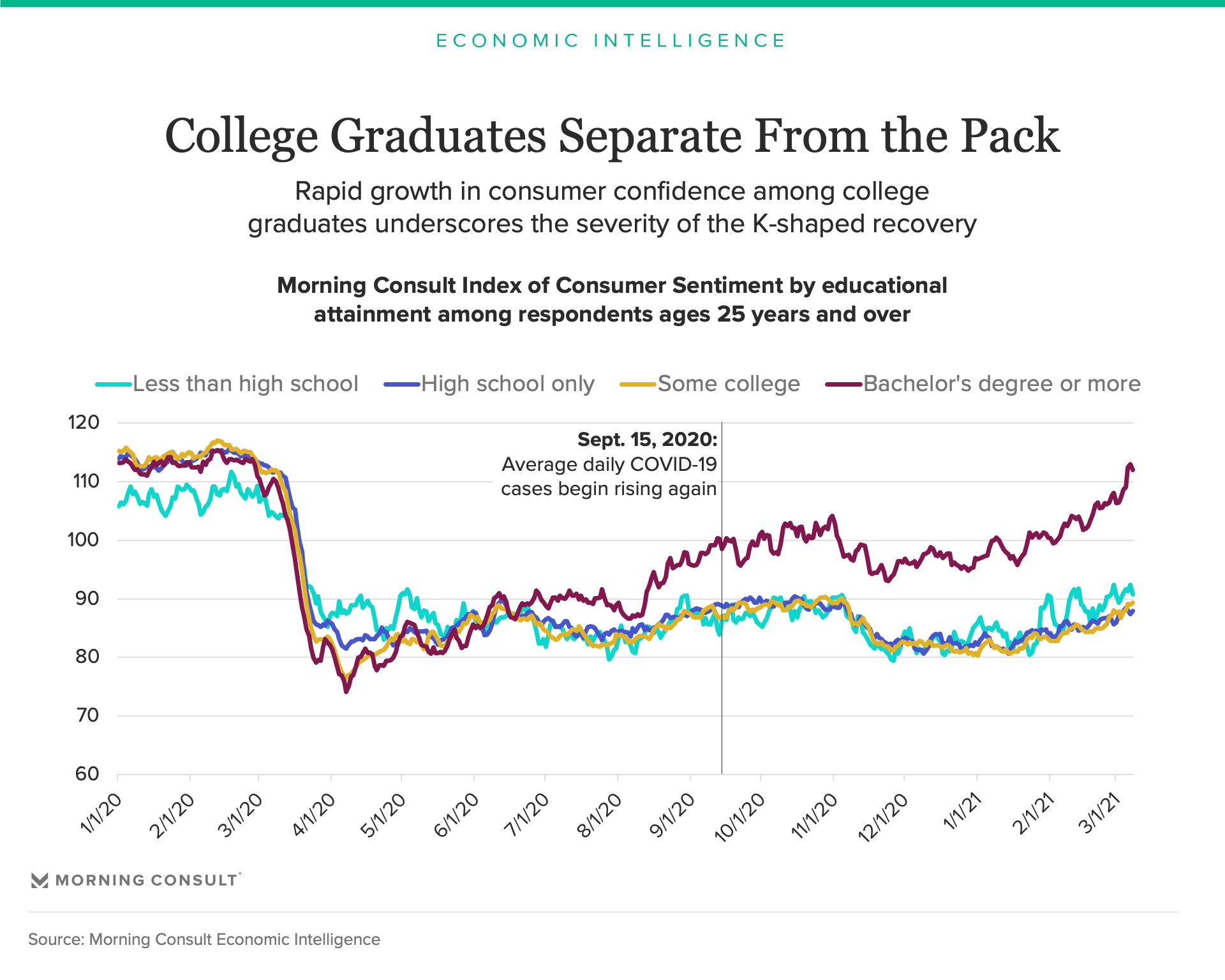

As most Americans lost confidence in the economy, higher-educated Americans began to distance themselves from the rest, underscoring the K-shaped nature of the recovery. Not only were they more likely to maintain their jobs, they also remained more secure in the jobs they had, as evidenced by the growing educational gap in confidence over the summer.

Election, pandemic drive volatility in confidence

During the lead-up to the election, consumers were hesitant to dramatically alter their assessment of the economy. However, following the election, confidence among Republicans dramatically fell, while confidence among Democrats increased.

Daily consumer confidence exhibited elevated volatility following the election due to the mixed messages in the fight against the virus. While new daily cases were rapidly increasing, Pfizer and BioNTech announced that their vaccine was found to be more than 90 percent effective in preventing COVID-19. Given the significant logistical obstacles to producing and distributing the vaccine, consumers were hesitant to dramatically alter their economic assessments as the pandemic continued spreading at an accelerating rate.

Financial support eases concerns

The second coronavirus relief package, signed by President Donald Trump on Dec. 27, 2020, effectively ended the ambiguity facing consumers. While new cases were still increasing, most Americans would receive additional financial support via $600 stimulus checks and weekly federal unemployment insurance payments. While states were still slow in distributing the additional unemployment insurance money, the federal government distributed stimulus checks much faster the second time around, driving consumer confidence and spending higher in January and February.

Looking ahead

The trajectory of the recovery in consumer confidence is likely to continue to be a function of the economic, political and public health developments. More financial support appears to be on the way, with the House of Representatives preparing to vote on the $1.9 trillion relief bill approved by the Senate last weekend. The accelerating rate of vaccinations should also support continued increases in optimism among consumers.

Despite these improving conditions, U.S. consumers are likely to continue facing economic headwinds. In April of last year, I wrote “The timing of the rebound in confidence depends on the extent to which the ongoing economic shutdown spills over into other areas of the economy, including labor markets and credit conditions.” That assessment remains true with eleven months of hindsight. Employment conditions are likely to remain weak for the foreseeable future, particularly for low-income Americans, and deferred liabilities such as mortgage forbearances and unpaid taxes on unemployment insurance jeopardize Americans’ repayment capacity.

John Leer leads Morning Consult’s global economic research, overseeing the company’s economic data collection, validation and analysis. He is an authority on the effects of consumer preferences, expectations and experiences on purchasing patterns, prices and employment.

John continues to advance scholarship in the field of economics, recently partnering with researchers at the Federal Reserve Bank of Cleveland to design a new approach to measuring consumers’ inflation expectations.

This novel approach, now known as the Indirect Consumer Inflation Expectations measure, leverages Morning Consult’s high-frequency survey data to capture unique insights into consumers’ expectations for future inflation.

Prior to Morning Consult, John worked for Promontory Financial Group, offering strategic solutions to financial services firms on matters including credit risk modeling and management, corporate governance, and compliance risk management.

He earned a bachelor’s degree in economics and philosophy with honors from Georgetown University and a master’s degree in economics and management studies (MEMS) from Humboldt University in Berlin.

His analysis has been cited in The New York Times, The Wall Street Journal, Reuters, The Washington Post, The Economist and more.

Follow him on Twitter @JohnCLeer. For speaking opportunities and booking requests, please email [email protected]