Holiday 2024: What Retailers Can Expect This Shopping Season

Key Takeaways

High interest rates on credit cards are unlikely to drop substantially, helping to expand the audience for buy now, pay later loans.

While inflation has moderated, prices on major holiday categories haven’t fallen. Keeping prices competitive will be the key challenge for retailers at year-end.

Shopping enjoyment is on the upswing, particularly among high earners. Retailers should plan in-store shopping events early and often.

Data Downloads

Pro+ subscribers are able to download the datasets that underpin Morning Consult Pro's reports and analysis. Contact us to get access.

The 2024 winter holidays might feel far away: After all, we’ve got the summer Olympic Games, an entire U.S. presidential election cycle, and four more opportunities for the Fed to lower interest rates before then. A lot can and will change in that time. But, retailers know that holiday shopping is just around the corner.

The last few holiday seasons have no doubt been financially stressful for consumers. Still, the holidays are something to look forward to: A June 2024 survey saw that shoppers are more excited (68%) than anxious (55%) about the year-end holiday season. The cohort most likely to say they’re anxious? Millennials, the generation currently sandwiched between caring for young children and their aging parents.

Based on what we know happened last year and current consumer economic trends, here are four predictions for retailers to take into planning for the year end sales bonanza.

Prediction #1: Use of buy now, pay later loans will grow

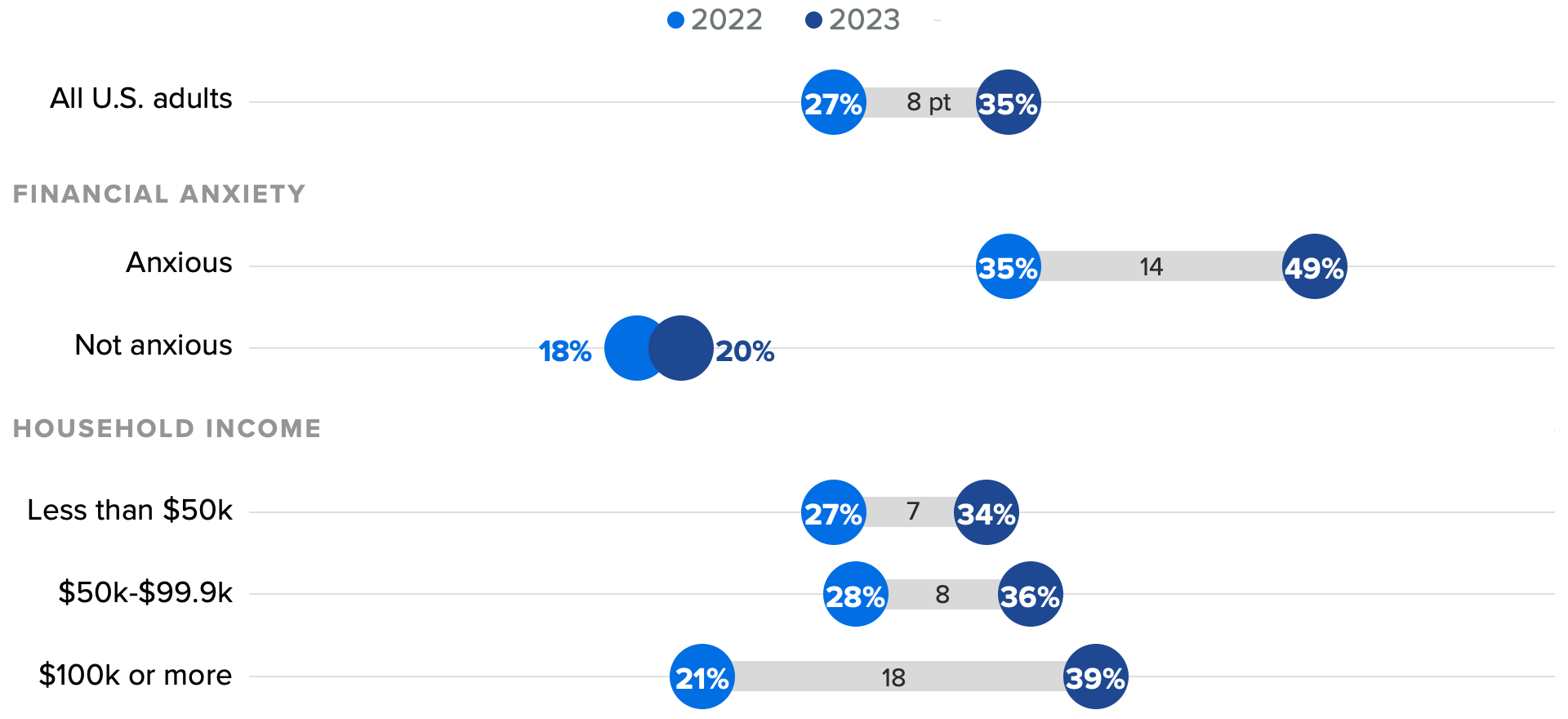

Buy now, pay later loans continue to be popular with shoppers, especially young consumers. Those who have kept up discretionary spending despite inflation are increasingly leaning on BNPL and away from high interest credit cards. In the 2023 holiday season BNPL was a key part of shoppers’ financial plans, particularly financially anxious and high income shoppers.

2023 saw an increase in the BNPL consideration among high income and financially anxious shoppers

A recent announcement from the Consumer Financial Protection Bureau confirmed that BNPL lenders are in effect credit card providers, and subject to the same consumer protection regulations as traditional credit card companies. This should only serve to enhance consumers’ perception of BNPL providers as a reliable financial tool.

Prediction #2: “Value” will remain the word of the year

Consumer spending has remained relatively strong throughout this inflationary period, though signs of weakness are showing, particularly among middle-income households. About one-third (34%) of consumers say “giving a gift for a wedding, birthday or other occasion would put a strain on their finances for the month,” a share that’s increasing for the middle income bracket.

Gift-giving strain is on the rise for middle-income households

Retailers including Walgreens, Best Buy and Michaels are responding to consumers’ pull back and announced significant price drops, particularly on general merchandise and household goods. In an already heavily promotional time of year, retailers should expect stiff competition on price as consumers find the lowest cost ways to keep the holiday magic alive. Cheap and cheerful gifts and decor will win this year.

Prediction #3: Early bird shoppers will be looking to splurge

Last year saw a significant jump in early shopping (17 weeks before Christmas) from Gen Zers (+13 percentage points form 2022 to 2023) and high earners (+7 percentage points over the same period). Rather than trying to shop early to spread holiday expenses out over more time and paychecks, early bird shoppers were just having fun.

Early holiday shopping reflects financial ease, not strain

This year, shoppers with more discretionary flexibility in their budgets will once again be eager for an excuse to shop and spend. Major sale events like Black Friday (which is not necessarily meaningfully tied to the Friday after Thanksgiving) encourage stocking up on gifts for others, as well as treats for oneself.

Prediction #4: Special shopping events will lure shoppers into stores

Store enjoyment is on the upswing as inflation cools, particularly among high-income shoppers. Higher prices sucked the fun out of shopping, but early 2024 data shows a rebound. Retailers, especially those catering to younger customers, should plan for events in a big way. Beyond the typical pictures with Santa, consumers are most interested in events with food and drinks — a great opportunity for brand partnerships — and special brand events.

Millennials and Gen Zers are most interested in attending in-store events

These events aren’t explicitly tied to winter holidays, and retailers should deploy these options year-round to draw in young shoppers. E-commerce brands without physical spaces should seek out brick-and-mortar partners for pop up events, and vice versa: bringing a brand that consumers don’t often get to shop in person is a good draw for store foot traffic.