Consumers Could Face Mounting Debt Pressures in 2023, With Lower Earners Looking Most Vulnerable

Key Takeaways

Recent trends in household finances are promising: In early 2023, incomes increased and consumers were better able to pay down debts.

However, a closer look at sources of income and debt across income groups shows that many consumers may be increasingly exposed to risks from inflation and rising interest rates in the coming months.

Lower-earning households look especially vulnerable to rising prices and financing costs, suggesting recent progress toward reduced financial inequality could be reversed later this year.

For more on consumer spending, read our report on household finances and the threat of inflation.

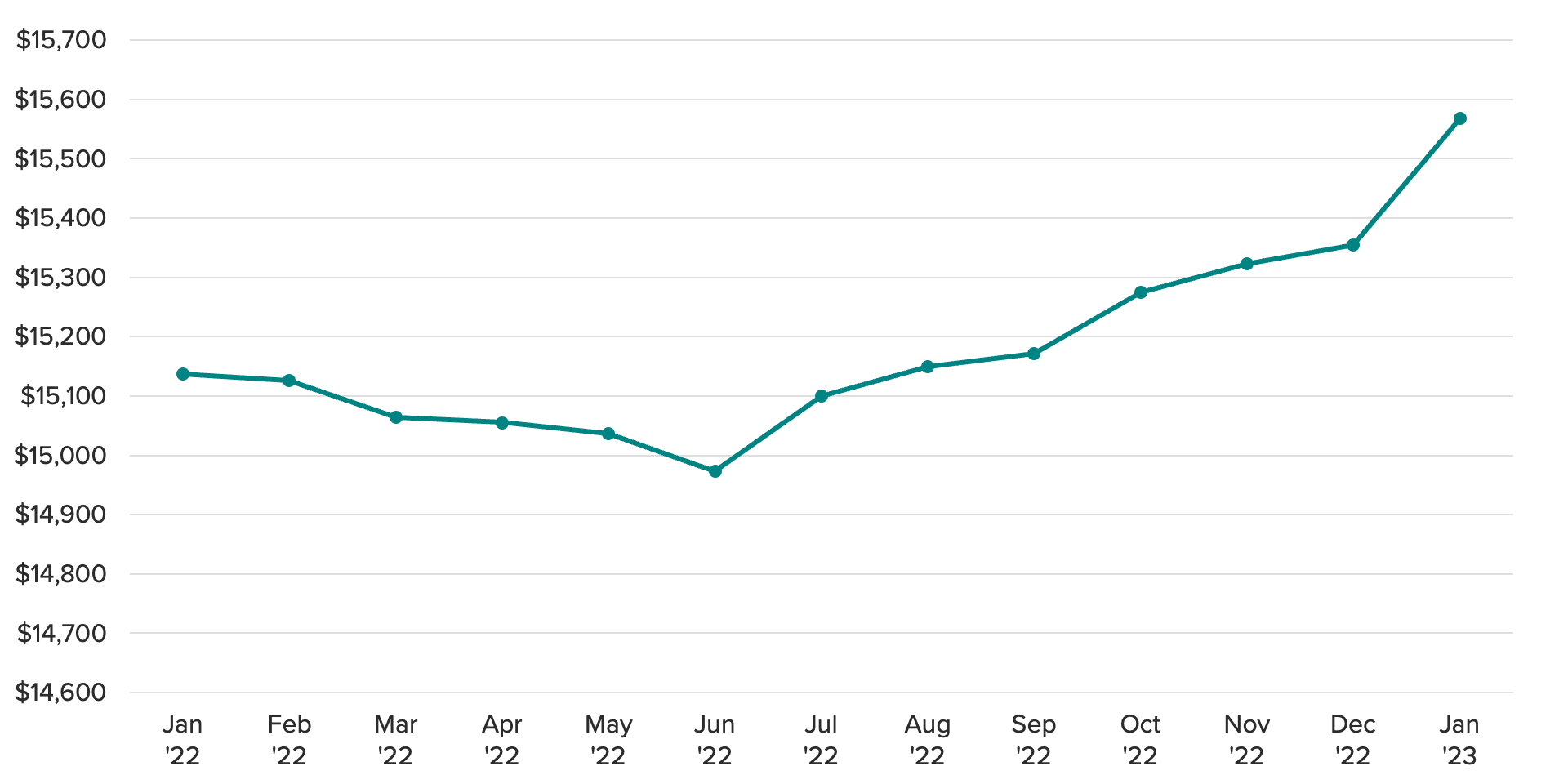

Consumer spending rebounded in January, continuing 2022’s theme that the U.S. consumer remains resilient despite persistent elevated inflation. The question now is whether recent strength in outlays is a sign that robust spending may continue in the coming months, or if the prolonged strain of rising prices and higher interest rates will increasingly restrict expansion.

Source: BEA, Morning Consult, Haver Analytics

To answer this question, it is helpful to examine the main sources of funds that underpin consumer spending: income, savings and debt. This third major funding source for consumers — debt — may play an increasingly critical role in shaping household finances and spending in 2023. As inflation diminishes purchasing power of wages and savings, more consumers may need to take on additional debt to cover expenses — even though the cost of using this funding source will rise as the Federal Reserve raises interest rates to cool price growth.

To this end, Morning Consult launched a monthly survey in October 2022 to collect detailed data on income sources and debt flows among U.S. consumers. Following on the credit card usage analysis released earlier this week, this memo seeks to highlight differences in earning and debt patterns based on household income level, and illustrate how these dynamics may impact consumer finances and spending power in the coming months.

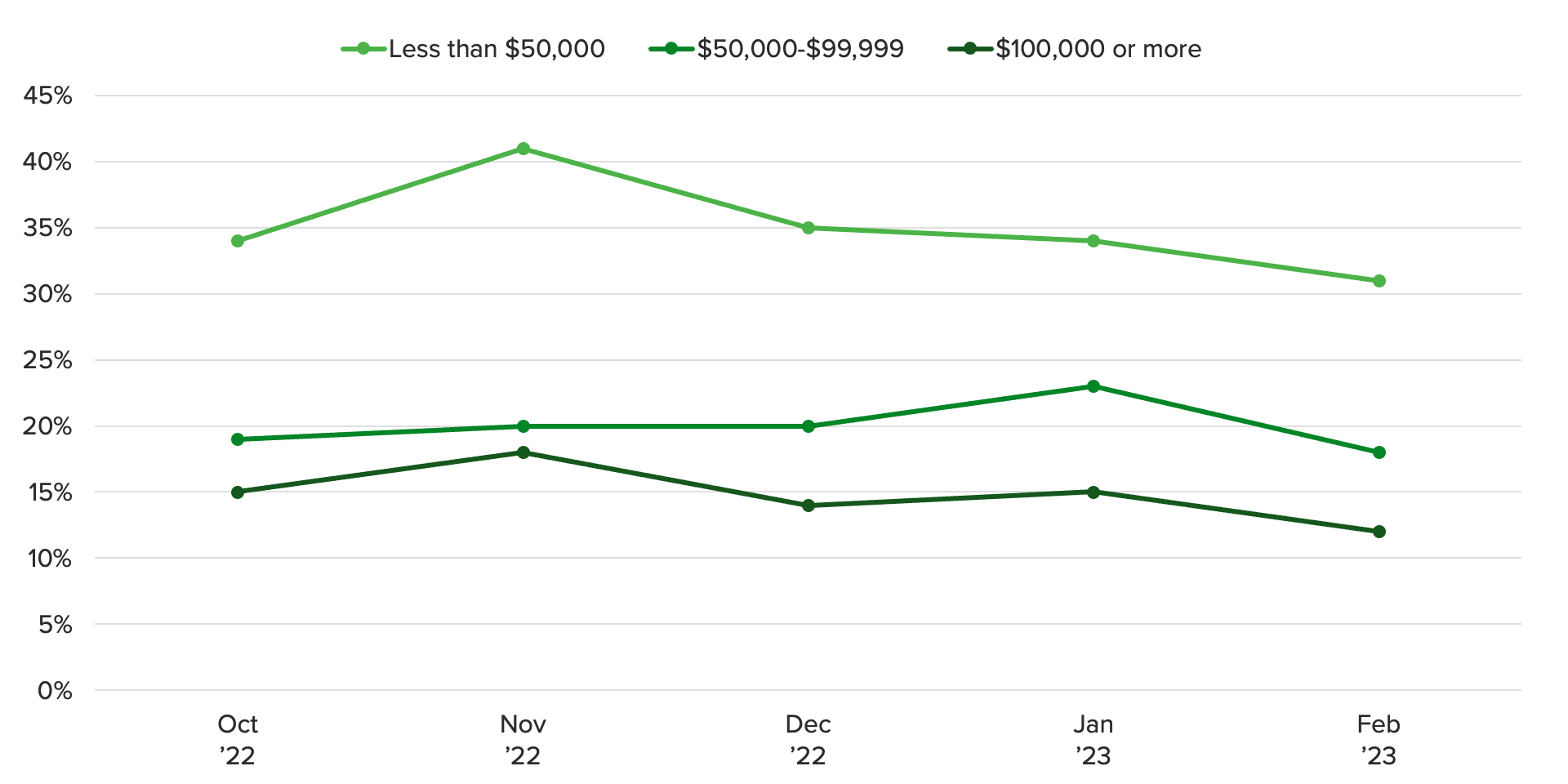

Households of all income levels benefited from decreased debt utilization pressures recently, but relief may be temporary

For all income groups, monthly debt obligations as a share of income declined in the past month to their lowest levels since tracking began in October. This dip in credit utilization was driven by both rising income and lower debt outlays.

In a positive sign for the lowest earners, the gap between their debt utilization and that of the highest income group also narrowed compared with Q4 2022. Stronger jobs and wage growth in lower-paying sectors, along with increased income from government outlays, have benefited households at the lower end of the income spectrum. However, there are reasons to suspect this recent improvement may be transitory as inflation and rising interest rates continue to shape household finances this year.

Lower earners’ purchasing power is disproportionately vulnerable to negative impacts of inflation

Growing reliance on debt could compound financial strains on U.S. households this year, especially among those with lower income and less in savings. While lower-earning households have recently benefited from improving finances, characteristics of this cohort’s income sources leave this group disproportionately exposed to potential fallout from elevated inflation and associated rate hikes this year.

Source: Morning Consult Economic Intelligence

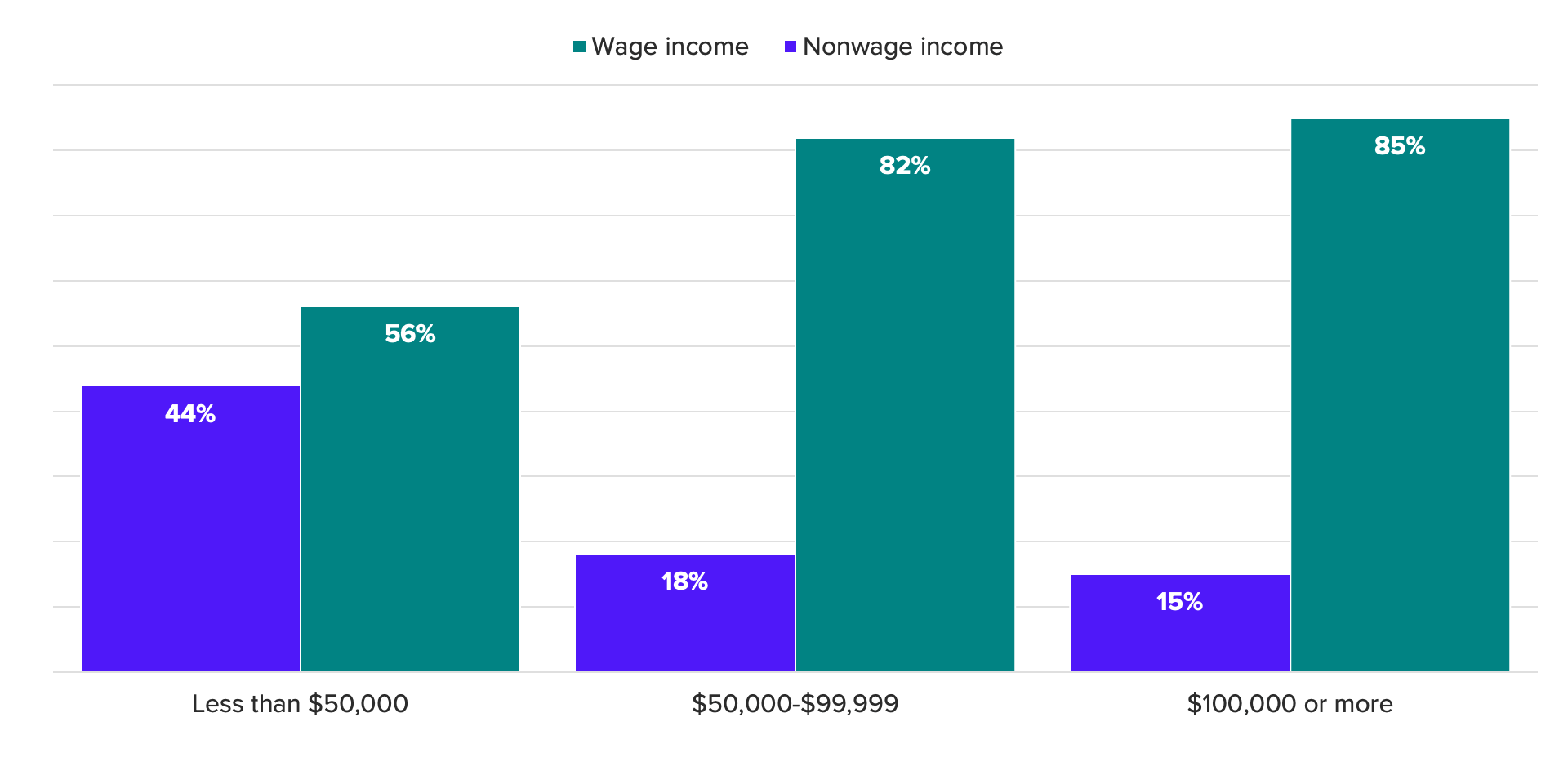

Adults from households earning less than $50,000 per year are more likely to rely on government transfers, including social security, disability payments and food stamps. Higher-earning households, meanwhile, tend to rely more on wages, business profits and investments as income sources. Each of these income sources is largely determined by market forces and can therefore adjust in response to nominal prices. Government outlays, meanwhile, will not fluctuate as often in response to prices.

For example, cost of living adjustments for Social Security were implemented in January. The 8.7% increase effectively offered a raise to recipients of these payments. Those earning less than $50,000 per year reported the highest share who rely on this income source, and thus would have disproportionately felt the benefit of the pay bump. However, this was a retroactive adjustment in response to high inflation over the past year; the payment amount in January may reflect the change in price levels felt over the course of 2022, but as Social Security payments remain fixed for the rest of the year, each month of additional inflation in 2023 will gradually erode their purchasing power.

Meanwhile, certain government benefits tied to the pandemic, such as expanded SNAP disbursements, are being pared back. As these income sources fail to keep pace with inflation this year, lower earners may be pushed to take on more debt to cover expenses.

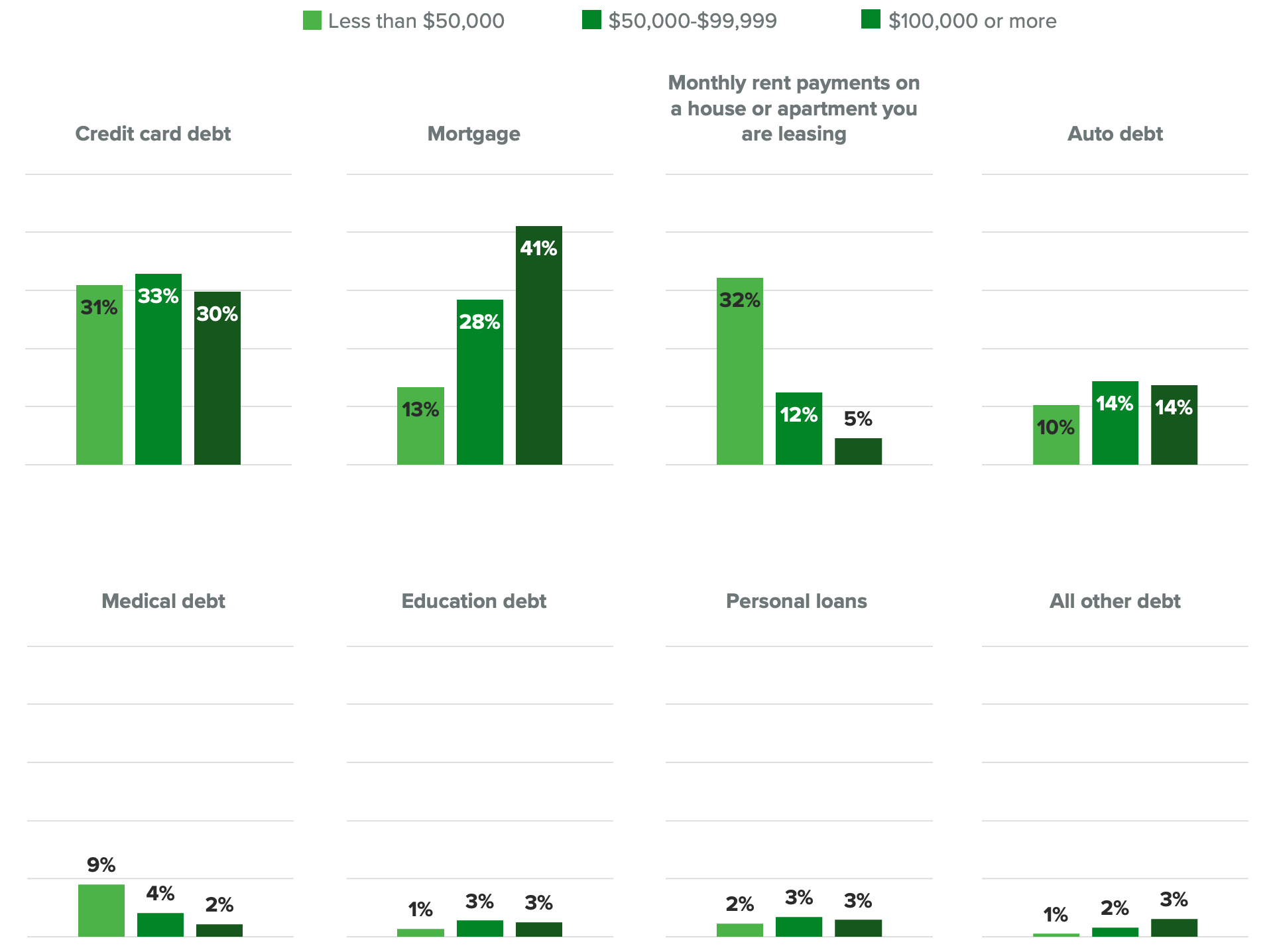

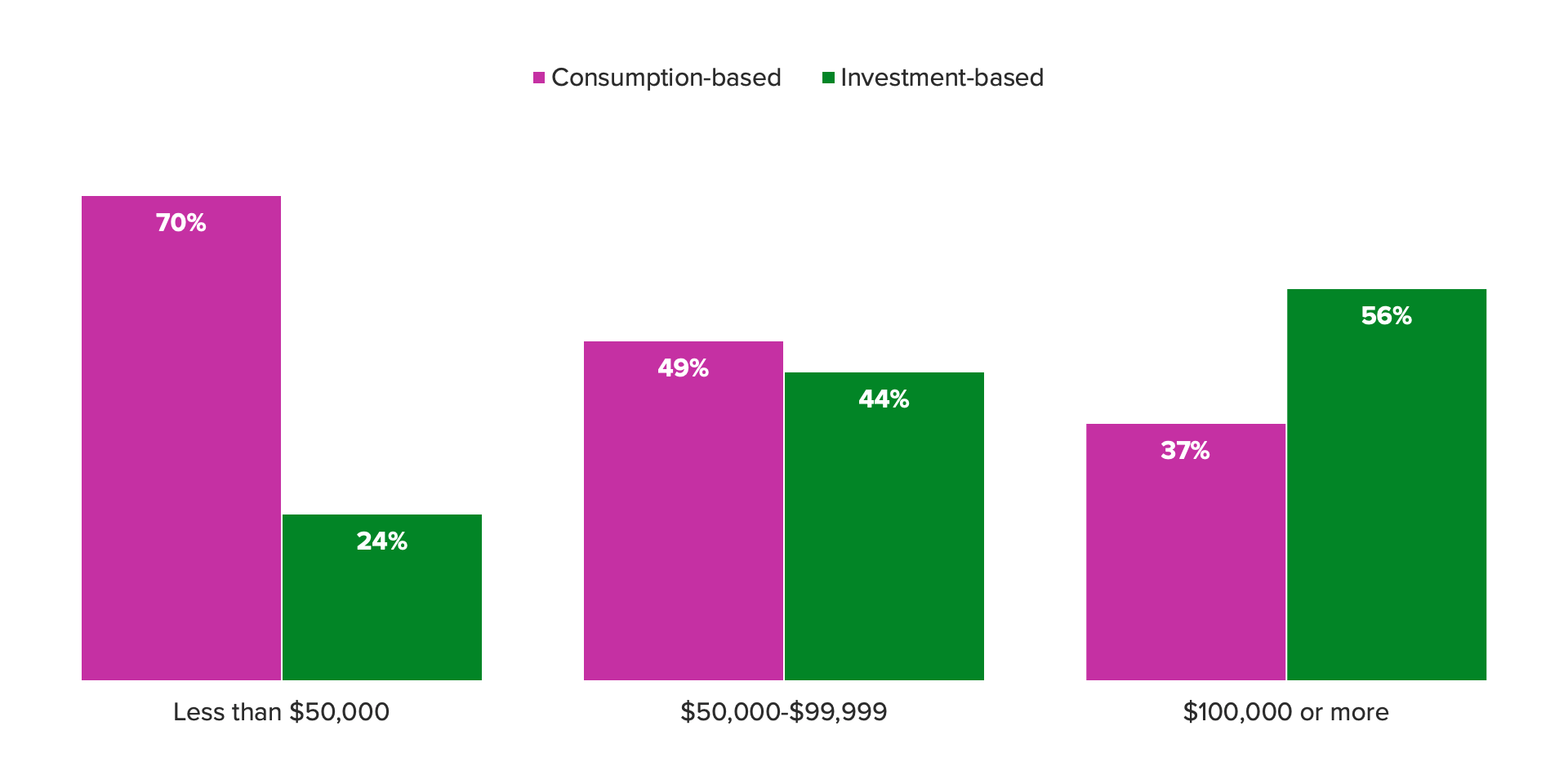

Lower earners’ debt is more likely to be tied to consumption, whereas higher earners are more likely to be servicing loans on goods and services with potential future value

The largest monthly debt obligations reported by consumers are housing costs and credit card debt. Credit patterns are roughly similar across income groups. Though spending allocations differ somewhat between essentials and discretionary items, credit card purchases are generally tied to past consumption — quite literally in the case of groceries or restaurant meals, but also in the sense of goods and services purchased for personal use or experience such as clothing, electronics or vacations.

Differences in types of housing-related debt, meanwhile, have more notable implications for financial outcomes by income group. High earners are much more likely to have a mortgage — implying homeownership — whereas lower earners’ housing debt is tied to rental leases. Therefore, while housing costs make up a roughly similar share of debt servicing each month for all consumers, high earners with mortgages have the opportunity to recoup a portion of that expense with the future sale of their home, while low earners paying rent do not.

A similar pattern is visible to a lesser extent with high earners’ debt allocation tied to educational and auto loans. Education, in theory, is an investment in that it confers the future benefit of higher earnings potential. Loans tied to auto payments are slightly different in that durable goods depreciate over time, but cars and trucks will typically have at least some future resale value.

In total, members of the lowest income group had 70% of debt tied to consumption — in other words, money they won’t see again. These categories include credit purchases, “buy now, pay later” programs, medical debt and rents. Only 24% of monthly debt payments for the lowest income group were tied to assets or investments with potential future value such as mortgages, education debt or auto loans. Comparatively, the highest-earning group had 37% of debt tied to consumption-centric categories, while 56% of monthly debt flows had potential to be at least partially recouped in the future.

Inflation and interest rates threaten to increase debt burdens

Not only does the consumption-related debt that makes up most of lower-income consumers’ monthly outflows lack the benefit of potential future value, but it also leaves its holders more exposed to inflation. As everyday expenses climb, so too could debt, even as the cost of carrying it increases due to higher interest rates.

Lower earners are not the only group exposed to the risk of rising interest rates as the Fed continues its quest to tame inflation this year. The labor market is expected to continue cooling, and layoffs have so far been concentrated among high-paying sectors such as technology or finance. The greater reliance on wage income relative to other sources among households earning $100,000 or more annually means this group could be detrimentally impacted if labor conditions continue to weaken for white collar jobs.

Risks are mounting at both ends of the income spectrum

Improving incomes boosted household finances in early 2023, reducing consumers’ need to rely on debt to finance spending. However, factors that contributed to these improvements are likely to fade if elevated inflation persists and the Fed continues to raise interest rates. So far, the rate hikes have had a more visible impact on higher-earning households, with homeowners and highly paid workers among the first affected by tighter financial conditions. However, lower-earning households will be especially vulnerable to developments in inflation and rate hikes going forward due to this group’s greater reliance on fixed income, higher utilization of debt relative to income and fewer opportunities to convert debt sources to income sources.

Kayla Bruun is the lead economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency economic data. Prior to joining Morning Consult, Kayla was a key member of the corporate strategy team at telecommunications company SES, where she produced market intelligence and industry analysis of mobility markets.

Kayla also served as an economist at IHS Markit, where she covered global services industries, provided price forecasts, produced written analyses and served as a subject-matter expert on client-facing consulting projects. Kayla earned a bachelor’s degree in economics from Emory University and an MBA with a certificate in nonmarket strategy from Georgetown University’s McDonough School of Business. For speaking opportunities and booking requests, please email [email protected]