Consumer Confidence Falls Despite Success in Fighting the Pandemic

Key Takeaways

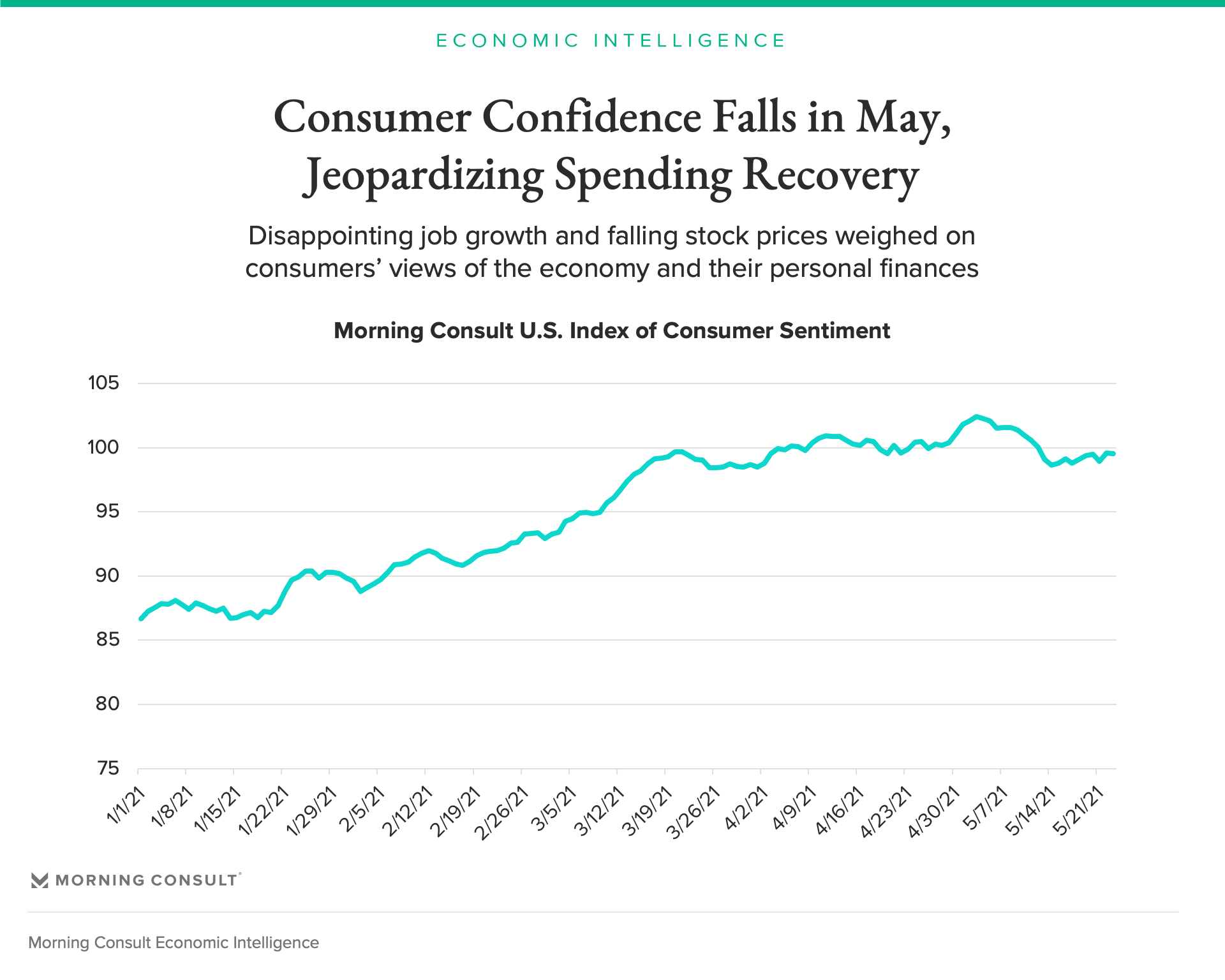

Morning Consult’s U.S. Index of Consumer Sentiment decreased between May 3 and May 23, marking the end of a four-month increase in consumer confidence.

Falling COVID-19 case counts have allowed consumers to shift their focus away from the public health crisis and toward the underlying economy, characterized in May by weak job growth, shrinking savings and falling stock prices.

Regardless of their willingness to engage in pre-pandemic activities such as indoor dining, consumers need jobs to provide them with incomes to spend on those activities.

Despite unprecedented direct financial support to millions of Americans and significant progress in the public health battle against the coronavirus, U.S. consumers have started to sour on the economy. Morning Consult’s U.S. Index of Consumer Sentiment fell from 102.40 on May 3 to 98.64 on May 14, before moderately rebounding to 99.56 as of May 23. The decrease in consumer confidence in May marks the end of four months of consistent increases, calling into question the speed and strength of the economic recovery.

This analysis describes the current drivers of U.S. consumer confidence, reconciling recent positive developments in the fight against the virus with consumers’ growing economic pessimism. How can consumer confidence fall at the same time as consumers feel more comfortable returning to normal than they have in the past year?

While these developments may seem contradictory, they provide different signals regarding the strength of U.S. consumers. Recent decreases in consumer confidence reflect consumers’ growing awareness of the serious financial and economic issues they are likely to face even after the economy fully reopens.

Vaccinations were unlikely to drive consumer confidence higher

The country’s success in vaccinating its population did not translate into an increase in consumer confidence in May for two reasons. First, by the end of April, the positive impact of vaccinations on consumer confidence was already baked into the numbers. American adults who planned on getting vaccinated were equally as confident in the economy as those who had not been vaccinated but planned on doing so. As a result, new vaccinations in May did not drive consumer confidence higher.

An increase in the willingness of vaccine holdouts to receive the vaccine has the potential to significantly increase consumer confidence. However, the share of vaccine holdouts has remained essentially unchanged at 34 percent since the week ending April 19.

Second, even though vaccinations have driven down the average number of new coronavirus cases in the United States, consumers do not improve their economic outlooks based on falling case counts. Morning Consult’s global, daily consumer confidence data in November 2020 identified the asymmetric relationship between the coronavirus and consumer confidence: increases in new cases or deaths exerts downward pressure on confidence, but decreases in new cases or deaths does not drive an increase in confidence.

The recent decrease in U.S. consumer confidence in May is consistent with these prior findings that argued that additional vaccinations after April would not drive further increases in consumer confidence. With the virus’ spread increasingly under control, consumers are able to turn their attention away from the pandemic and back to the fundamentals of the economy when making their financial and economic assessments.

The U.S. economy slowed in April, and consumers noticed

The second and third stimulus checks provided much needed boosts to households’ finances from January to April, translating into immediate increases in consumer confidence. However, these checks were never intended to act as permanent replacements for income from jobs. Rather, they were supposed to provide workers a lifeline or bridge, allowing them to pay their bills until the economy reopened and jobs became available. Unfortunately, those jobs have yet to materialize. The April jobs report was particularly disappointing, with adults across the income spectrum continuing to experience elevated levels of pay and income losses during the month.

Over two months after the passage of the American Rescue Plan, the impact of the third round of stimulus checks on personal finances is starting to wear off. A prior analysis estimated that $1,400 checks would allow 22.6 million adults to pay their expenses for at least 4.5 months without incurring additional debt or eating further into their depleted savings, assuming that they maintain income from work and unemployment benefits. As of May 24, half of the 4.5 months has already expired, leaving millions increasingly uncertain about their future financial prospects.

Lastly, recent volatility in stock prices also contributed to the decrease in consumer confidence. Although stock prices remain elevated by historical standards, growth in the S&P 500 slowed in April, and the index contracted in May following the disappointing April jobs report. Previous research shows the strong correlation between the S&P 500 and Morning Consult’s U.S. ICS, and this most recent period of stock market volatility is no exception.

Sustainability of economic recovery hangs in the balance

Even as more American consumers are inoculated and grow increasingly willing to engage in pre-pandemic activities such as going to the movies, decreases in their assessment of their finances and the economic condition of the country as a whole jeopardize the strength and sustainability of the economic recovery. Regardless of their willingness to engage in these activities, consumers need jobs to provide them with incomes to spend on pre-pandemic activities. The second and third rounds of stimulus provided millions of Americans with a financial bridge until July to partially cover their expenses while waiting for the economy to create millions of jobs. Consumers are closely following the rate of job growth to determine if the bridge was long enough.

John Leer leads Morning Consult’s global economic research, overseeing the company’s economic data collection, validation and analysis. He is an authority on the effects of consumer preferences, expectations and experiences on purchasing patterns, prices and employment.

John continues to advance scholarship in the field of economics, recently partnering with researchers at the Federal Reserve Bank of Cleveland to design a new approach to measuring consumers’ inflation expectations.

This novel approach, now known as the Indirect Consumer Inflation Expectations measure, leverages Morning Consult’s high-frequency survey data to capture unique insights into consumers’ expectations for future inflation.

Prior to Morning Consult, John worked for Promontory Financial Group, offering strategic solutions to financial services firms on matters including credit risk modeling and management, corporate governance, and compliance risk management.

He earned a bachelor’s degree in economics and philosophy with honors from Georgetown University and a master’s degree in economics and management studies (MEMS) from Humboldt University in Berlin.

His analysis has been cited in The New York Times, The Wall Street Journal, Reuters, The Washington Post, The Economist and more.

Follow him on Twitter @JohnCLeer. For speaking opportunities and booking requests, please email [email protected]