Introducing Morning Consult’s U.S. Reputation Tracker

Key Takeaways

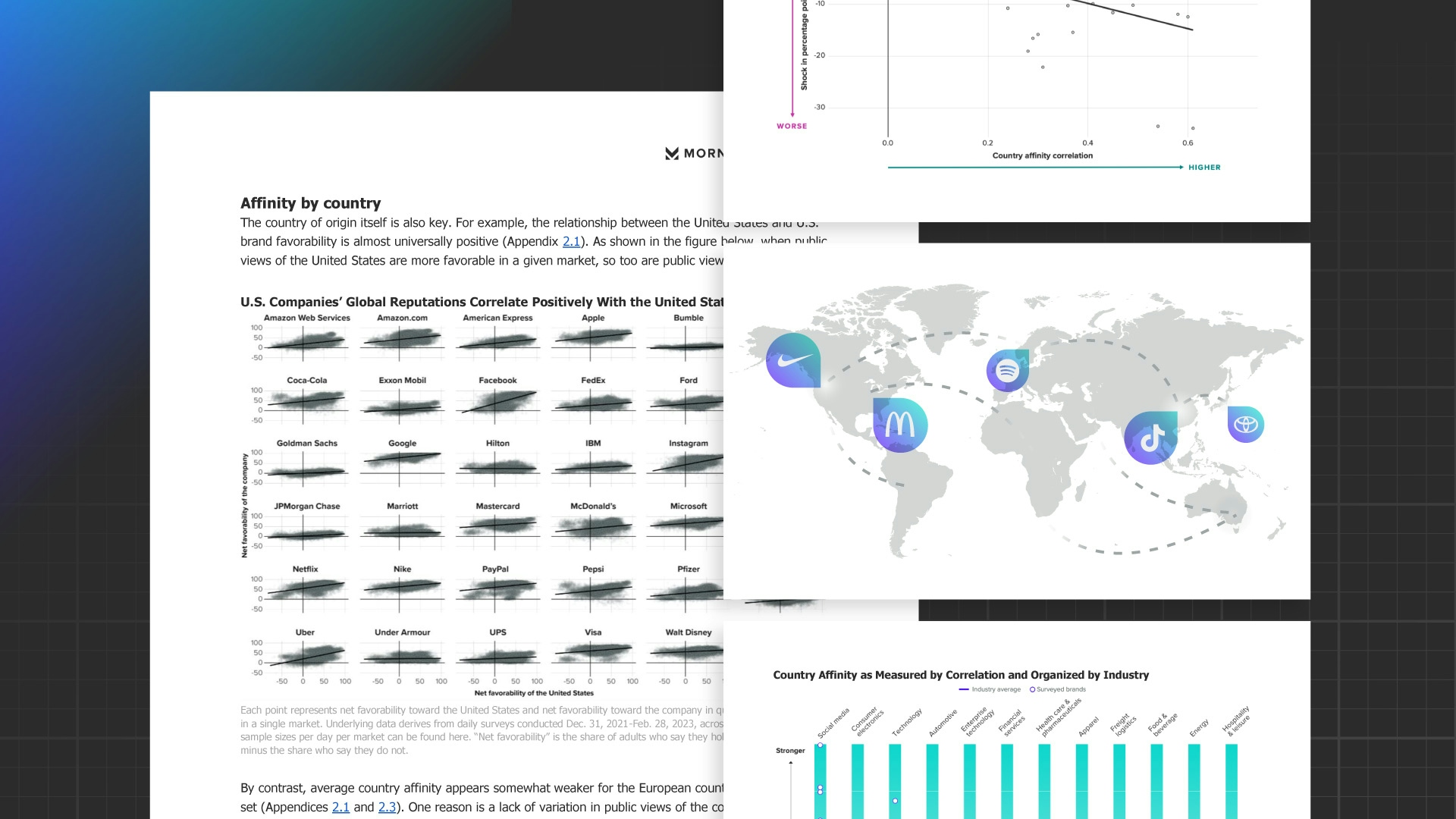

If there is one lesson for U.S. brands to retain from the past several years of geopolitical upheaval — marked by wars in Europe and the Middle East, and perennially strained relations between the United States and China — it’s that America’s reputation matters for their own.

Morning Consult has launched a global U.S. Reputation Tracker to assist companies in managing this relationship, and the risks and opportunities it affords. The tracker provides country-specific, regional, and global metrics of America’s reputation — including GDP- and population-weighted metrics — among overseas consumers and residents of supply chain host countries in 42 global markets covered by Morning Consult Intelligence. The tracker also provides sector-specific assessments of “country affinity,” defined as the strength of the relationship between views of America and views of U.S. companies, derived from global sentiment toward a blinded basket of major U.S. multinationals.

The tracker’s primary use-case is to facilitate corporate risk management and scenario planning efforts by enabling brands to identify (1) markets where unfavorable views of America pose a heightened risk of worsening brand reputation; (2) markets where favorable views of America offer revenue and supply chain opportunities; and (3) the sectors most exposed to these effects, whether positive or negative.

Per our reputation tracking data, which is presented in greater detail below, Donald Trump’s potential return to the U.S. presidency in 2025 and a worsening of the Israel-Hamas war, alongside strained U.S.-China relations, are among the three most pressing geopolitical threats to America’s reputation overseas and, by extension, to those of U.S. brands.

You can find our U.S. Reputation Tracker here, along with regularly updated downloadable data assets and a chart pack. Contact us with questions regarding the tracker and access to the underlying data beyond what is available via the tracker landing page.

Introducing Morning Consult’s U.S. Reputation Tracker

If there is one lesson for U.S. brands to retain from the past several years of geopolitical upheaval — marked by wars in Europe and the Middle East, perennially strained relations between the United States and China, and U.S.-led tariff wars targeting America’s trading partners — it’s that America’s reputation matters for their own.

Brands need look no further than the aforementioned geopolitical developments for evidence of this relationship at work: Views of major U.S. brands deteriorated dramatically following Moscow’s invasion of Ukraine in February 2022 due to America’s unambiguous support for Kyiv; consumers across the Middle East boycotted U.S. brands following the Oct. 7, 2023 Hamas attacks due to Washington’s staunch support for Israel, resulting in pronounced reputational hits to American brands; and Chinese consumers have routinely rolled out boycotts targeting U.S. firms amid worsening relations between Beijing and Washington. In brief, when America’s reputation dims among overseas consumers, so too does the luster of American brands.

The impact of Donald Trump’s election to the presidency in November 2016 on views of the United States and of American companies — inferred from trade patterns — is similarly well documented. And our own country affinity research, drawing upon brand and political data from Morning Consult Intelligence, systematically validates these dynamics globally, finding that views of America in overseas markets where U.S. brands serve consumers and/or route their supply chains are both correlated with, and can causally affect, views of American companies.

With no end to the Russia-Ukraine and Israel-Hamas wars in sight, U.S.-China relations chilled if not frozen for the foreseeable future, and President Trump’s potential return to the White House in 2025, the global geopolitical environment is likely to get worse before it gets better. Amid this challenging backdrop, U.S. companies would be wise to devote additional resources to managing the risks — and in some cases, opportunities — linked to shifting global views of America.

Tracking geopolitical risks to, and opportunities arising from, America’s global brand

To assist companies in doing so, Morning Consult has launched a global U.S. Reputation Tracker. The tracker leverages our daily survey data to provide country-specific, regional, and global metrics of America’s reputation — including GDP- and population-weighted metrics — among overseas consumers and residents of supply chain host countries in 42 global markets covered by Morning Consult Intelligence, with historical coverage of nearly four years.

Across all countries and metrics featured in the tracker, we measure U.S. reputation as net favorability toward the United States, defined as the share of consumers holding favorable views of America minus the share holding unfavorable views. The tracker reports these data points on a monthly basis. For clients seeking higher frequency metrics of America’s reputation, the favorability data underlying the tracker is available across 42 markets on a daily basis via Morning Consult Intelligence. Additional methodological details can be found here.

In addition to measuring U.S. reputation globally, the tracker also provides sector-specific assessments of “country affinity,” defined as the strength of the relationship between views of America and views of U.S. companies, derived from global sentiment toward a blinded basket of major U.S. multinationals available via Morning Consult Intelligence.

The tracker’s primary use-case is to facilitate corporate risk management and scenario planning efforts by enabling brands to identify (1) markets where unfavorable views of America pose a heightened risk of worsening brand reputation; (2) markets where favorable views of America offer revenue and supply chain opportunities; and (3) the sectors most exposed to these effects, whether positive or negative. Firm-specific analysis is possible using Morning Consult Intelligence data on a case-by-case basis.

The biggest risks on the horizon

Per the past several years of our U.S. reputation tracking data, Donald Trump’s potential return to the White House in 2025 (and its implications for both global trade policy and the war in Ukraine), a worsening of the Israel-Hamas War, and increasingly strained U.S.-China relations are among the three most pressing geopolitical threats to America’s reputation overseas and, by extension, to those of U.S. brands. We address each in turn.

1. A second Trump presidency

The final months of the Trump presidency saw America’s global reputation solidly underwater on an unweighted and GDP-weighted basis — and nearly underwater on a population-weighted basis — among consumers in a core set of overseas markets where our tracking data history is the longest (markets include Australia, Brazil, Canada, China, France, Germany, India, Japan, Mexico, Russia and the United Kingdom). In the year-long period following Joe Biden’s inauguration in January 2021, America’s reputation rebounded sharply, rising by approximately 20-30 points on a net basis across the three metrics we examine (see leftmost portion of chart below). No other single event in the history of our data has had such a profound impact on America’s reputation among overseas consumers.

Global average U.S. reputation: Core markets

Should a second Trump presidency materialize, we expect it to drive a shift of similar magnitude in reverse. On the trade front, U.S.-led tariff wars targeting American allies and partners — a mainstay of trade policy under the first Trump administration — are poised to return in force and will almost certainly have knock-on effects for America’s reputation overseas and by extension, for U.S. exports. American brands should anticipate potentially greater reputational fallout this time around in light of Trump campaign proposals to enact a 10% blanket tariff on all foreign goods entering the U.S. market, alongside a 60% tariff on goods coming from China. Our own research has documented the potential fallout for U.S. companies doing business in Asia — whether trading or investing — as a function of America’s reputation in the region, in a clear nod to the aforementioned risks. With an expanded global trade war potentially on the table, we expect the repercussions for U.S. brands doing business the world over to be swift and serious, particularly in China.

We anticipate similar risks to American brands arising from a pivot in U.S. policy toward the war in Ukraine under a second Trump presidency. As our own research has documented, America’s reputation rose substantially among European consumers following the war’s onset, a trend we attribute to the Biden administration’s robust support for Ukraine and for NATO. But as the administration’s ability to deliver on pro-Ukraine war efforts has suffered amid congressional infighting, so too has America’s reputation: While European consumers’ views of NATO remain robust, their favorability toward America is now below pre-war levels. A second Trump presidency would likely aggravate the situation owing to Trump’s well-known hostility toward NATO, and his potential favoritism toward Russia when it comes to ending the war.

The policy contours of a second Trump presidency remain uncertain, as does the likelihood that it will materialize. But given the above dynamics, brands would be wise to price the potential risks of such an outcome into their scenario planning efforts now, lest they be caught unawares come November.

2. The Israel-Hamas war

As the Israel-Hamas war has shown, worsening views of America among overseas consumers may hit brands seriously — or not at all — as a function of where their core overseas markets and supply chains are located. These localization effects speak to the need for brands to be attentive not only to what events constitute potential reputational risks, but also to where they are located and whether they are global in scope or more limited.

Case in point: Among our larger set of 42 overseas markets where we track America’s reputation, the onset of the Israel-Hamas war in August 2023 drove a relatively moderate downswing in global average views of America on the order of 4-6 points in the window bookending the initial Hamas attacks (September-November, 2023), with a downswing of similar magnitude observed across core tracking markets. Relative to a second Trump presidency, we therefore expect a marked increase in Israeli wartime aggression — such as that linked to a full-scale invasion of Rafah — to pose less generalized risks for U.S. brands doing business overseas.

Global average U.S. reputation: All markets

But these relatively muted global trends mask more pronounced regional swings — all to the downside — that American companies should be attentive to on a forward-looking basis. Should the conflict worsen, it will come as no surprise that we expect the potential risks to be most pronounced in MENA countries, which saw an average 16 point drop in net favorability toward the United States in the window surrounding the war’s onset. But we also anticipate localized risks in Asia, where the U.S. saw a 7-point downturn in net favorability during this same time period, due largely to sharply deteriorating views of America in countries with large Muslim populations (e.g. Indonesia, Malaysia and Pakistan). By contrast, we expect risks to U.S. brands doing business in Europe and the Americas to be less pronounced, though we expect Europe to pose some secondary risks for companies adopting strong pro-Israeli stances.

Regional average U.S. reputation: All markets

If there is a bright spot for U.S. companies amid the ongoing conflict, it’s that the impact of the war on U.S. brands will be severe for some, and trivial for others. Amid future geopolitical crises, this suggests that our data will be most useful as a predictive tool in markets that are geographically close to the crises, and where shocks to country favorability are most acute and channel through to brand favorability more generally. Brands that fail to quantify their exposure risk being caught unawares in overseas markets further down the road.

3. Worsening U.S.-China relations

Relations between Washington and Beijing have been deteriorating since at least the onset of the U.S.-China trade war in January 2018, when former President Trump imposed tariffs on imported solar panels and washing machines, largely viewed as targeting China — before ballooning into 25% tariffs on a wide range of Chinese imports and tit-for-tat retaliation from Beijing, alongside expansive and historically unprecedented reviews of Chinese stateside business operations via the Committee on Foreign Investment in the United States.

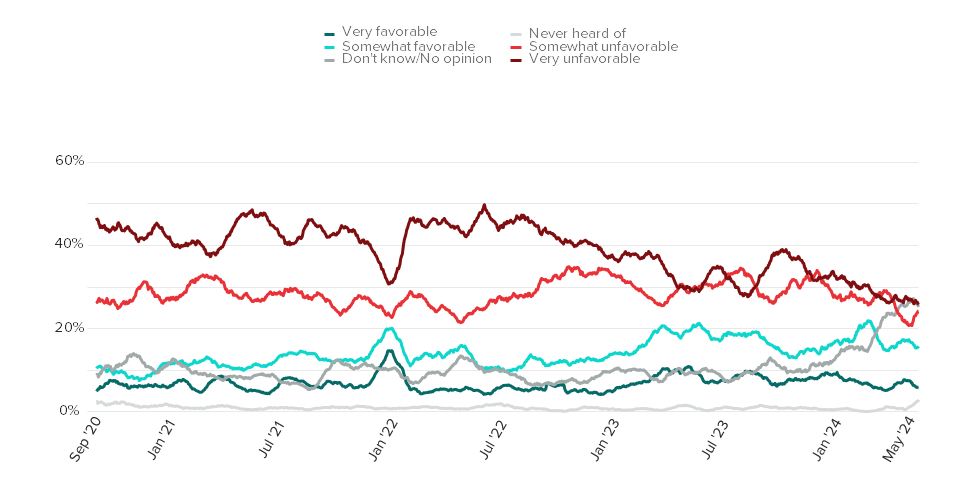

The situation has not dramatically improved: While fewer Chinese consumers hold “very unfavorable” views of the United States relative to the waning days of the Trump administration, the share holding “unfavorable" views has remained relatively flat, and the average Chinese consumer is far more likely to hold negative views of the United States than positive ones.

America’s reputation among Chinese consumers

In comparative perspective, China ranks below only Russia when it comes to overseas markets holding the most unfavorable views of the United States globally, reflecting the continuation and, in some cases, expansion of many of Trump’s trade- and investment-related policies under the Biden administration.

America’s reputation by overseas consumer market

As Biden has recently signaled with his efforts to impose new tariffs on some Chinese imports and end tariff exclusions on others, trade and investment action targeting Chinese firms would likely continue to expand under a second Biden presidency. Our expectation is that Chinese views of America would deteriorate in turn. Should former President Trump return to the White House, we expect the reputational and material consequences for U.S. brands to be far worse owing to more severe tariff action.

Regardless of the administration in place come November, should trade policy tensions continue to ramp up (our current expectation), we also expect an increased likelihood of Chinese consumer boycotts, in turn magnifying the risks facing American firms with a physical presence in China, in addition to risks posed by anticipated retaliatory tariffs emanating from Beijing. With respect to boycotts specifically, our own research from last year has shown that while Chinese consumers’ support for aggressive foreign policy has softened a bit, their enthusiasm for it remains strong overall. We expect similarly strident economic nationalism to pose risks to U.S. brands going forward in light of our late 2023 finding that roughly 70% of Chinese consumers said they’d be willing to boycott a foreign firm in 2024. Should U.S.-China relations take a turn for the worse, we would expect the share to rise.

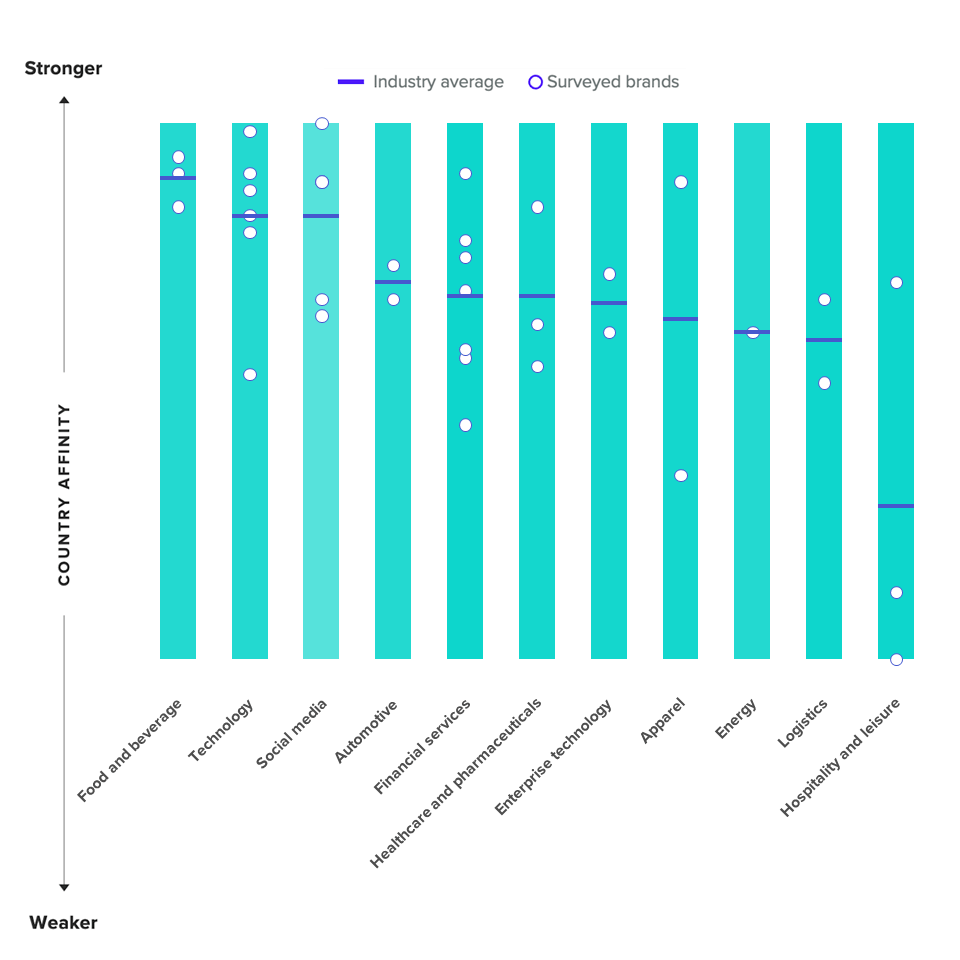

Sector-specific risks

Just as the severity of reputational risks to U.S. brands doing business overseas varies by country, so too does it vary by sector. To measure these effects, our tracker relies on a proprietary country affinity metric which assesses the strength of the relationship between views of America and views of U.S. brands using blinded data from a subset of major U.S. multinationals. Higher country affinity indicates a stronger relationship, posing heightened risks for companies that find themselves in high-affinity sectors when views of America are dour, and heightened opportunities when views are favorable.

U.S. country affinity by sector

As our research surrounding both the Russia-Ukraine war and the Israel-Hamas war has shown, country affinity is dynamic over time, such that the sectors most exposed to the risks and opportunities emanating from views of America abroad may vary substantially when a new crisis emerges. To offer one example, whereas the U.S. tech sector (and social media companies specifically) faced heightened exposure at the outset of the war in Ukraine (and still enjoy high country affinity with the United States), the Israel-Hamas war has shifted these dynamics, rocketing the food and beverage sector into pole position, in line with external reporting on the matter.

Our tracker provides a novel tool for brands to measure these sector-specific dynamics on a near real-time basis, complementing their monitoring of country-specific and regional effects in markets where they do business.

Guidance for brand stewards

U.S. brand reputation is now at the mercy of geopolitical upheaval and will remain so for the foreseeable future. In recognition of this fact, the savviest U.S. brands will take steps to mitigate their exposure, with a second Trump presidency — and its implications for both global trade policy and the war in Ukraine — the Israel-Hamas war, and worsening U.S.-China relations among the most pressing risks worth monitoring. Our U.S. reputation tracker provides a one-stop shop for brands seeking to adopt a data-driven approach to managing these dynamics at a speed and scale that has heretofore not been possible.

Brand stewards can find the tracker here, along with regularly updated downloadable data assets and a chart pack.Please contact us with questions regarding the tracker and access to the underlying high-frequency data beyond what is available via the tracker landing page.

Jason I. McMann leads geopolitical risk analysis at Morning Consult. He leverages the company’s high-frequency survey data to advise clients on how to integrate geopolitical risk into their decision-making. Jason previously served as head of analytics at GeoQuant (now part of Fitch Solutions). He holds a Ph.D. from Princeton University’s Politics Department. Follow him on Twitter @jimcmann. Interested in connecting with Jason to discuss his analysis or for a media engagement or speaking opportunity? Email [email protected].

Related content

Country Affinity: Predicting Negative Reputational Shocks to Global Brands Amid the Israel-Hamas Conflict

Introducing Country Affinity: A New Morning Consult Tool to Safeguard Your Brand in an Uncertain World