Cooling Inflation Has Been Driven by Goods. How Long Will That Trend Continue?

This is the second of three memos in our What to Watch in Inflation series. Each one will explore how different key sectors of the economy could affect the evolution of inflation in the coming months, how those developments may drive the Federal Reserve’s decision-making and what these factors imply about the probability of a recession. Additional insights on spending and inflation can be found in our January Consumer Spending & Inflation report.

Key Takeaways

Goods price growth has steadily declined for the past six months amid diminishing supply chain disruptions and softened demand as consumers reallocated spending toward services.

While price growth for goods such as groceries is likely to continue slowing in the near term, upside risks for goods price growth remain a concern as much of the easy lifting sits in the rearview mirror.

Early signs of demand recovery for categories such as autos and furniture could reverse the downward trend in goods inflation, threatening to slow the Fed’s progress against inflation.

In the first memo of this series, we discussed how the nonhousing services portion of inflation has been stubbornly elevated, prompting concern that this component could hinder the Federal Reserve’s fight against inflation. Goods inflation, on the other hand, has forged a very different path over the past year: Annual price growth peaked in March 2022 before trending steadily downward over the second half of the year, assisting the Fed in making progress toward its goal of cooling top-line inflation. Should the disinflationary trend for goods shift to neutral or reverse, this component of inflation runs the risk of flipping from a help to a hindrance for the Fed.

Up until now, the story behind the slowdown in goods prices has been relatively straightforward: Supply chain disruptions cleared up, and goods demand softened as consumers reallocated more spending to services categories, causing price pressures to steadily dissipate. Over the second half of 2022, goods prices declined in most months. However, as Fed Chair Jerome Powell mentioned in his February press conference, the consensus belief is that negative monthly price growth for goods is transitory and will likely not continue in the long term. This memo seeks to examine some of the trends currently impacting various goods categories and identify potential upside risks to price growth over the remainder of this year.

Essential goods prices still have room to fall

Food and energy are essential purchases that make up a relatively large share of both consumer budgets and the Consumer Price Index. The energy component switched from a strong upside driver to a downward pull on inflation over the course of 2022. While food price growth has slowed slightly, it is one of the few goods categories that continues to put upward pressure on topline inflation.

Morning Consult’s data suggests that food prices are poised to continue cooling: Morning Consult’s Purchasing Difficulty Index for groceries, which measures consumers’ difficulty finding certain items, has fallen precipitously since tracking began in early 2022, suggesting that supply constraints continue to loosen. Concurrently, consumers are increasingly resisting price increases, as captured by the underlying indexes that make up the Consumer Purchasing Power Barometer. While consumers initially responded to elevated food prices by trading down (Substitutability Index), more have begun walking away from high-priced grocery purchases altogether (Price Sensitivity Index).

Disinflationary pressures from energy prices, combined with the recent trends for groceries, support the likelihood of further slowing in top-line inflation. However, these categories are notoriously volatile and closely linked to global commodity prices, as evidenced by the spike in food and energy prices following Russia’s invasion of Ukraine nearly a year ago. The reopening of China this year is poised to increase demand for commodities including energy and food, in turn putting pressure on prices. Prices for these categories thus remain vulnerable to potential external shocks that the Fed would have few tools to counteract.

Could the slowdown in durable goods prices start to plateau?

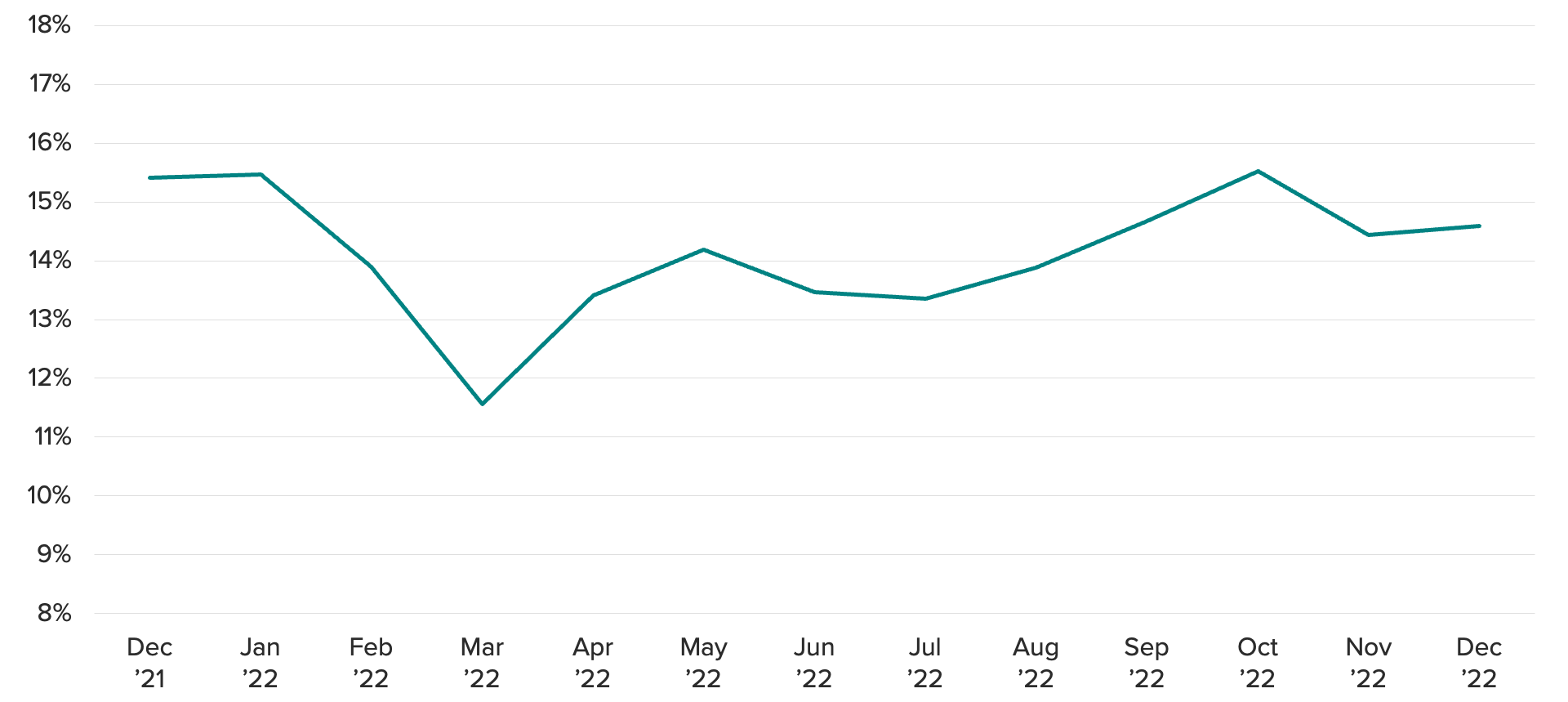

The durable goods category was among the first to show signs of easing inflation pressures, with annual price growth peaking in February 2022 and falling steadily through the end of the year. The same factors affecting goods overall — improving supply and the reallocation of spending to services — played a role in cooling price growth. Additionally, because large durables often constitute large investments for households, rising interest rates, fewer home sales and heightened price sensitivity for discretionary goods have exacerbated the slowdown in demand.

The drop in durables price growth has lasted nearly a year; annual inflation for the category fell to zero in December. Could dynamics be shifting to stabilize or even boost price growth this year?

Morning Consult’s data shows signs that demand for durables may be starting to recover. CPPB scores for home-related categories and autos rebounded in January compared with their respective 2022 lows. Purchase intentions across most of these same categories also improved on average from Q3 to Q4, though home repairs — which also had the smallest CPPB recovery — registered a decline as home sales slumped over this period.

While there is little evidence of a rapid rebound in durables purchases, some level of recovery for demand and prices is not unrealistic. Unaffordability and unavailability during 2022 may have prompted some accumulation of pent-up demand, and inventory levels relative to sales remain low by historical standards, especially for categories like autos. A bump in demand amid improving buying conditions could shift the course of durables inflation higher in the coming months.

Consumers’ discretionary budget allocations may influence the price path for smaller goods purchases

For smaller goods purchases such as apparel, electronics and sporting goods, price pressures have dissipated to varying degrees as consumers increasingly prioritize spending on services. However, that shift in spending patterns may be running out of runway in the coming months as the share of expenditures allocated to goods draws closer to its pre-pandemic level. Within the discretionary category, Morning Consult’s own monthly spending data showed a rebound in nondurable goods’ share of spending over the second half of 2022. Should this trend continue, demand-side factors could add price support to some of the smaller goods categories filling out the CPI.

Many of these types of consumer goods are imported. Further depreciation of the dollar against the currencies of major trading partners like China could also exert upward pressure on prices for these items.

Goods disinflation may regulate in the coming months, reducing helpful downward pressure on topline inflation

While we find little evidence of an imminent, rapid reversal in the supply-and-demand dynamics currently influencing goods prices, the current path of goods inflation will not continue indefinitely. It is therefore important to be mindful of upside risks to prices for goods components. For categories tied most closely to global commodity prices, such as food and gas, a multitude of external shocks could alter the course of prices. For instance, the war in Ukraine and related tensions could further disrupt supply, and China’s reopening is likely to lift demand.

Meanwhile, a turnaround in demand for other consumer goods could put pressure on inventories that have still not fully recovered by historical standards. For durable goods like autos and furniture, Morning Consult’s data has already picked up some signs of strengthening purchase intent. The negative influence of goods inflation thus far has been a critical aid to the Fed, but it remains to be seen how long the beneficial trends of loosening supply and moderating demand will persist.

Kayla Bruun is the lead economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency economic data. Prior to joining Morning Consult, Kayla was a key member of the corporate strategy team at telecommunications company SES, where she produced market intelligence and industry analysis of mobility markets.

Kayla also served as an economist at IHS Markit, where she covered global services industries, provided price forecasts, produced written analyses and served as a subject-matter expert on client-facing consulting projects. Kayla earned a bachelor’s degree in economics from Emory University and an MBA with a certificate in nonmarket strategy from Georgetown University’s McDonough School of Business. For speaking opportunities and booking requests, please email [email protected]

Sofia Baig is an economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency data. Previously, she worked for the Federal Reserve Board as a quantitative analyst, focusing on topics related to monetary policy and bank stress testing. She received a bachelor’s degree in economics from Pomona College and a master’s degree in mathematics and statistics from Georgetown University.

Follow her on Twitter @_SofiaBaig_For speaking opportunities and booking requests, please email [email protected]